OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

- Best & Worst Perfromers

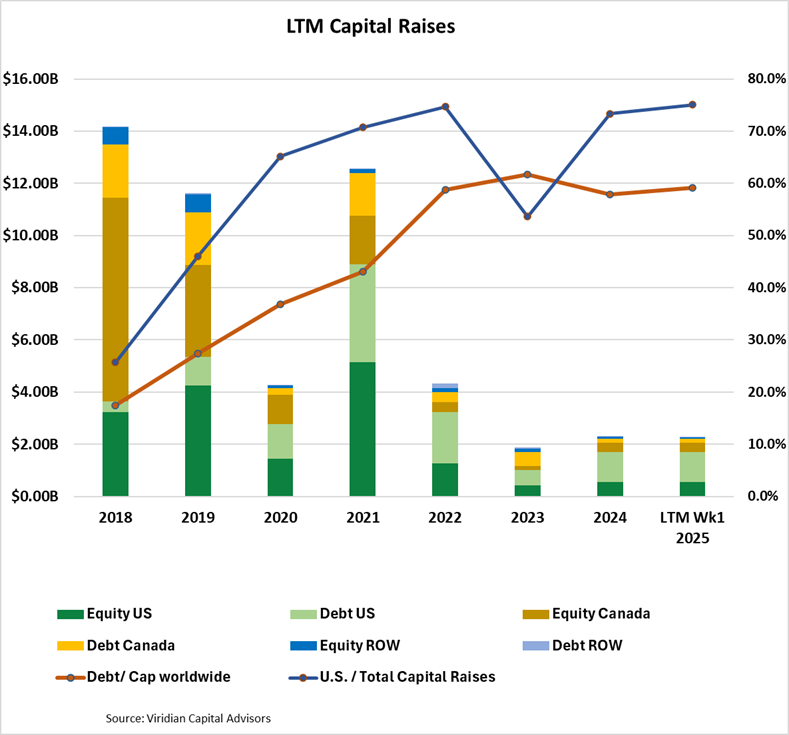

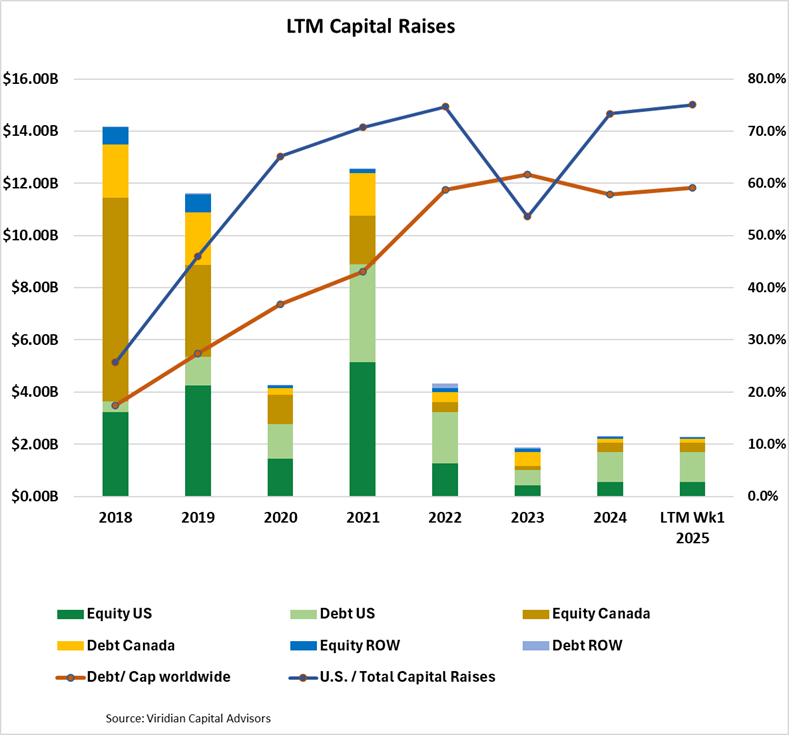

- LTM capital raises total $2.27B, down -2.1% from the same period in 2024. Debt as a percentage of capital raised on a worldwide basis remained steady at 59.1%, compared to 57.8% last year. U.S. raises accounted for 71.2% of total funds, up from 58.2% at the same point in 2023. Raises from outside Canada and the U.S. represented 2.3% of the total funds raised, falling short of the average of 5.33% in the six previous years.

- Raises by public companies accounted for 79.76% of total raises in the LTM period, the highest since 2021.

