Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

- Best & Worst Perfromers

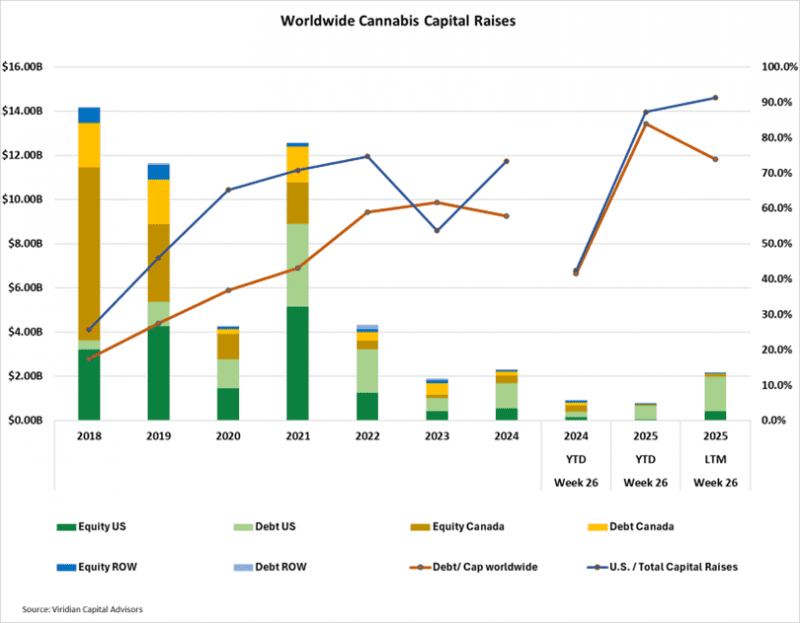

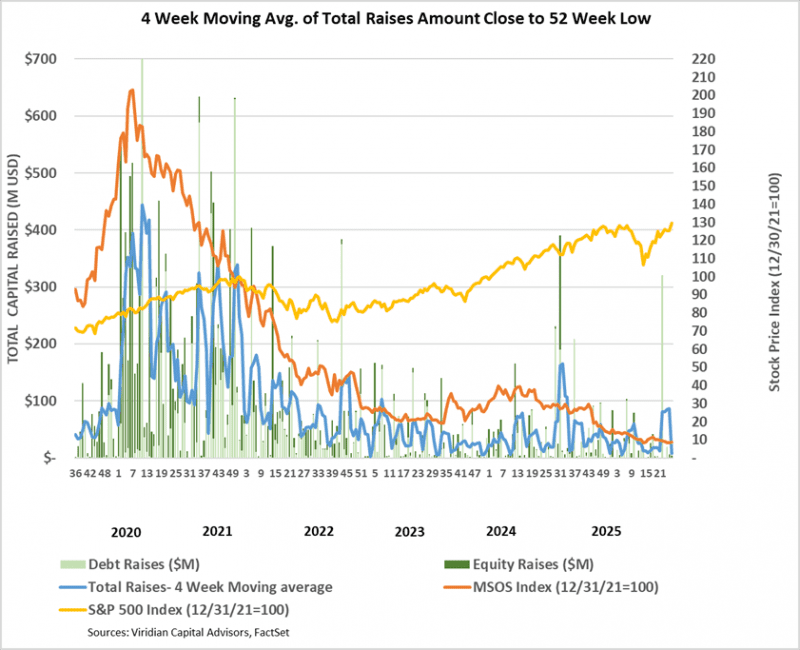

- YTD capital raises totaled $0.76B, down 16.1% from last year’s $0.91B. From an LTM view, capital raises totaled $2.17B, down 6.4% from the same period in 2024. Debt as a percentage of capital raised on a worldwide basis was 83.9%, compared to 41.6% last year. U.S. raises LTM accounted for 91.3% of total funds, up from 42.4% at the same point in 2024. Raises from outside of Canada and the U.S. represented 5.6% of the total funds raised, in line with the average of 5.33% in the six previous years.

- Public company raises accounted for 78.0% of total raises in the LTM period, the highest since 2021.

