OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Each week, Viridian publishes insights and analysis on completed M&A transactions in the prior week. Our analysis includes:

-

- M&A Market Commentary

- Public and Private Companies

- Buyers & Sellers

- YTD M&A Analysis

- M&A by Industry Sector

- Deal Structure and Valuation Analysis

- Pending Deal Risk Arb Analysis

- Valuation Gap Analysis

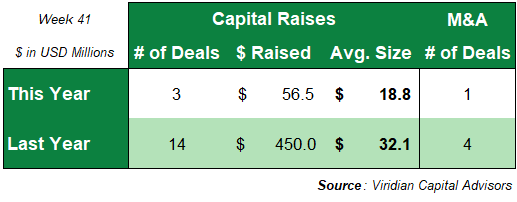

- One M&A transaction closed this week with a no disclosed transaction value compared to four transactions for $0.8M in the prior year.

Total YTD M&A volume is down 80.2% from 2021, with $4.72B in consideration and 145 deals closed versus $23.82B in transaction value and 271 closings in 2021.

- Last year’s total included two of the largest M&A transactions ever done in cannabis, the $4.5B Tilray acquisition of Aphria and the $7.2B Jazz Pharma acquisition of GW Pharma. Without the two megadeals mentioned above, the volume in 2022 would trail 2021 by 61.0% YTD.

- We believe the likelihood of relatively sizeable public/public M&A transactions has increased significantly based on the low trading multiples of tier 2 and 3 MSOs and SSOs, particularly those perceived to be cash flow pressured. We discuss this in our outlook section above.

U.S. volume is down 67.3%, with 40.4% fewer transactions.

- The average transaction size of $34.3M is down 45.1% from 2021. Still, 2022’s average is expected to grow as large public/public transactions like Cresco/Columbia Care close in the 4th quarter.

- The Cresco/Columbia deal spread narrowed by 370 bp to 13.2% on 10/14/22. Doubtlessly, the collapse of the Verano/Goodness Growth deal was an influence in the spread widening. However, we believe this transaction has a broader basis. Cresco’s motivation to purchase Columbia Care is not primarily based on the latter’s NY assets, the value of which is no longer clear.

- Verano canceled its acquisition of Goodness Growth in a surprise announcement this week. Perhaps we should have anticipated dramatic news from the severe spread compression we saw last week to only 2.8%. The spread compression appears to have been caused by a major ETF’s unrelated large purchase of Goodness shares. We believe the most likely underlying cause is a growing perception that the New York market is less attractive than initially expected. In its overarching pursuit of social equity, the state has stalled its adult rec rollout and allowed the illicit market to obtain what may prove to be an unassailable head start, ironically supplied by the largest legacy cultivation market in the world, California.

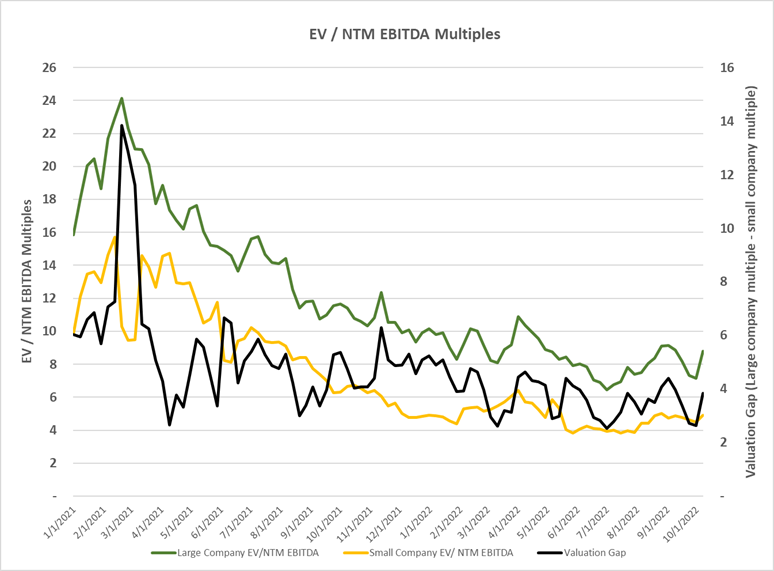

- The valuation gap narrowed 102bp to 3.85 on 10/14/22, significantly below its 3.96 LTM average. The valuation gap is the difference between the EV/NTM EBITDA multiple for the largest MSOs and the multiple for the less than $300M market cap group, which are their primary targets.

- This measure has been a significant driver of M&A activity since a larger gap creates an opportunity for more accretive transactions. The gap tends to increase in improving markets while declining in retreating markets.

- A gap of over 4 points is conducive to accretive transactions between the largest MSOs and smaller competitors. At the same time, a tighter financing market makes it more challenging for small companies to finance the growth of their business.

- We note that the gap is based on trading prices and not on values where a company could raise significant amounts of capital. The difference is crucial because one of the key drivers we see for accelerating M&A activity is the inability of smaller companies to finance themselves in the current cannabis capital markets.