OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Viridian publishes weekly data and analysis on debt capital raises in the Cannabis/CBD/Psychedelic industries. This data includes information about the company issuing debt (public/private, state/country location), deal size, deal structure, pricing, warrants, and credit data.

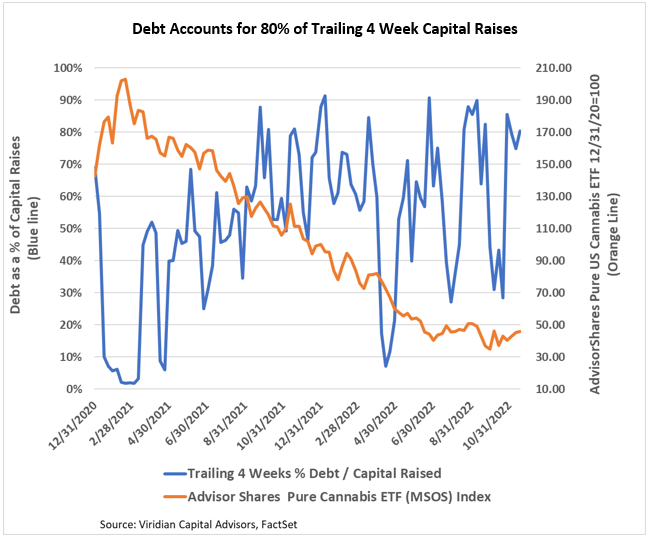

- Debt accounted for 80% of trailing 4-week capital raises. We expect this ratio to be volatile because of the limited capital raise activity but average above 50%. Several large MSOs, including TerrAscend (TER: CSE), Jushi (JUSH: CSE), and AYR (AYR.A: CSE), have significant refinancings to do based on their debt maturity schedules. Several smaller tier 2 and tier 3 companies have upcoming financing needs that we believe will spur an increase in debt financing.

The Week’s Largest Debt Raise:

- On November 15, 2022, Charlotte’s Web Holdings (CWEB: TSX)(CWBHF: OTC) announced the closing of a $56.7M Unsecured Convertible Debentures.

-

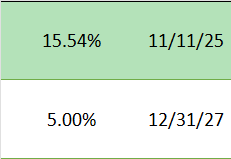

- The new convertible debentures have a 5% interest rate that steps down to 1.5% following the date that U.S. federal laws permit the use of CBD as an ingredient in food products or dietary supplements.

- The notes mature on November 14, 2029, and are convertible at approximately $1.51 per share (a premium of 131.6%)

- The notes were purchased by tobacco giant BAT and are convertible into approximately 19.9% of the outstanding common stock.

- The high premium reduces the value of the conversion option embedded in the convertible notes. Accordingly, the effective cost of the notes is only 5.52%. Although CWEB ranks as the top credit among the 12 Hemp companies in our database with market caps between $10M and $100M, its credit quality does not merit such a low effective cost. The implied credit support of BAT and interest in acquiring the company at a future date justifies the rate.

-

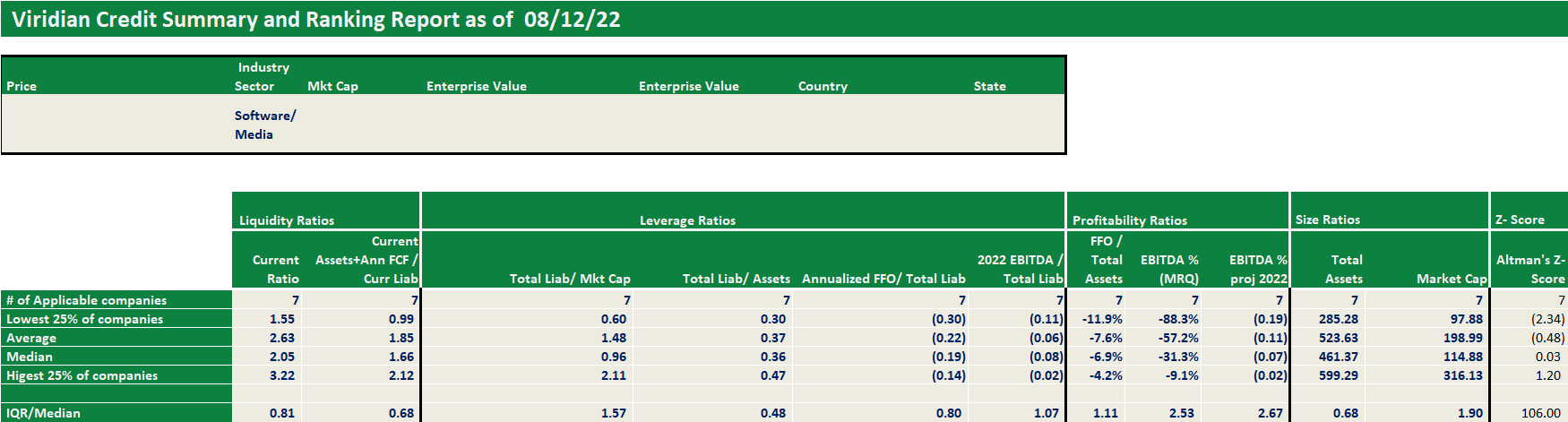

Each week, Viridian highlights a specific industry sector and provides a deep dive into credit metrics and comparable company credit rankings for public companies operating in that sector. Credit ratings are not currently available for public cannabis companies leaving companies, lenders, and investors with a gap of information. The Viridian Cannabis Credit Tracker fills this gap. The model uses 11 market and financial statement variables to discern 4 key credit factors: Liquidity, Leverage, Profitability, and Size, to provide credit/liquidity analysis for over 370 public Cannabis/Hemp companies.

Viridian publishes weekly insights on debt capital raises in the Cannabis/CBD/Psychedelic industries. These insights typically highlight the most interesting/meaningful debt transactions of that week, and commentary on market conditions, debt deal structures, and lenders.