OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Quick

Links

Past Charts

Home » Viridian Capital Chart of the Week: Are There Good Values Among Canadian Cannabis Companies?

Chart of the Week

Chart of the Week

The Viridian Capital Chart of the Week highlights key investment, valuation and M&A trends taken from that week’s Deal Tracker that we believe are impactful for investors, companies and acquirers.

Week ended 07/28/2023

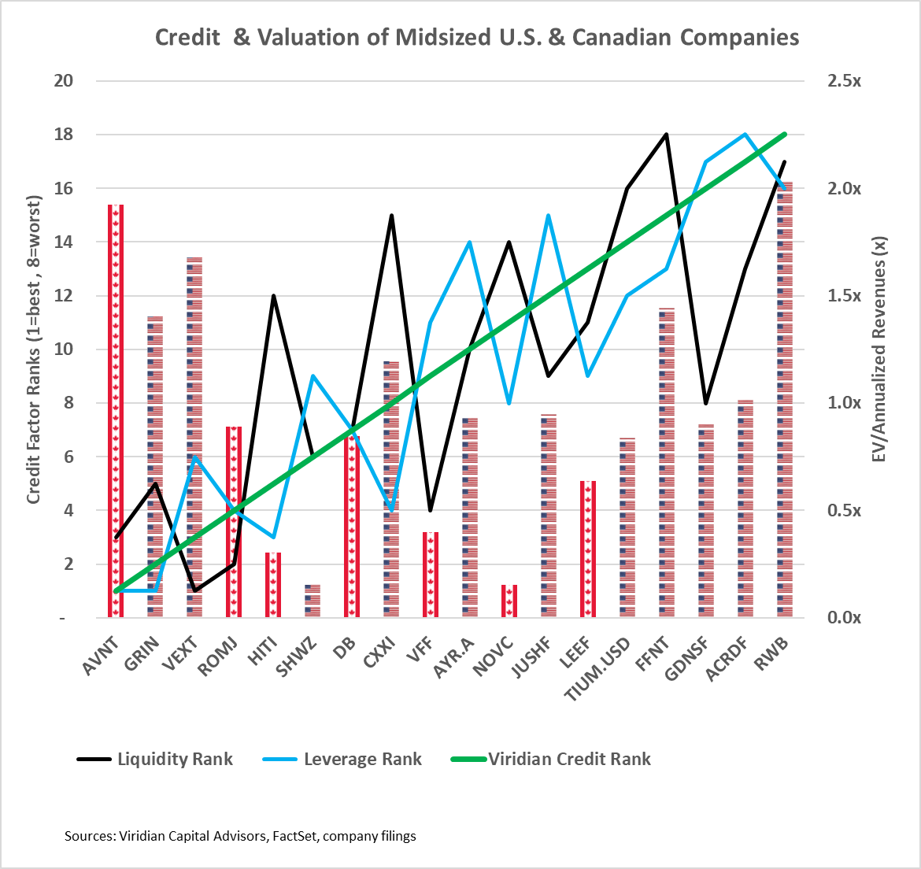

Viridian Capital Chart of the Week: Are There Good Values Among Canadian Cannabis Companies?

- This week’s chart explores the valuation and credit of the eighteen U.S. and Canadian cannabis companies with market caps between $20M and $100M. The presence of U.S. and Canadian companies in the group allows for comparing credit quality and valuation.

- The bars show enterprise value to annualized revenue. The green line shows the Viridian Capital model credit ranking, the black line depicts the Viridian Capital liquidity ranking, and the blue line represents the Viridian Capital leverage ranking. The graph is arranged with the best-ranked credits on the left.

- Surprisingly, given most investors’ negative perception of the Canadian cannabis industry, five of the top-ranked companies by credit quality are Canadian.

- Avant Brands (AVNT: TSX)(AVTBF: OTCQX) ranks as the top credit quality company in the group. The company has excellent liquidity with a cash flow adjusted current ratio of 2.49x as of its April quarter end and 2.78x proforma for its recent $2.65M credit facility. Leverage is the third lowest of the group thanks to its 2nd place total liabilities to market cap and funds from operation to total liabilities. AVNT has four consecutive quarters of positive cash flow from operations and adjusted EBITDA. The only rub is that it is priced for growth with the second-highest enterprise value to annualized sales of the group (1.95x). Still, the company was proactive in blowing out the stale inventory it acquired in its February acquisition of FLOWR out of Canadian bankruptcy. It stands to gain from the increased production capacity, which will now be oriented towards AVNT’s fast-selling premium flower.

- Rubicon Organics (ROMJ: TSX)(ROMJF: OTCQX) is another reasonable-looking Canadian operator from a credit point of view. The company has strong liquidity, low leverage, positive adjusted EBITDA, and cash from operations. Knocks on the company include its #13/18 profitability ranking and its minimal size (Total assets= $40m. Market cap=$21M). Still, ROMJ is priced at only .9x annualized sales.

- High Tide (HITI: Nasdaq)(HITI: TSX) trades at .3x annualized revenues and 4.0x annualized adjusted revenues. The company’s thin 7.5% EBITDA margins are somewhat concerning as it is low liquidity with a free cash flow adjusted current ratio of only 1.08x. Still, the company’s leverage on both a market basis and funds from operations/ liabilities basis are amongst the best of the group.

- Decibel Cannabis (DB: TSX)(DBCCF: OTCQX) ranks as the seventh strongest credit of the group due to its 7th ranking in leverage and liquidity. Decibel has been gaining market share and is now the 2nd largest Canadian LP by market share. Its solid profitability (EBITDA margin of 25%), positive cash from operations, and free cash flow make it worthy of consideration at its trading value of .85 EV/ annualized revenues.

- There are several attractively priced Canadian cannabis companies with solid credit quality. Investors should look to diversify with a small allocation in these smaller solid Canadian players.