Viridian publishes weekly data and analysis on debt capital raises in the Cannabis/CBD/Psychedelic industries. This data includes information about the company issuing debt (public/private, state/country location), deal size, deal structure, pricing, warrants, and credit data.

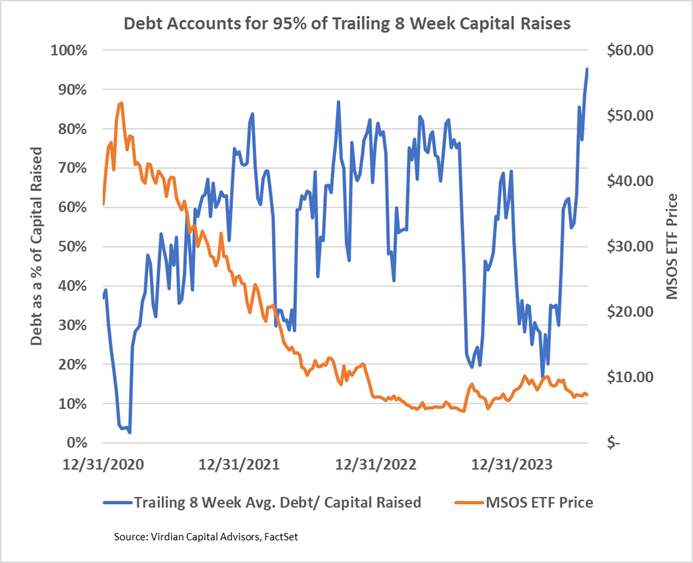

- Debt accounted for 95% of trailing 8-week capital raises, up sharply from last week due to the Ascend Wellness (AAWH: CSE) refinancing. The ratio may go down if companies are able to utilize favorable regulatory-induced stock price increases to complete equity issues.

- The Week’s Debt Transactions

- On 7/18/24, Ascend Wellness (AAWH: OTCQX) announced the closing of its $235M principal amount Notes issue with a 12.75% coupon and five-year maturity,

- The Notes will be issued at a price of 94.75%, which produces a yield to maturity of approximately 14.25%.

- The Notes are secured by substantially all assets of the Company and certain subsidiaries subject to certain carveouts.

- The Notes are callable at par for the first two years.

- The yield at first blush seems high, given where the Company’s debt has been quoted in the market recently; however, there appear to be no equity kickers, and the $275M issue that was maturing in August 2025 represented nearly 140% of the Company’s market cap.

- The last time such a significant maturity issue was addressed was the AYR exchange completed in February 2024. We expected AYR to have to pay a high rate of interest to complete that deal, but we were shocked to see AYR giving up nearly 25% of the Company’s equity for a two-year extension. Admittedly, Ascend is a stronger credit than AYR was at the time of its exchange, but the difference is still striking.

- Ascend noted that all of the four largest previous lenders, along with several new institutional investors, participated in the transaction.

- The transaction shows a substantial thawing of the cannabis credit markets ahead of the final enactment of S3. We expect refinancing news from TerrAscend and GTI to be forthcoming.

- The thawing of the debt market will take time to filter down to lower credit quality companies as new capital tends to gravitate to the most prominent, liquid names. However, tax-deductibility of interest expense from the removal of 280e will have a significantly positive impact on the cost of cannabis debt.

Viridian publishes weekly insights on debt capital raises in the Cannabis/CBD/Psychedelic industries. These insights typically highlight the most interesting/meaningful debt transactions of that week, and commentary on market conditions, debt deal structures, and lenders.