Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

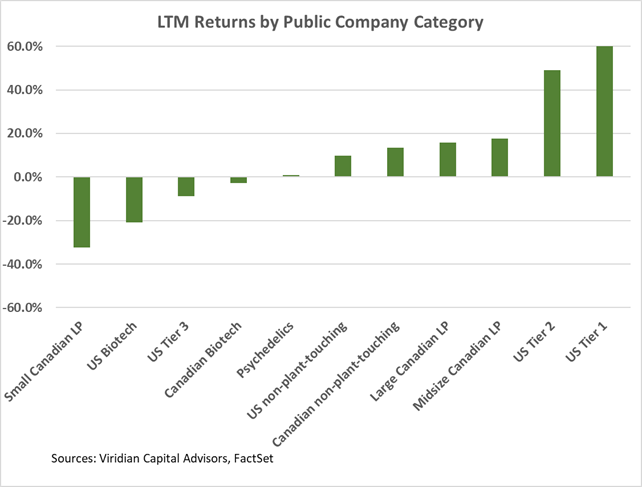

- Best & Worst Perfromers

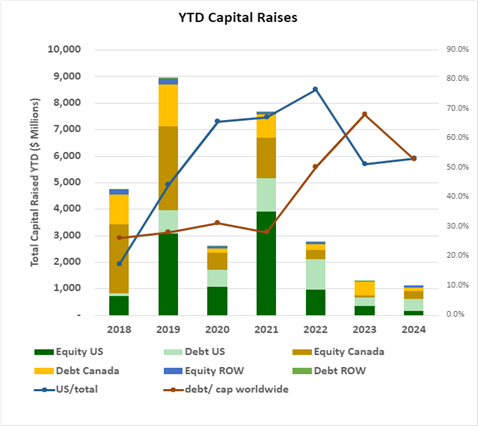

- YTD capital raises totaled $1,143.31M, down 12.6% from the same period in 2023. Debt as a percentage of capital raised dropped to 52.9% from 68.1% in the previous year on a worldwide basis. The U.S. bucked this trend with 73.0% of capital raised in debt compared to 50.6% in 2023.

- U.S. raises accounted for 53.2% of total funds, the lowest percentage since 2019. Conversely, raises from outside the U.S. represented a historically high 8.3% of the total funds raised.

- YTD raises by public companies accounted for 67.8% of total funds, the lowest percentage since before 2018.

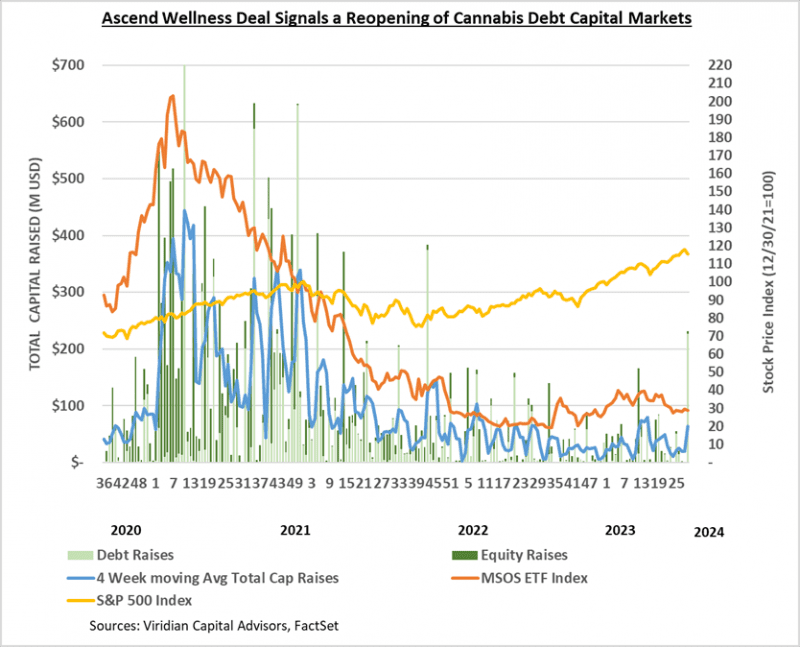

- Cannabis equities (as measured by the MSOS ETF) ended down 2.50% for the week.