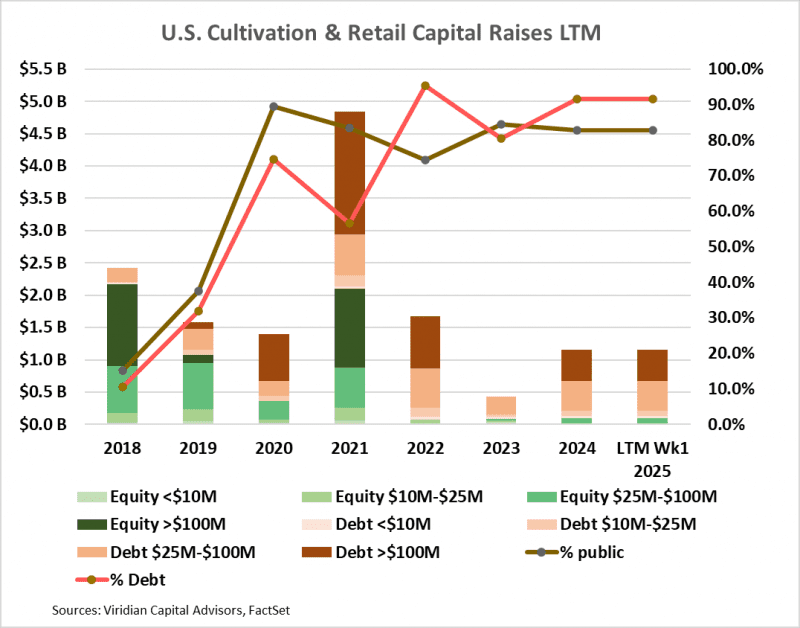

- Cultivation and retail sector capital raises are up .2% in the LTM period vs 2024, which in turn was up 170% from 2023.

- Debt accounts for 91.5% of funds raised in the LTM period. Large debt issues (>$100M) represented 41.9% of capital raised compared to zero in 2023.

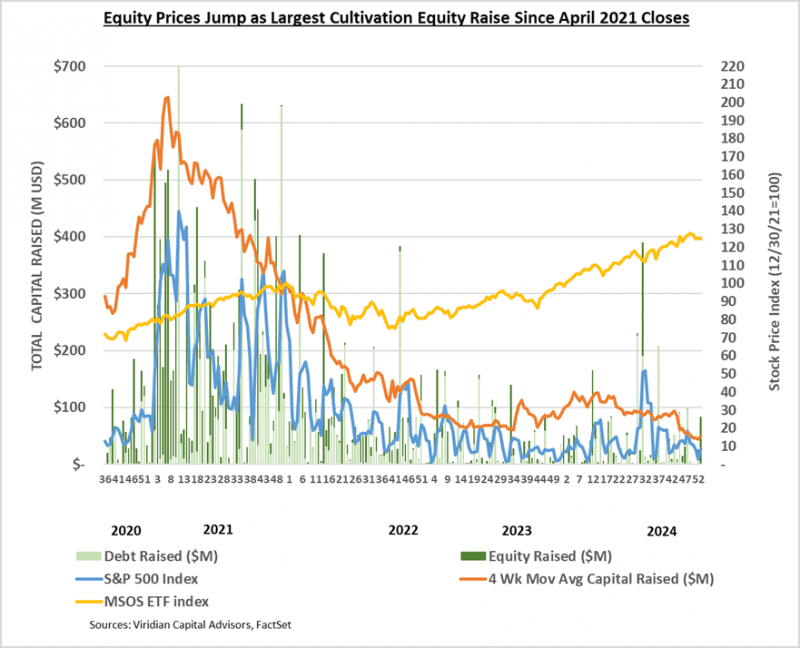

- Cannabis equity prices (as measured by the MSOS ETF) rose 8.87% for the week, bouncing off all-time lows.

VIRIDIAN INSIGHTS

- REVIEW OF OUR 2024 PREDICTIONS AND NEW PREDICTIONS FOR 2025

-

- 2024 RECAP

- We are relatively pleased with our predictions on the regulatory front, although we wish we were wrong. In our January 5th issue, we said,

- “THE DEA WILL GO ALONG WITH RESCHEDULING TO LEVEL 3. However, the process may take longer than widely expected with public hearings and likely court appeals.” We doubted S3 would be enacted by the election.

- “The SAFER ACT, HOWEVER, WILL CONTINUE TO STRUGGLE. WE HAVE DOUBTS THAT IT WILL BE ENACTED IN 2024”

- We were overly bullish on growth and margin gains for 2024, calling the projected 6.2% growth for the top ten MSOs “a bit cautious.” We also thought the 25.7% EBITDA margin expectations were “too low.” It turns out revenue growth was virtually zero, and the projected margins were spot-on.

-

-

- We correctly predicted, “THE CANNABIS CAPITAL MARKETS WILL SEE A MODEST RESURGENCE.” Indeed, capital raises were up for 2024, particularly for plant-touching company debt issues. However, we believed that as S3 got closer, we would see an uptick in stock prices that would elicit equity issuance and debt reduction. Boy, were we wrong on that front! We failed to fully understand the immense investor skepticism that would mean that “close doesn’t count.” Investors want to hear the coin hit the bottom of the cup with regard to S3 and any other cannabis regulatory or legal reforms.

- We were also off in our predictions that cannabis debt securitization would take off in 2024. The Pelorus deal convinced us that more similar deals would be upcoming. We are now a bit more sophisticated regarding the topic. It will probably take a strong version of the SAFER Act to get rating agencies to rate cannabis debt, a key gating item for future progress on this front.

