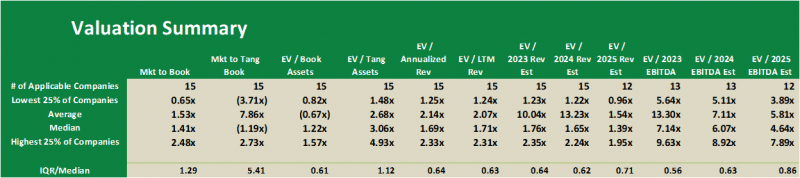

OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

The Viridian Value Tracker is the most comprehensive valuation product in the industry.

-

- A broad set of 12 valuation measures assures applicability, regardless of whether the company has analyst coverage or revenues. The typically presented EV/ Projected Revenues and EV/ Projected EBITDA are available for less than 1/3 of the cannabis companies we track.

- Most valuation studies present only the average valuation measures, while the Tracker goes one step further and shows the distribution of values (the quartiles, median, and dispersion) for each measure. This gives users a more complete view of how companies in the cohort group are valued.

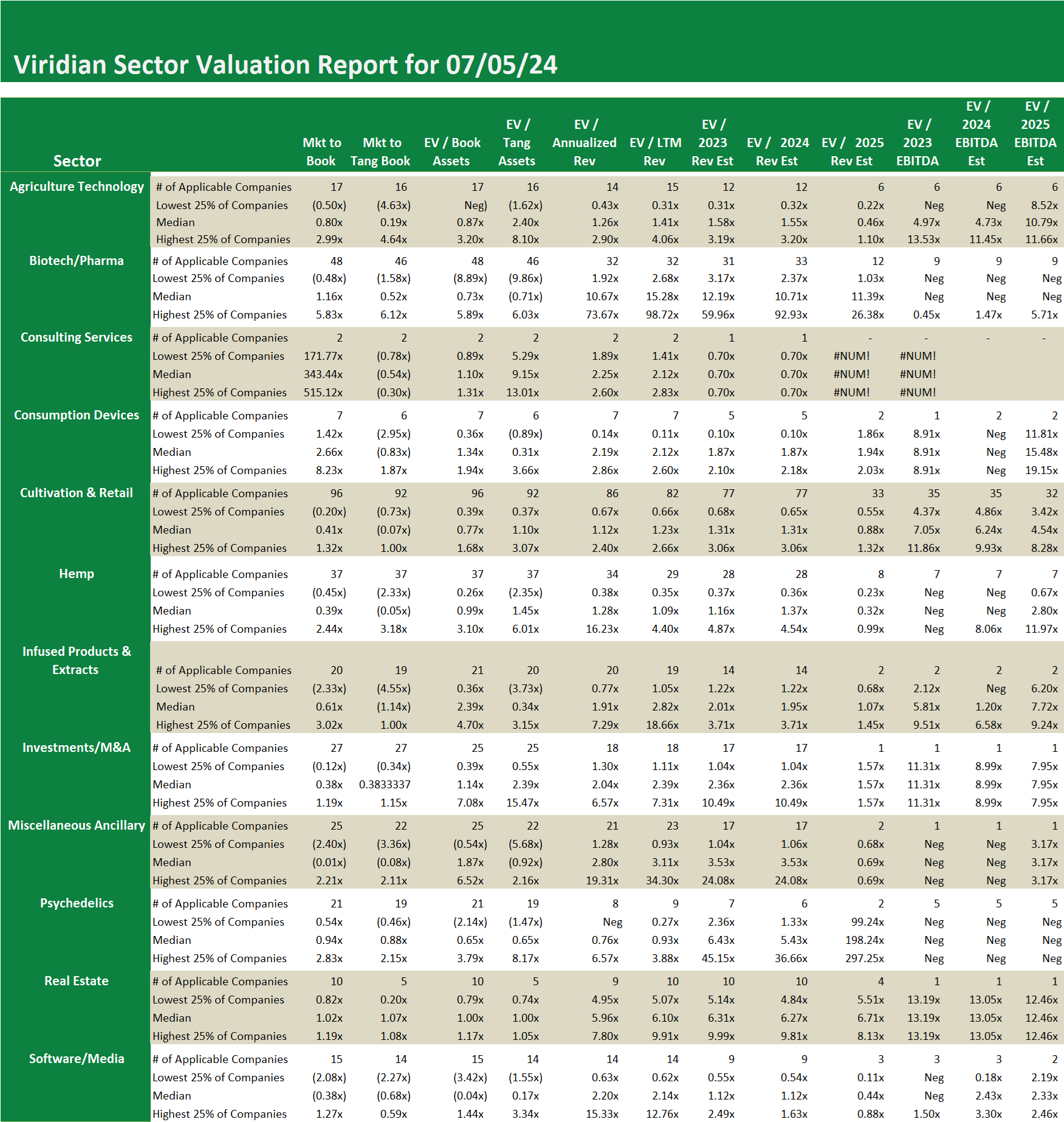

Sector Valuation Report – Comparing The Valuations of U.S. MSOs and Canadian LPs over $100M

US MSOs >$100M

Canadian LPs >$100M

The charts above compare the valuation metrics for US MSOs and Canadian LPs, which are over $100M in market cap.

- Curiously, the median EV/2024 EBITDA and EV /2025 EBITDA are significantly higher for the Canadian LPs than the U.S. MSOs. What could explain this discrepancy?

- If we take EV/revenue and divide it by EV/EBITDA, we get EBITDA/Revenue. Doing this calculation using median 2025 numbers, we get 35.6% for the U.S. MSOs compared to 7.5% for the Canadian LPs, demonstrating something most of us already knew – the US companies are much more profitable than their Canadian counterparts. So, one explanation might be that the Canadians have more room to improve profitability relative to the MSOs. Perhaps, but frankly, things have been going in the opposite direction for years, so that doesn’t seem likely to be the explanation.

- The more plausible reason is that the Canadians have access to a much broader group of investors and trade with much higher liquidity. We view this as an indication of how the MSOs might trade if a combination of S3 and SAFER (dare we mention that forgotten bill) could allow for uplistings.

- This points to the next giant leap for U.S. cannabis MSOs. Removal of 280e is powerful, but uplistings is the next frontier. The combination of S3 and uplisting probably makes for the best possible world for MSOs, better even than full legalization.

Sector Valuation Report – Comparing The Valuations of U.S. MSOs and Canadian LPs over $100M

US MSOs >$100M

Canadian LPs >$100M

The charts above compare the valuation metrics for US MSOs and Canadian LPs, which are over $100M in market cap.

- Curiously, the median EV/2024 EBITDA and EV /2025 EBITDA are significantly higher for the Canadian LPs than the U.S. MSOs. What could explain this discrepancy?

- If we take EV/revenue and divide it by EV/EBITDA, we get EBITDA/Revenue. Doing this calculation using median 2025 numbers, we get 35.6% for the U.S. MSOs compared to 7.5% for the Canadian LPs, demonstrating something most of us already knew – the US companies are much more profitable than their Canadian counterparts. So, one explanation might be that the Canadians have more room to improve profitability relative to the MSOs. Perhaps, but frankly, things have been going in the opposite direction for years, so that doesn’t seem likely to be the explanation.

- The more plausible reason is that the Canadians have access to a much broader group of investors and trade with much higher liquidity. We view this as an indication of how the MSOs might trade if a combination of S3 and SAFER (dare we mention that forgotten bill) could allow for uplistings.

- This points to the next giant leap for U.S. cannabis MSOs. Removal of 280e is powerful, but uplistings is the next frontier. The combination of S3 and uplisting probably makes for the best possible world for MSOs, better even than full legalization.