OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Quick

Links

Past Charts

Home » Viridian Capital Chart of the Week: MSOs Are Trading Near Historically Cheap Levels

Chart of the Week

Chart of the Week

The Viridian Capital Chart of the Week highlights key investment, valuation and M&A trends taken from that week’s Deal Tracker that we believe are impactful for investors, companies and acquirers.

Week ended 08/30/2024

Viridian Capital Chart of the Week: MSOs Are Trading Near Historically Cheap Levels

-

- As of 8/30/24, cannabis equity prices have reverted to near their historical lows, driven by the DEA announcement of an ALJ hearing on December 2, 2024. The delay means that the ruling cannot go into effect prior to the election and probably not prior to year-end or even Spring. That conjures up the possibility that whatever 280e refunds MSOs might have received for 2024 may not happen, and the economic cost to the companies could be as much as 7% of the market cap based on our beginning-of-the-year analysis that calculated a $700M savings for the top 10 MSOs.

- Perhaps an even bigger fear is that if Trump wins, rescheduling and other reforms might be rolled back or canceled. We believe that Trump’s Saturday remarks supporting the Florida legalization and generally supporting cannabis decriminalization should go a long way toward reducing those fears.

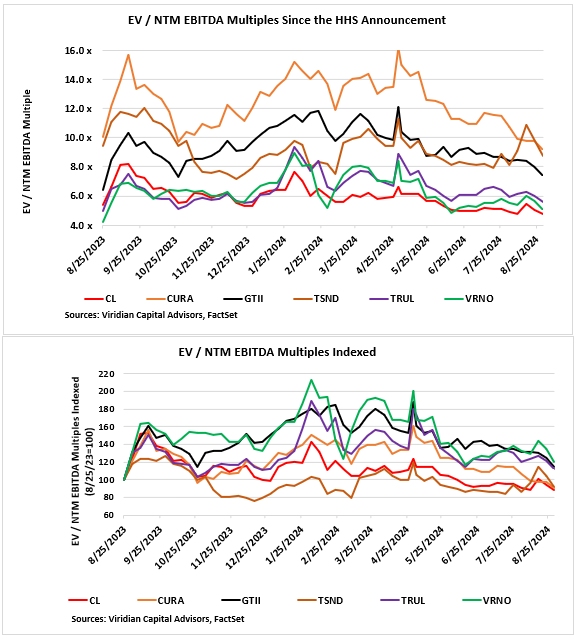

- The top graphs show EV / Consensus Next Twelve-Month EBITDA multiples for six of the top market cap MSOs from the Friday before the HHS announcement to the present. The top graph shows the multiples, while the bottom graph shows those same multiples indexed so that 8/25/23 = 100.

- After an immediate firm bump following the HHS announcement, most of the multiples fell through year-end of 2023. Multiples rose sharply in early 2024 and peaked on 4/30/24 when the DEA announced that it agreed with the recommendation for S3. Unfortunately, prices and multiples have drifted lower ever since, with a particularly nasty downturn following the recent DEA announcement.

- The bottom graph shows EV/ NTM multiples indexed so that 8/25/23 = 100. The graph shows that three of the six MSOs, Cresco (CL: CSE), Curaleaf (CURA: TSX), and TerrAscend (TSND: TSX), are now trading at lower multiples than they were prior to the HHS recommendation for Schedule 3. The three MSOs showing multiple expansions over the period have gained between 12.5% (Trulieve) and 19.9% (Verano), far less than the doubling we had expected as S3 ground its way through the system.

- We still firmly believe that S3 will still be put into effect with all of the benefits it initially promised, albeit at a slower pace than we initially expected. For the first time in history, we appear to have two presidential candidates who are both advocating cannabis regulatory and legal reform. That historical precedent should not be minimized. S3 is only a starting point, however, and we are disappointed that the positive political rhetoric has not extended to a revival of the SAFER Act, another necessary step toward normalization.