- Finally, our worst prediction: “CANNABIS M&A WILL BOUNCE BACK FROM ITS LOWEST YEAR EVER IN 2022.” Instead, it set a new record low! We are encouraged, though, by the announced Vireo deal and the completion of the Cansortium/RIV transaction.

-

-

- 2025 PREDICTIONS

-

- More US MSOs will follow Curaleaf and GTI into hemp-derived THC beverages. It took the benefits of the hemp-derived THC product to ignite the beverage category. Still, the advantages are inescapable, from production economics(no seed-to-sale tagging/tracking) to distribution (nationwide DTC sales!) With the Farm Bill on hold for at least another year, look to see most of the holdouts jump in.

- S3 will be enacted, probably close to the end of 2025, but SAFER will continue to struggle. The S3 train is still on the tracks and doesn’t require much action from DC. However, the impacts are likely to be felt less strongly than initially anticipated. Many MSOs are already taking the cash flow bonanza of 280e elimination by just not paying their 280e taxes. The actual removal of 280e will undoubtedly produce a celebration and sigh of relief, but much of the cash flow benefits are already in the financial statements.

- Meanwhile, the remarkable rise of cannabis to the level of national discussion is likely to fade. The election and any attendant political mileage are past. Cannabis has never been a vote generator, and no Congressmen fear any repercussions from ignoring cannabis.

- M&A will see a resurgence but it will be intrastate focused. The difficulties of dealing with license overlaps and competing cultures will continue to stall any more significant public/public transactions. Still, deals within states like Michigan and Missouri will continue to grow.

- Consolidation in developed markets may finally begin to slow price compression. We liken cannabis to the airline industry: both have perishable commodity products with high fixed costs and exit barriers, leading to brutal price competition and credit degradation. Cannabis suffers from an additional problem- virtually perfect substitutes from hemp-derived intoxicants and the illicit market. Ask yourself what changes in airlines have shored up the industry—our answer – is consolidation. Cannabis will and must consolidate, and the consolidation within state markets we are seeing now is the most important as it will lead to rationalization of capacity and oligopolist pricing rigor.

- MSOs will get an early start on managing 2026 debt maturities. With a finite amount of capital available, astute management will not want to wait until 2026. We expect a brisk year of refinancings in 2025, most of which should go smoothly. Recent Viridian publications have highlighted companies with a market-implied asset value of less than liabilities and those with particularly large refinancing needs relative to their market caps.

-

-

- PHARMACANN VS IIPR – LET THE GAMES BEGIN

- On December 19, 2024, PharmaCann defaulted on its obligations to pay rent for December under six of its eleven leases with IIPR for properties located in Illinois, Massachusetts, Michigan, New York, Ohio, and Pennsylvania.

- Although PharmaCann paid December rent in full (totaling $90,000) under its other five leases with IIPR (all retail locations), as a result of cross-default provisions, the company was also in default under these leases.

- IIPR said what you would expect them to say: “continuing discussions with Pharma Cann regarding the Leases and expects to enforce its rights under the Leases aggressively, which may include, but is not limited to, commencing eviction proceedings as IIP deems necessary.”

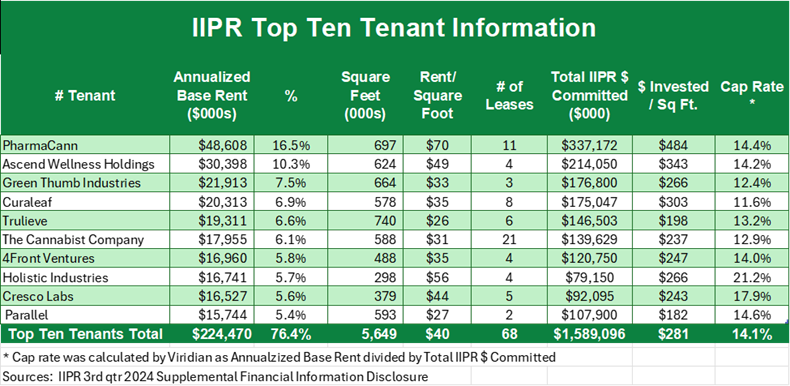

- Information from IIPR’s 3rd quarter financial supplement gives us some interesting data points:

-

- Can PharmaCann argue that it is paying excessive rental rates? The chart above clearly shows that PharmaCann’s base rent per square foot of space is the highest of the top ten IIPR tenants by a considerable margin. Does this mean they are being overcharged?

- Not so Fast! Yes, PharmaCann is paying the highest rent/sq ft, but the table above also shows that IIPR has the largest invested dollars per square foot in the PharmaCann leased properties.

- Viridian calculated an approximate average cap rate by dividing the total annualized base rent by the IIPR committed investment for each tenant. On this basis, PharmaCann’s cap rate of 14.4% is higher than the average but only the fourth highest of the ten. Note: Cannabist’s low cap rate of 12.9% is probably due to the fact that nearly 30% of the IIPR’s committed investment on Cannabist properties are for retail locations that generally carry lower cap rates.

