OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Quick

Links

Past Charts

Home » Viridian Capital Chart of the Week: Debt Raises Decline as Effective Cost of Capital Increases

Chart of the Week

Chart of the Week

The Viridian Capital Chart of the Week highlights key investment, valuation and M&A trends taken from that week’s Deal Tracker that we believe are impactful for investors, companies and acquirers.

Week ended 07/21/2023

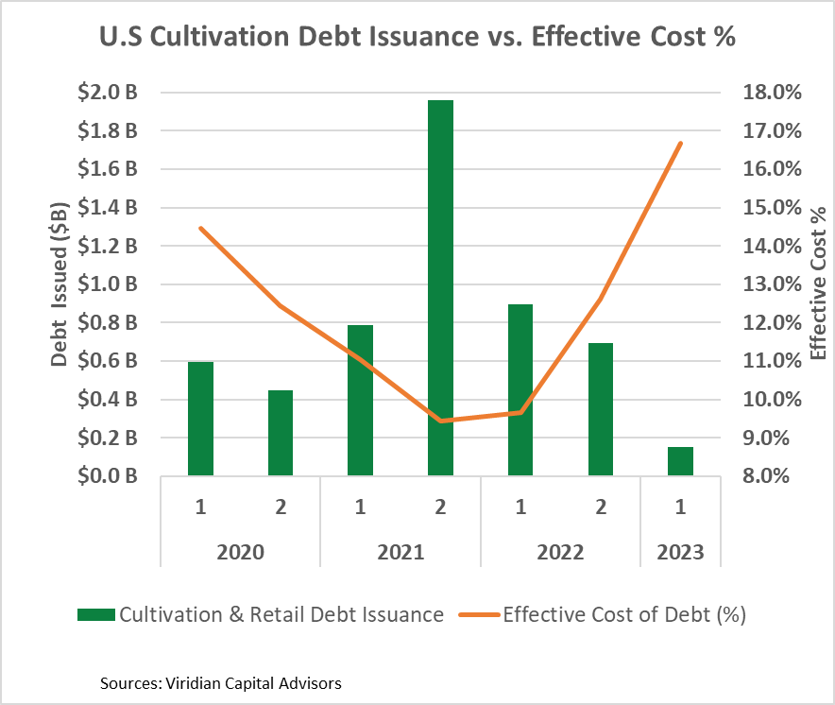

Viridian Capital Chart of the Week: Debt Raises Decline as Effective Cost of Capital Increases

- This week’s chart explores the relationship between U.S. Cultivation & Retail sector debt issuance and effective costs of debt.

- Cannabis companies issued a record amount of debt in 2021, including six of the ten largest debt deals in U.S. cannabis history. The pace declined in 2022, but low debt costs and strong access to debt capital kept the spigot open. The first half of 2023, however, has seen a sharp reduction, with sequential quarter issuance down 78%.

- There are several reasons for the downturn in debt issuance:

- MSOs have reduced capital spending and cash used in acquisitions in response to challenged capital markets.

- Many MSOs have essentially maxed out their debt-carrying capacity. Ten of the nineteen MSOs, with market caps over $5M and sell-side analyst coverage, now have more than 3x debt/ 2024 consensus EBITDA. Viridian estimates debt higher than 3x EBITDA is difficult to sustain in a 280e world.

- Also, as the orange line on the graph indicates, the effective cost of debt has risen significantly since the first half of 2022, making debt less attractive to issuers.

- Viridian calculates the effective cost of debt issues in a manner that puts all debt structures on an even basis. We explicitly value the embedded options in convertible debt and debt with attached warrants. We subtract that value and any OID from the debt’s principal before calculating a new yield, which we term the effective cost.

- The obvious reason for the rise in effective cost is the underlying rise in market interest rates. Another less recognized component is the rise in the percentage of debt with equity-linked features. Nearly 52% of the debt issued in the first half of 2023 had equity links compared to 5.5% and 5.7% for the first and second halves of 2022, respectively.

- The cannabis industry needs a re-equitization to maintain its growth rates. However, the delay in any meaningful reform in Washington is putting a freeze on this activity. Investors have become skeptical that SAFE is anything besides political football, and they are afraid of getting bagged again. Meanwhile, no CFO wants to be the guy that sold stock at the absolute bottom of the market only to have some catalyst like SAFE run his stock up by 50% or more. That reasoning led to a lot of debt issuance, but only a few companies currently have significant excess debt capacity.

- A few brave companies, including TerrAscend (TSND: Nasdaq)(TRSSF: OTCQX) and Ascend Wellness (AAWH.U: CSE)(AAWH: OTC) have tiptoed into the equity market in the last couple of weeks, and both have excellent reasons to raise equity. Otherwise, only the liquidity starved or those with very high IRR projects will likely enter the capital market soon.