OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Quick

Links

Past Charts

Home » Viridian Capital Chart of the Week: U.S. CULTIVATION & RETAIL CAPITAL RAISES FOR THE FIRST 15 WEEKS OF 2025 ARE DOWN 35% FROM THE SAME PERIOD IN 2024 AND ARE VIRTUALLY ALL DEBT

Chart of the Week

Chart of the Week

The Viridian Capital Chart of the Week highlights key investment, valuation and M&A trends taken from that week’s Deal Tracker that we believe are impactful for investors, companies and acquirers.

Week ended 04/11/2025

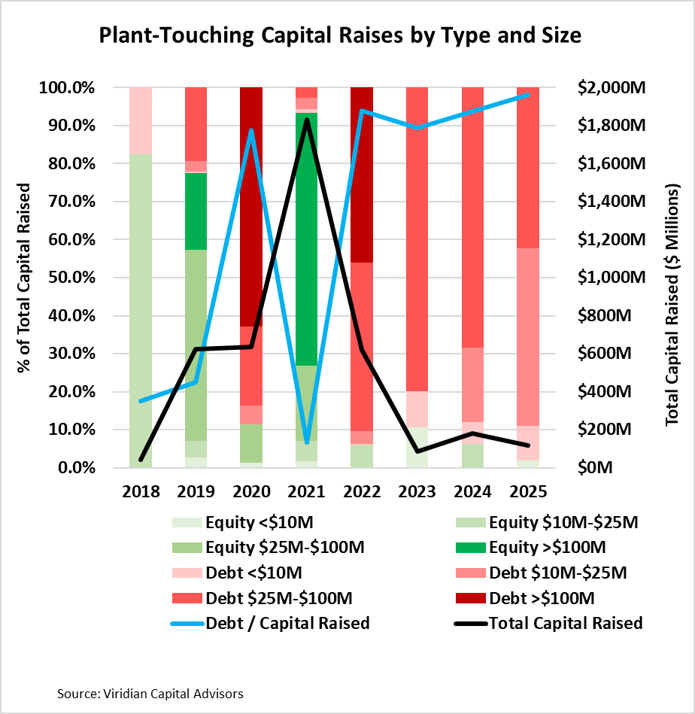

Viridian Capital Chart of the Week: U.S. CULTIVATION & RETAIL CAPITAL RAISES FOR THE FIRST 15 WEEKS OF 2025 ARE DOWN 35% FROM THE SAME PERIOD IN 2024 AND ARE VIRTUALLY ALL DEBT

- The Viridian Chart of the Week depicts the composition of U.S. Cultivation and Retail capital raises for the first fifteen weeks of 2025 compared to the same period in each of the previous seven years.

- The black line (measured on the right axis) shows the total capital raises for the sector in each period. Total tracked 2025 raises of $118.0M for the first fifteen weeks of 2025 are down 35% from $181.3M for the equivalent period in 2024. Caution is advised in interpreting the results of only a bit over ¼ of the year, as it would only take one or two large deals to skew the results significantly. Nonetheless, the year is not starting auspiciously. LTM results show a different picture, which readers are urged to review in our Weekly Deal Tracker. What doesn’t change, whether you are looking at the first fifteen weeks or LTM, is the dominance of debt in the sector.

- The red bars on the graph depict debt raises, and the shade indicates the size of the issue. Pink indicates raises of under $10M, and gradually deepening color indicates larger issue sizes. For the first time in the last eight years, the majority of capital raises for the first fifteen weeks were composed of debt issues of $25M or less.

- The blue line shows the percentage of capital raises that were debt. Debt made up 98.06% of all capital raises for the sector YTD and has accounted for over 90% of raises in each similar period since 2023.

- The green bars depict equity raises, and the sliver at the bottom of the 2025 column represents the $2.29M of YTD equity raises for cultivation and retail sector companies. For all intents and purposes, the equity market for plan-touching businesses is closed. Companies are reluctant to issue stock at prices they believe are below intrinsic value, and investors are suspicious of companies that would want to raise equity at current prices.

- The industry needs equity to repair overleveraged balance sheets. Our Credit Tracker release last week demonstrated that even very highly performing companies cannot sustain over 2.3x leverage in a 280e environment. However, nine of the fifteen companies we graph each week in the Tracker have higher than 2.3x leverage. Granted, many of them are acting like 280e doesn’t exist and running up tax liabilities on the theory that they will go away. Even assuming 280e is eliminated, there are at least five MSOs on our weekly graphs that are bumping against the 3.6x leverage we calculate is sustainable post 280e.

- There are great investment opportunities in the current market. Still, investors need to be comfortable that their portfolio investments can survive the current treacherous environment of slow growth, stretched consumers, declining margins, and limited capital availability. Consult the Viridian Deal Tracker for tools to avoid trouble.