- Why is PharmaCann so out of line on Investment / Sq ft.? Approximately 38% of IIPR’s investment in PC properties is accounted for by a $139.5M, 239k sq ft facility in Hamptonburgh, NY. This facility was acquired In 2016 at $596/ sq ft! Another 9% of investment is attributable to a Massachusetts facility at $526 per sq ft that was acquired in 2018. The real story seems to be that back in the heady days of 2016-2018, PharmaCann and IIPR did a few deals at prices that, in retrospect, seem crazy. In their defense, the state markets in question seemed poised for massive expansion and the term “wholesale price compression” had not yet entered the vocabulary. Both IIPR and PC agreed to terms that do not work in 2024, as the lease rates on these properties arguably prevent anyone from being profitable in the context of current prices and operating costs. PC has already shut down the Michigan facility; it is probably losing money in MA, and NY needs significant rental reductions to make sense.

- SO WHAT NOW?

- From IIPR’s point of view: In q3’24, IIPR’s Adjusted Funds from Operation (AFFO) of $64.3M was $2.25 per diluted share. IIPR paid a $1.90 dividend amounting to 84% of AFFO/sh. (note this payout ratio has gone up for each of the last 4 quarters). PharmaCann’s quarterly lease payments are approximately $12.2M, which means that if IIPR cannot quickly resolve this issue, it may have to reduce its dividends.

- Similarly, if IIPR evicts PharmaCann, significant lease rate haircuts are likely to be required to get new tenants into the facilities. The process also has an uncertain time horizon, potentially requiring dividend cuts.

- Selling the properties, even to a cannabis buyer, would require massive write-offs. If IIPR were able to sell the properties at $300/sq ft (higher than its average of $281), it would incur a $128M loss. Much of this pain has already been taken in the stock price reduction.

- From PharmaCann’s point of view: Loss of the NY facility would likely cost the company its RO status, and the impact of the loss of the entire cultivation portfolio would probably result in the company’s liquidation.

- PharmaCann likely needs to bargain for lower lease rates and possibly a deferral of near-term lease payments. PharmaCann’s financial picture is unknown, but if the company is to continue operations, it must agree on at least the bulk of these properties. If Chapter 11 were available to cannabis companies, a likely scenario would be that the company would reject several of the leases where the economics do not make sense. Unfortunately, that option is not available in court, but perhaps some variant of it will enter the negotiations.

- THE MOST LIKELY SCENARIO IS THAT THE PARTIES COME TO A NEGOTIATED SETTLEMENT.

- IIPR will likely have to offer both lower base lease rates and some deferral of payments.

- In return, PharmaCann may need to offer equity warrants as an incentive. PC may also need to extend the maturities of the leases, offering IIPR more time to amortize its losses.

- WILDCARD? CRONOS. In 2021, Cronos paid approximately $110M for options to acquire around 10% of PharmaCann, exercisable when regulatory changes enabled this ownership. Cronos is still cash-rich and may cut some deal to take a more significant future stake in PC through more options or a Canopy USA type structure. This would only be a possibility in the context of negotiating lower lease rates that shore up the profitability of PC.

