OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Quick

Links

Past Charts

Home » Viridian Capital Chart of the Week: Lenders vs. Borrowers – the Wisdom of Diversification

Chart of the Week

Chart of the Week

The Viridian Capital Chart of the Week highlights key investment, valuation and M&A trends taken from that week’s Deal Tracker that we believe are impactful for investors, companies and acquirers.

Week ended 06/14/2024

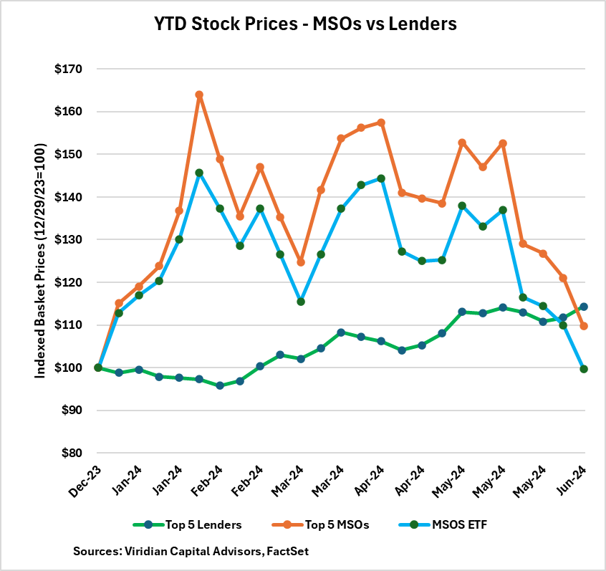

Viridian Capital Chart of the Week: Lenders vs. Borrowers – the Wisdom of Diversification

- The chart shows the YTD stock performance of two equally weighted baskets of stocks. The orange line depicts the YTD performance of a basket of the top five MSOs by market cap: Curaleaf, GTI, Trulieve, Verano, and Cresco. The green line shows the YTD results of a basket of the top five cannabis lenders and sale-leaseback providers: IIPR, Chicago Atlantic, AFC Gamma, NewLake Capital, and Silver Spike.

- The blue line shows the MSOS ETF’s YTD performance. Note that the MSOS ETF price has a .97 correlation with the price of a simple equal-weighted basket of the top five MSOs but significantly underperforms the basket due to administrative expenses.

- On a YTD basis, the 14.7% YTD return on the lender group outpaced the 9.75% return on the MSO basket and significantly exceeded the 0.25% loss on the MSOS ETF. Both the MSO basket and the MSOS ETF have dropped for four consecutive weeks.

- The slow and steady rise of the lender group basket vs. the wild ride the MSO group has experienced is rooted in the fundamental nature of the two bets. We continue to believe that a doubling of MSO prices is likely as the full impact of rescheduling is realized, but we do not expect that the lender group will double. Lenders will benefit strongly, however, from the improved credit profile of their portfolio companies and the NPV boost to loan portfolio values from an expected reduction of cannabis borrowing rates.

- The relative volatility of MSO and MSOS ETF prices vs the lender group also has a lot to do with the nature of the respective investor groups. The MSOS ETF is primarily owned by retail investors who are unable to purchase the underlying stocks. There is an underlying get-rich-quick, momentum basis of investment that is often devoid of fundamental investment rationale. When that is matched with the tremendous illiquidity of the underlying assets, wild swings are bound to occur. Throw in the role of algorithmic trading programs to complete the casino trading atmosphere.

- The lender group, primarily trading on senior exchanges, is owned by institutional investors, who do serious fundamental analysis. The group has been successful at extricating itself from a number of credit issues, and while land mines may still exist in the portfolios, they appear manageable.

- Investors would be wise to diversify their cannabis bets. The lower risk, more liquid lender basket has produced a 28% annualized return YTD, and some participation in the sector belongs in most cannabis investment portfolios. Similarly, we recommend direct investments in the underlying debt positions of the MSOs, producing low teens to low twenty percent yields.

- While we are still firm believers in the MSO upside thesis, there is wisdom in portfolio diversification.