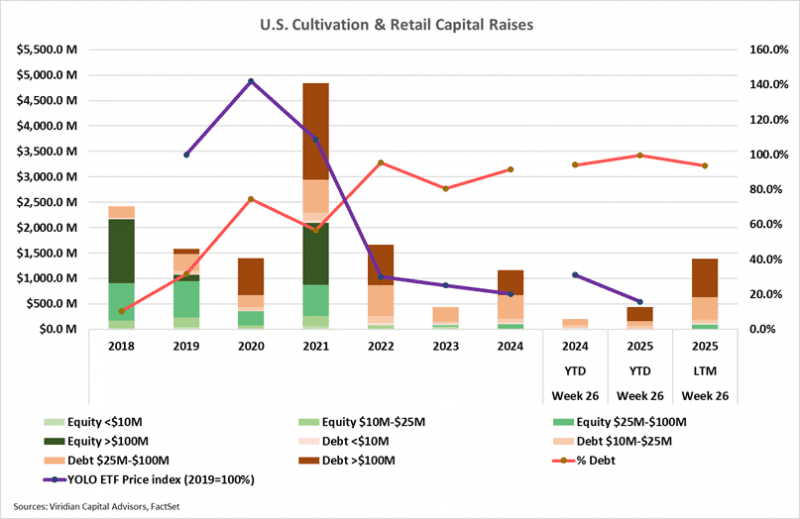

- YTD capital raises for the cultivation and retail sector total $436.69M, up 112.2% from last year’s $205.8M. For the LTM period, the capital raised in the cultivation and retail sector was $1,390.21M, 19.9% higher than in 2024, which in turn was up 167% from 2023.

- Debt accounts for 93.6% of the funds raised over the last 12 months (LTM). Large debt issues (>$100M) represented 54.4% of capital raised compared to zero in 2023.

- Cannabis equity prices (as measured by the MSOS ETF) were up 5.66% for the week.

VIRIDIAN INSIGHTS

- HEMP JUMPS THE GUN CELEBRATING ITS TEXAS “VICTORY”

- The Hemp industry was a bit too quick to celebrate the veto of Texas bill SB3, which would have banned all consumable hemp-derived THC products beginning September 1, 2025.

- We noted last week, though, that Abbott is no fan of Hemp, and his veto was narrowly based on:

- Legal Vulnerabilities: Abbott warned that SB3 would face constitutional challenges and that it could retroactively criminalize legal businesses violating state and federal protections

- Public Safety vs Enforcement: Abbott argued that because the bill would likely be delayed or weakened if it got tied up in court, it would leave harmful products unaddressed.

- Economic impact: Abbott undoubtedly heard from voters that the law, if enacted as proposed, would essentially eliminate over 50,000 jobs in businesses that generate over $4 billion annually.

- Abbott’s veto is not a business-as-usual move; he essentially wants to regulate hemp in ways similar to how other states regulate medical cannabis, with one twist: Abbott wants licensed retail operators to be overseen by the Texas Alcoholic Beverage Commission.

- We believe that the system Abbott foresees will drive significant amounts of the business underground into the illicit market. Hemp has become a massive market, driven by its wide distribution and low-cost products. Regulation, as envisioned, will substantially reduce both of those advantages.

- The veto is clearly better than the alternative of total elimination of the industry, but hemp advocates shouldn’t be cheering too loudly.

- More importantly, a far more threatening piece of legislation is working its way through the U.S. Congress.

- Hidden in the Agriculture-FDA appropriations bill are far more restrictive hemp provisions that would essentially eliminate the non-industrial hemp business on a nationwide basis.

- The bill redefines “hemp” as cannabis with a <= 0.3% total THC basis (including THCA)

- The bill also bars any consumable hemp product containing any “quantifiable” THC or similar cannabinoids, including both natural and synthetic forms.

- Industry leaders, including the U.S. Hemp Roundtable, believe the bill, as currently worded, would effectively ban all consumable hemp products, including CBD.

- The bill is still in the House, and if passed there, it would need to be considered in the Senate, followed by a conference committee that would reconcile the two bill versions.

- The bottom line is that there are a few times during the process where the current wording might get softened or removed. However, the threat of such a truly draconian bill taking effect on a national basis is daunting.