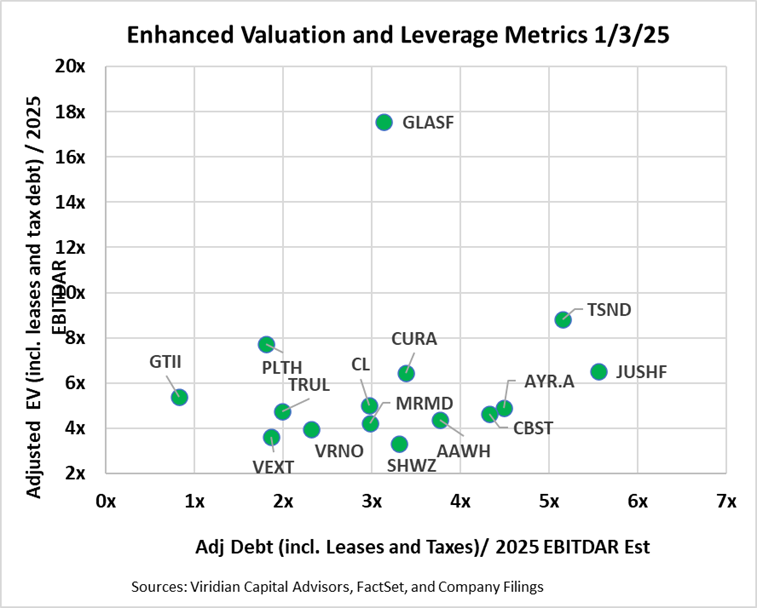

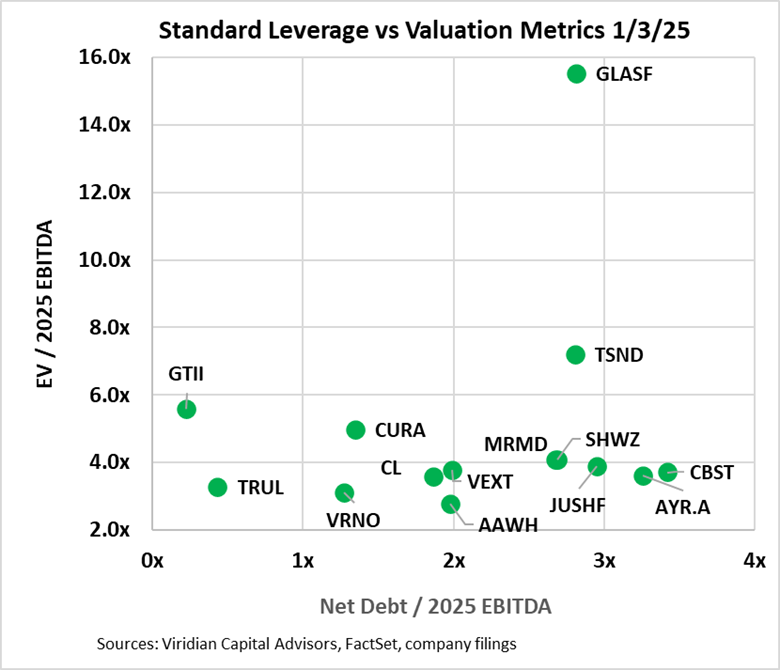

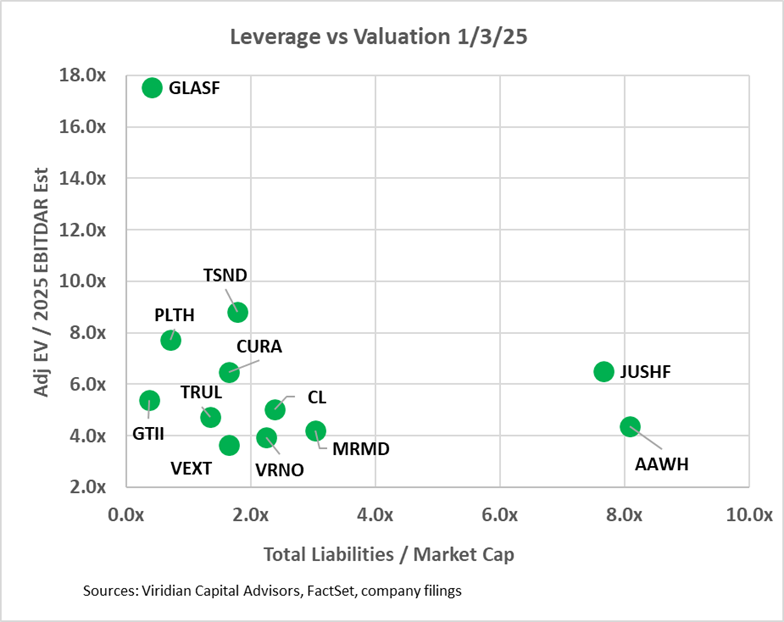

- MSO VALUATION AND FINANCIAL FLEXIBILITY DEPICTED BY FOUR GRAPHS. BOTTOM LINE: MSOs ARE TRADING AT HIGHER VALUATION MULTIPLES AND HAVE HIGHER LEVERAGE THAN STANDARD MEASURES INDICATE!

- The four graphs below seek to map the financial options available to eighteen of the largest MSOs based on their Valuation, Leverage, and Liquidity. We have updated our measures to look at 2025 EBITDAR estimates as we believe most investors are now looking to these values in their valuations.

- The first two graphs present different versions of EV/EBITDA on the vertical axis and Debt/EBITDA on the horizontal axis.

- The first graph presents our latest view of the most appropriate valuation and financial statement-based leverage metrics: Adjusted E.V. / 2025 EBITDAR and Adjusted net debt / 2025 EBITDAR. In calculating Adjusted Net Debt, we make several key assumptions: 1) Leases that are included on the balance sheet are considered debt. We view most leases in the cannabis space as equivalents to equipment loans or mortgage loans. While it is true that a lease default does not necessarily trigger a cascade of events leading to bankruptcy, the distinction is often meaningless in cannabis due to the mission-critical nature of many long-term leases and the absence of bankruptcy protection in cannabis. 2) We consider any accrued taxes (including uncertain tax liability accounts listed as long-term liabilities) in excess of the most recent quarterly tax expense to be debt. Our calculation of enterprise value is now market cap plus debt plus leases plus tax debt minus cash. We now use EBITDAR rather than EBITDA since lease expense is taken out prior to EBITDA.

- The second graph utilizes EBITDA and employs the traditional calculations of both debt and enterprise values, leaving out leases and taxes.

- Our adoption of new metrics tends to make the companies look less cheap and more leveraged.

