OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Quick

Links

Past Charts

Home » Viridian Capital Chart of the Week: Analysts Expect Higher 2025 MSO EBITDAs But Do the Sharp 4th Quarter Downward Revisions Tell the Real Story?

Chart of the Week

Chart of the Week

The Viridian Capital Chart of the Week highlights key investment, valuation and M&A trends taken from that week’s Deal Tracker that we believe are impactful for investors, companies and acquirers.

Week ended 12/27/2024

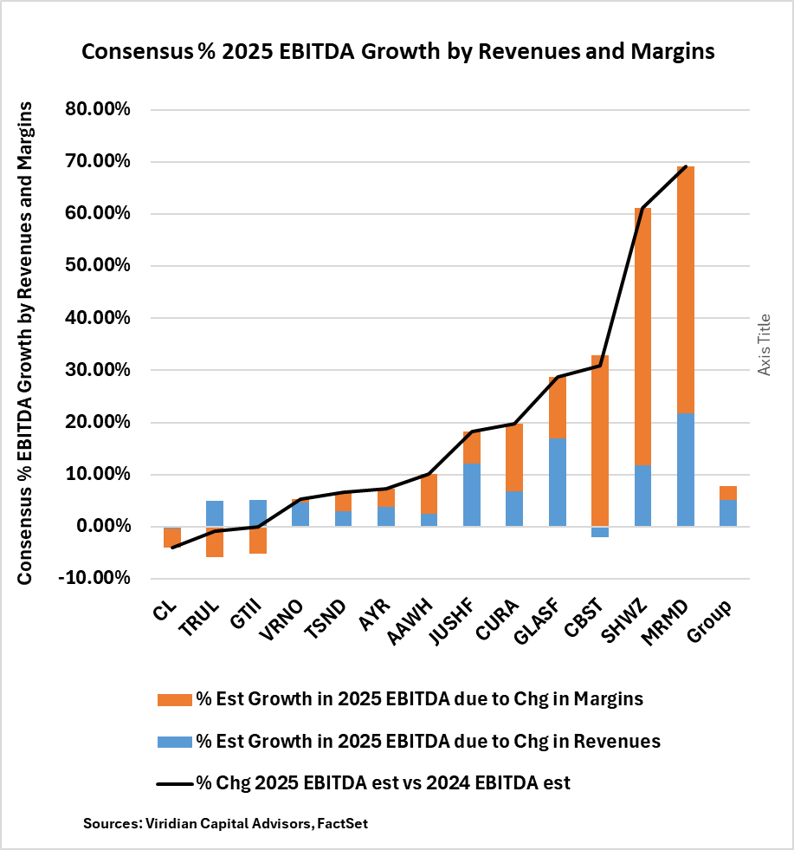

Viridian Capital Chart of the Week: Analysts Expect Higher 2025 MSO EBITDAs But Do the Sharp 4th Quarter Downward Revisions Tell the Real Story?

- MSO stocks are trading near all-time lows, and social media stories are swirling about the debt maturity “tsunami” approaching in 2026. Against this backdrop, it would be natural to assume that the 2025 EBITDA estimates were lower than 2024.

- Recent sharp downward revisions would support this negative impression. Eleven of the thirteen companies on the chart had negative 2025 EBITDA revisions in Q4: 24, ranging from -5.1% for Green Thumb (GTII: CSE) to -30.7% for Glass House (GLASF: OTCQB). Only two MSOs had positive changes: Trulieve (TRUL: CSE) (3.1%) and Schwazze (SHWZ: OTC)(13.7%). Analysts cut 2025 EBITDA estimates for the group by 7.6%.

- Still, despite these 4th quarter cuts and other significant reductions throughout 2024, analysts remain bullish on 2025.

- The graph shows the projected % 2025 EBITDA gains, decomposed into the portion attributable to revenue growth vs. the component due to margin increases. Ten of the thirteen companies show EBITDA increases in 2025, aggregating 7.9%. Approximately 5.1% of this increase was due to increased revenues, while 2.8% was attributable to increased margin.

- The four companies on the left side of the graph demonstrate the critical issues of 2025: modest revenue growth, challenged by ongoing margin pressures. Pennsylvania is the only large population state that has any significant potential for adult rec in 2025 to provide a boost to growth. However, ongoing wholesale price compression is exacerbating overall weakened consumer demand. MSOs have made great strides in cutting costs, reducing working capital, and economizing on capital spending. But how much more blood can be squeezed from the turnip? Rescheduling should free up cash flows for high IRR investments that can boost margins, but the timing is still uncertain.

- The companies on the right-hand side, including Cannabist, Schwazze, and Marimed, are bouncing back from pretty horrific results in 2024. Still, overall, they are too small to swing the industry dynamics much. Two large competitors, Curaleaf (CURA: TSX) and Glass House (GLASF: OTCQB), show both solid revenue and margin growth that bear monitoring.

- We have all seen how the sell-side analyst game works. Analysts cut their forecasts for 2025, but was it enough? Analysts are jealous of their relationships with corporate management and are reluctant to cut their projections too aggressively, so instead, it becomes the death of 1000 cuts. We want to be more optimistic, but we see little in the macro picture to suggest either a return to robust growth or a marked resurgence in margins.

- Absent significant changes in Washington that go beyond S3, we expect further weakness ahead. Margins are projected to growth by less than 1 point, but in the current environment, we would be happy with that.