- IS RECEIVORSHIP THE INEVITABLE RESULT OF ONE TOO MANY “EXTEND, AMEND, AND PRETENDS?”

- On May 23, 2025, 4Front (FFNT: CSE)(FFTNF: OTCQB) announced that all of its U.S. subsidiaries filed for a voluntary receivership in aid of liquidation.

- Credit watchers attuned to our favorite early warning indicator, total liabilities to market capitalization, had ample warning: FFNT crossed our first warning line at 5x in July 2024, and by October, the company had surpassed our critical level of 10x.

- So, what does this mean for other beleaguered credits, namely AYR?

- We are convinced that a more global restructuring along the lines we outlined in our talk at MJUNPACKED could righten AYR’s ship. Our plan was based on converting approximately $120 million of the maturing 13s into equity, utilizing $30 million derived from asset sales (including the Virginia license), and extending the remainder. Our pro forma showed a company with approximately 2.4 times Debt/EBITDA, a sustainable load even in an ongoing 280E environment. Of course, obtaining agreements between diverse groups of lenders and equity holders is never easy, resulting in two main alternatives: the ever-popular “kick the can down the road” maneuver or receivership. Are lenders finally at a point where they want to try a third strategy? Or is liquidation through receivership the new normal?

- WILL TRUMP HAVE THE FORESIGHT TO STEAL THE CANNABIS ISSUE?

- We never felt that a pronouncement of support from Joe Biden would be enough, and we were proven right. However, we believe that if Trump publicly reaffirmed his campaign pledges regarding rescheduling and SAFER, both would happen.

- So, what will it take to get his attention and get Cannabis to the top of his list of priorities?

- First off, Cannabis is the ultimate in States’ rights issues. The very existence of the industry owes to the willingness of the states to thumb their nose at the federal government. Trump is no anarchist in that regard, but he is still a big supporter of states ‘ rights

- Next, cannabis reforms can add billions to the economy by fostering job growth, increasing tax revenues, and reducing significant expenses in police, courts, and jails, among others. This goes along well with his pro-business and cost-cutting leanings.

- Promoting Cannabis is consistent with his tough stand on opioids, fentanyl, and drug gangs. Some states, like Utah, have explicitly stated that they believe their medical cannabis program can be the off-ramp for opioid abuse. Trump is skilled enough to make the point that being hard on hard drugs and pro-cannabis are consistent positions.

- Cannabis is an immensely popular issue favored by a strong majority of voters. With midterms coming up fast, Cannabis is an issue that Trump can steal from the Democrats and use to solidify his base.

- All of this and NOTHING from the White House? Has the world really become so ridiculous that it all rides on an appeal from Mike Tyson?

- ADMITTEDLY, OUR ARGUMENT BELOW DOES NOT SEEM TO HAVE AGED WELL WITH THE OUTPOURING OF ANTI-HEMP LEGISLATION ON THE STATE LEVEL AND NOW ANTI-HEMP BILLS IN THE U.S. HOUSE. STILL WE STICK BY WHAT WE SAID…

- It’s easy to see the impetus for moving into Hemp since the Hemp space has what the THC space desperately needs: Growth. It’s not exactly a closely held secret that hemp intoxicants, along with illicit THC vendors, have hit the THC industry right where it hurts. After all, what is the most significant incentive for an investor to consider crossing the gap and investing in a federally illegal substance? Growth right? Lately, however, growth has not been abundantly evidenced. Analysts are actually projecting a nearly 4% y/o/y decline in 2025 revenues and an 8% decline in EBITDA for the top 12 MSOs.

- Why is Hemp growing, and THC isn’t? In a nutshell, price and convenience. The Hemp intoxicant space, along with the illicit THC space, both drive home one point: there is a significant portion of the market that doesn’t care about seed-to-sale tracking and a COA on every bottle. They will gladly trade that for the ability to purchase at their gas station or, better yet, online through the mail, especially if it costs less. The THC market wants people to fear untested and untracked hemp products, but perhaps THC is overtested and over-tracked in ways that don’t add much value to the product.