- Surprisingly, nine of the companies on the enhanced metric chart are still above 3x leverage, which we have identified as the boundary of sustainability in a 280e environment. Four companies now exceed 4x leverage, which we believe will be close to the maximum sustainable post 280e.

- Jushi and TerrAscend appear as leverage outliers using the new metrics relative to AYR and Cannabist, which seemed more leveraged using standard measures.

- TerrAscend and, particularly, Glass House are valuation outliers. We have been positive on Glass House for quite a while, but the multiple spread to the nearest competitor is straining our resolve. We note GLASF’s $25M at the market equity issuance facility as another factor likely to restrain price appreciation.

- The third graph looks at leverage through the lens of total liabilities to market cap. We believe this is the single best measure of leverage because it is a direct reflection of the market’s assessment of the value of a company’s assets in excess of its liabilities and is sensitive to changes in market perception of a company’s future.

- On the bottom left are companies with Adj E.V./2025 EBITDAR of under 7x and total liabilities to market cap under 2x. The group includes Vext, GTI, Trulieve, and Curaleaf. Companies in this quadrant are right to consider stock repurchases or using cash in acquisitions. They can afford some additional debt and can take advantage of the ongoing dislocation in equity prices.

- In the middle, between 2x and 5x total liabilities/market cap, we see Verano, Cresco, and MariMed.

- On the right lies Jushi and Ascend. Ascend has now entered our high-risk zone of over 10x. AYR, 4Front, Cannabist, and Schwazze are now off the chart to the right, signaling pronounced credit risk. Our recent work using option modeling of equity prices showed that the market believes each of these companies has significantly less asset value than liabilities.

-

-

- The fourth graph introduces the free cash flow adjusted current ratio liquidity measure into the mix. Companies with less than 1x on this measure will likely have to raise capital next year. Surprisingly, eight of the companies fall into this bucket (including Schwazze, not pictured).

- The bottom left group, including Curaleaf, Verano, and TerrAscend, has low leverage but is below the critical 1x liquidity level. Companies in this range should consider taking advantage of the robust debt market to bolster liquidity.

- On the top left, we find companies with adequate liquidity and low market leverage, including both GTI and Planet 13.

- Companies in the lower middle-to-right generally have constrained liquidity and high leverage, a potentially dangerous combination in a capital-constrained environment. Aside from Curaleaf, Verano, and TerrAscend, mentioned above, seven other companies have less than 1x free cash flow adjusted current ratios, including Schwazze, AYR, Jushi, Cannabist, Ascend, and 4Front. These companies are high-risk with both high market leverage and low liquidity.

-

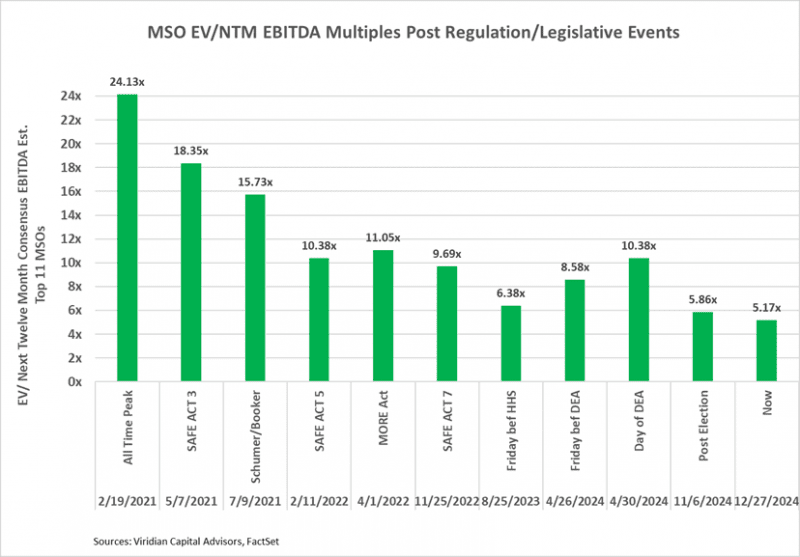

- EV/LTM MULTIPLES ARE NOW LOWER THAN BEFORE THE ORIGINAL HHS RESCHEDULING ANNOUNCEMENT ON 8/30/23

- We continue to believe that at current levels, U.S. MSOs have enormous upside potential. The graph below shows the multiples reached after a number of past legislative/regulatory events. It makes clear that a doubling of prices is a reasonable assumption. We recommend a balanced portfolio that leans toward the companies in the top half of the Viridian Credit Tracker model ranking.

- Despite the challenges to growth discussed above, we believe that many companies have become stupidly cheap. We recommend a “don’t step in the doggy do do” strategy. With refinancing risks made worse by cratering stock prices, this is no time to be a hero. Focus on building a diversified portfolio of companies ranked in the top 10 in our credit rankings. Put them in your portfolio and follow the total liabilities to market cap indicator that we recommended several weeks ago, as well as the credit tracker rankings. And resist the urge to look at the stock prices every day!

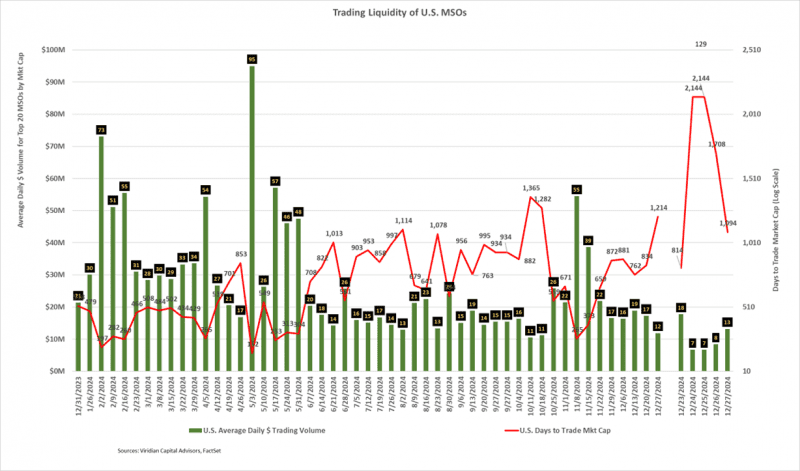

- MSO STOCK LIQUIDITY IS TRENDING LOWER

- The average daily dollar volume of $12M for the week ending 12/27/24 is lower than recent periods and corresponding weeks last year.

- The Days to Trade Market Cap (DTTMC) series depicts the number of days it would take to trade the market cap of a stock or group of stocks. The current DTTMC of 1214 implies that an investor who acquired a 5% position in the stock, assuming he wanted to be less than 25% of the average daily dollar volume, would require 243 days to trade out of his position. Of course, some of this is seasonal, and we will take a more careful look once the market is in full swing in 2025.

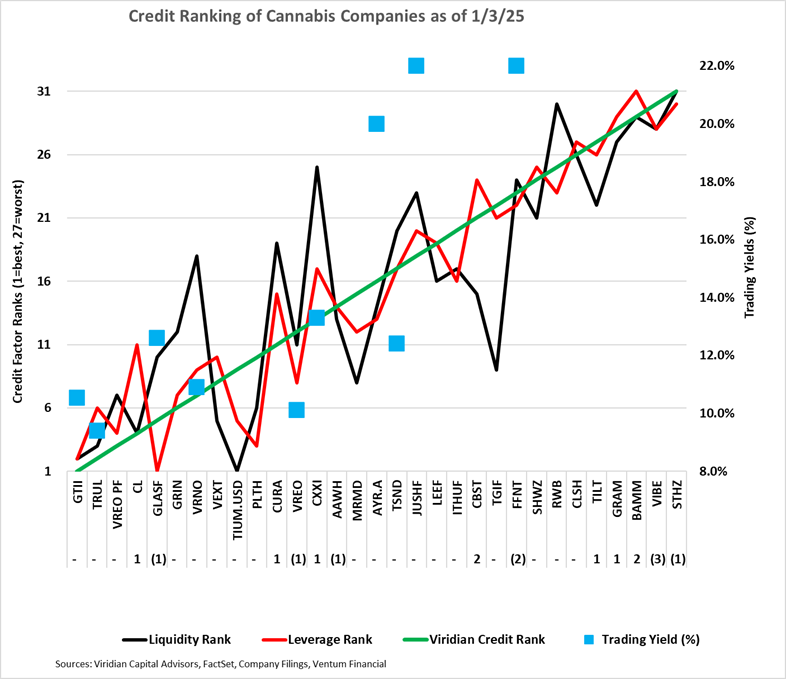

- GIVING CREDIT WHERE CREDIT IS DUE

- The chart below shows our updated 12/27/24 credit rankings for the 31 U.S. cannabis companies with over $3M market cap. The number below the ticker symbol indicates the change in credit ranking since last week, where a negative number suggests credit deterioration, while a positive indicates improvement.

- The blue squares show the offered-side trading yields for each Company. The prices shown have become a bit dated, so we will consider them only indicative. We expect updated pricing to reflect the dislocations observed in the equity market.

- We have replaced Acreage with Vibe at the beginning of this week.

- AYR has become the poster child of the 2026 debt “tsunami.” We generally don’t think the 2026 issues are nearly as severe as the press has made out, but AYR may be an exception. There are no near-term debt triggers because the company’s maturities have substantially been pushed out to December 2026. However, the approximately $300 million of 2026 maturities now represent 3.7x the company’s market cap, compared to 1.1x on 11/1/24. The 3.7x exceeds the level of maturity AYR faced at the end of 2024 before it conducted a somewhat disastrous restructuring/refinancing deal. Our latest work on asset coverage of liabilities did not provide comfort. AYR’s total liabilities to market cap implies a market belief that the company’s assets are only worth less than 60% of its liabilities. This week, Tilray announced that AYR’s interim CEO had joined the Tilray board. Does that signal an upcoming transaction? It seems hard to believe they could announce one piece of news if the other would be forthcoming. But a transaction doesn’t seem totally crazy to us.