- We think most of the tier-one MSOs who have not yet embraced Hemp THC beverages will eventually enter the sector. But what is keeping the MSOs from creeping farther across the line and beginning to sell THCA flower or other intoxicating hemp-based products? We see three reasons: reputational risk, political risk, and economic risk.

- On the reputational side, we see general agreement around the idea that hemp THC beverages are “OK.” And a short step away are hemp THC gummies. But smokable hemp intoxicants are still controversial, and top MSOs seem unwilling to offend any of their constituencies, especially investors, by jumping across the line quite yet. But that’s an economic calculus, not one driven by any deeply held principle. In fact, the whole idea that hemp THC beverages are OK, but THCA flower and other smokable hemp intoxicants aren’t, strikes us as less than intellectually honest. After all, it is the same molecule.

- On the political side, cannabis operators correctly believe that if they jump fully into the hemp intoxicant business, without even the fig leaf of only doing drinks, it will be virtually impossible to continue pushing for the elimination of these products. And make no mistake, MSOs in limited license states are still hoping they can stuff the genie back into the bottle! As time drags on with no new Farm Bill in sight and statewide legislation proving difficult, if not unworkable, we expect to see defections.

- On the economic side, perhaps licensed cannabis operators fear that such operations will cannibalize their licensed, tested, and over-costed THC operations. We are currently in Key West, where there is a chain of shops called Green Place. Blazoned in bold lettering across the entrance is a sign proclaiming, “No medical card required,” which is also a code for “tourists are welcome.” In the store, we found an assortment of flower, vapes, and prerolls that we were hard-pressed to identify as anything other than Weed, but under the guise of the farm bill, this was all Hemp. We do not doubt that this idea will spread further in the months to come.

- The production cost, tax, regulatory, and distribution advantages of Hemp make it a classic case of disruption that is difficult, if not impossible, to stop. The only real question is, will hemp become just another thriving part of the illicit market?

- GAUGING THE RISK OF THE 2026 DEBT MATURITY BUBBLE

- Much has been made of the upcoming wave of cannabis debt maturities in 2026. The sheer size is undoubtedly intimidating. The companies pictured on the graph below collectively have approximately $2.6 billion of debt maturing in 2026. (IAnthus maturities are actually in 6/27, but close enough!). Putting that figure into perspective, $2.6B is greater than the total capital raised for the cultivation & retail sector for any year since 2018, except for 2021.

- Viridian is generally more constructive about the issue than most other industry observers. We observe that in the high-yield bond market, it is virtually never the case that debt is paid off in cash. It is generally refinanced, OR the company is forced to restructure. Obviously, given the lack of prepackaged bankruptcy (or any bankruptcy, for that matter), restructuring is rightfully a prospect to be feared in the Cannabis Industry.

- So, how do we gauge the risk of something going wrong in 2026? Refinancing risk is a peculiar mixture of market psychology and financial realities.

- Successful completion of the Cannabist plan discussed above should have a positive impact on the market psychology regarding the other troublesome maturities. However, that effect has been clouded by overall market turmoil. And lest we seem Pollyannaish, we do recognize that several companies are looking increasingly troublesome. The graph below shows three relevant data points:

- The green bars show the 6/27/25 market-implied asset coverage of total liabilities. We arrive at this by viewing the equity as a call option on the asset value of the firm, with a strike price equal to its liabilities, and assuming maturities of 2026, as well as volatility of 40% and a risk-free rate of 4.25%. This provides us with all the elements of the Black-Scholes option pricing formula except for the current asset value. By iterating on the solution of the BS model, we can find the market’s assumption for asset value. The importance of this data point should be obvious. For companies with less than 1x asset coverage of liabilities, debt providers are effectively making an equity bet. They do not have adequate asset value coverage to fall back upon.

- The red line represents the Viridian Capital credit ranking, which considers four key credit factors: Liquidity, Leverage, Profitability, and Size. Refinancing will be more difficult for weaker credits (higher numbers). Companies with ranks of under 16 are in the top half of the Viridian-ranked universe of credits.