- We now show both Vireo as it exists and Vireo Pf as the proposed transaction would make it. Note the eight-notch credit upgrade from the proposed transaction.

- Cannabis equity prices (as measured by the MSOS ETF) rose 8.87% for the week, bouncing off all-time lows.

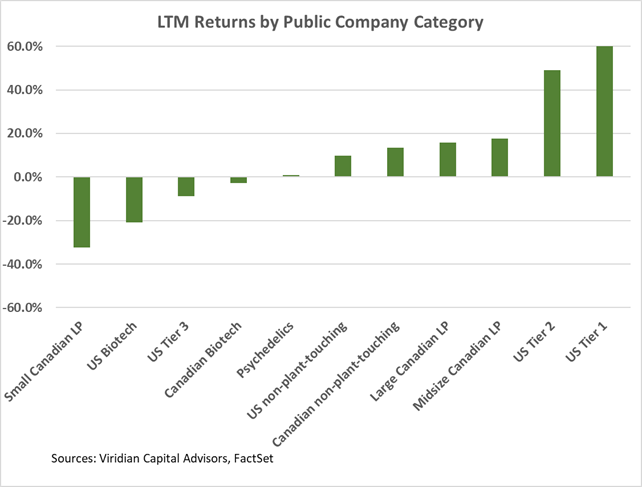

Trailing 52-Week Returns by Public Company Category:

-

- U.S. Tier 1s are now down nearly 50% over the LTM period versus a 15% loss on the tier 2s, consistent with a multi-year low in the valuation gap, our measure of large vs small company multiples.

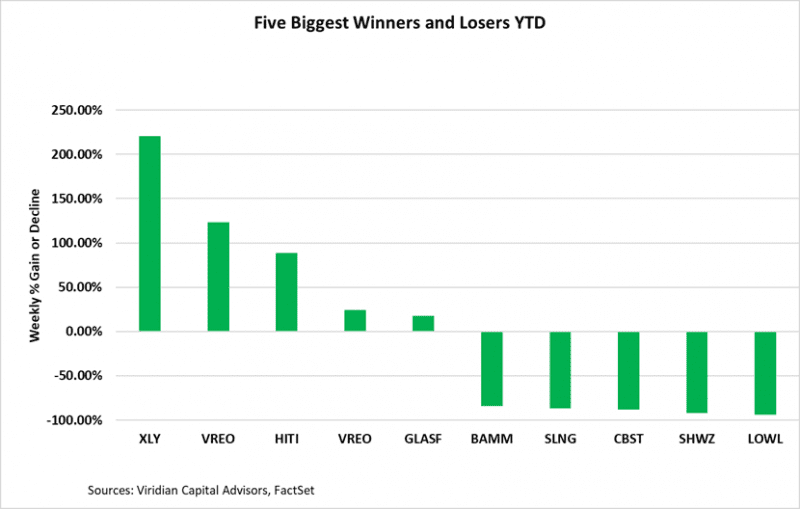

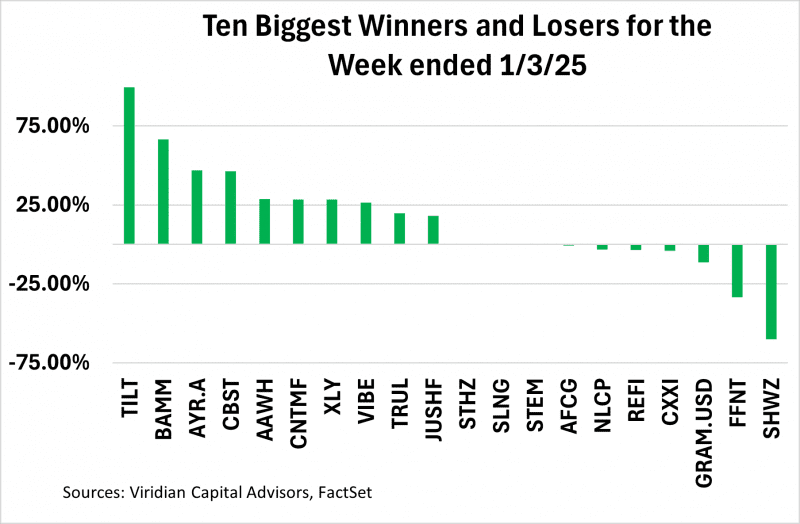

Best and Worst Performers for the week:

-

- Tilt (TILT: CSE) and Body and Mind (BAMM: CSE) were the best performers of the week after leading the losers list last week. Both equities appear to be out-of-the-money options based on our option theoretic market value of assets estimation methodology and are, therefore, primarily trading on volatility.

- Schwazze (SHWZ: CSE), another out-of-the-money option stock, was the biggest loser this week after being the second biggest gainer last week. It’s all about volatility trading.

- Gold Flora (GRAM: Cboe) was the biggest gainer, primarily based on the completion of a $2M debt raise, providing much-needed liquidity. The company places near the bottom of our credit list.