- The black dots represent the multiple of market cap that the 2026 debt maturities represent. Clearly, the larger the debt maturities relative to the market cap, the more difficult we would expect refinancing to be. The seven companies from ITHUF to the right side of this graph (except Cannabist) represent high risk. They have less than 1x asset value coverage, poor Viridian Credit Ranks, and maturing debt that is a multiple of market cap. Companies in this position represent approximately $867M of the maturing debt. Conversely, the five companies on the left-hand side of the graph represent low refinancing risk. They have solid asset coverage, strong Viridian Credit Ranks, and maturing debt that is less than one times their market capitalization. These companies represent $1.6 billion of the $2.6 billion total (62%), and we believe they should all be able to refinance their maturities without undue hardship.

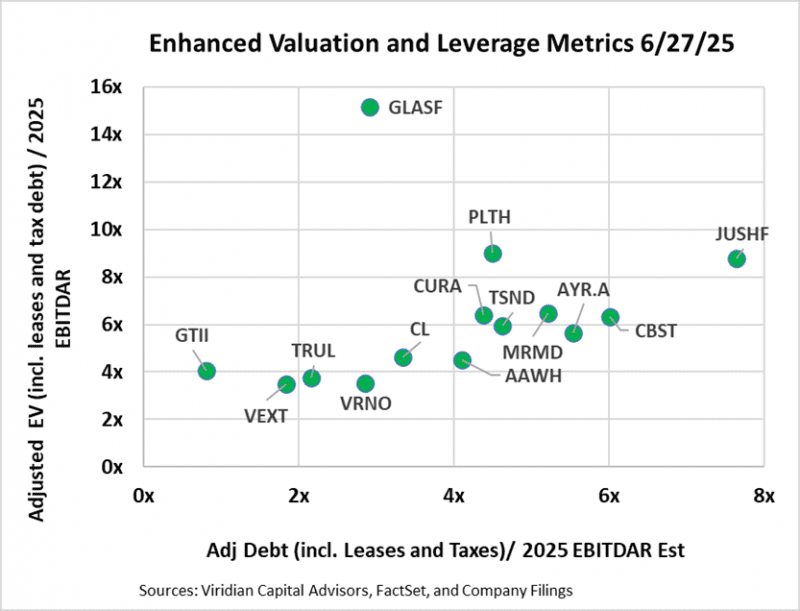

- FOUR KEY GRAPHS THAT SEEK TO MAP THE OPTIONS AVAILABLE TO THE MSOs BASED ON THEIR VALUATION, LEVERAGE, AND LIQUIDITY

- The first two graphs present different versions of EV/EBITDA on the vertical axis and Debt/EBITDA on the horizontal axis.

- The first graph presents our latest view of the most appropriate valuation and financial statement-based leverage metrics: Adjusted Enterprise Value (EV) / 2025 EBITDAR and Adjusted Net Debt / 2025 EBITDAR. In calculating Adjusted Net Debt, we make several key assumptions: 1) Leases that are included on the balance sheet are considered debt. We view most leases in the cannabis space as equivalents to equipment loans or mortgage loans. While it is true that a lease default does not necessarily trigger a cascade of events leading to bankruptcy, the distinction is often meaningless in the Cannabis Industry due to the mission-critical nature of many long-term leases and the absence of bankruptcy protection in This Sector. 2) We consider any accrued taxes (including uncertain tax liability accounts listed as long-term liabilities) in excess of the most recent quarterly tax expense to be debt. Our calculation of enterprise value is now market cap plus debt plus leases plus tax debt minus cash. We now use EBITDAR rather than EBITDA, as lease expense is deducted prior to calculating EBITDA.

- The second graph utilizes EBITDA and employs traditional calculations for both debt and enterprise values, excluding leases and taxes.

- Our adoption of new metrics tends to make the companies look less cheap and more leveraged.

- Surprisingly, nine of the companies on the enhanced metric chart are still above 3x leverage, which we have identified as the boundary of sustainability in a 280e environment. Four companies now exceed 4x leverage, which we believe will be close to the maximum sustainable post-280E.

- Jushi appears as a leverage outlier using the new metrics relative to AYR, which seemed more leveraged using standard measures.

- Glass House is a valuation outlier. We have been positive on Glass House for quite a while, but the multiple spread to the nearest competitor is straining our resolve. We note GLASF’s $25M at the market equity issuance facility as another factor likely to restrain price appreciation.

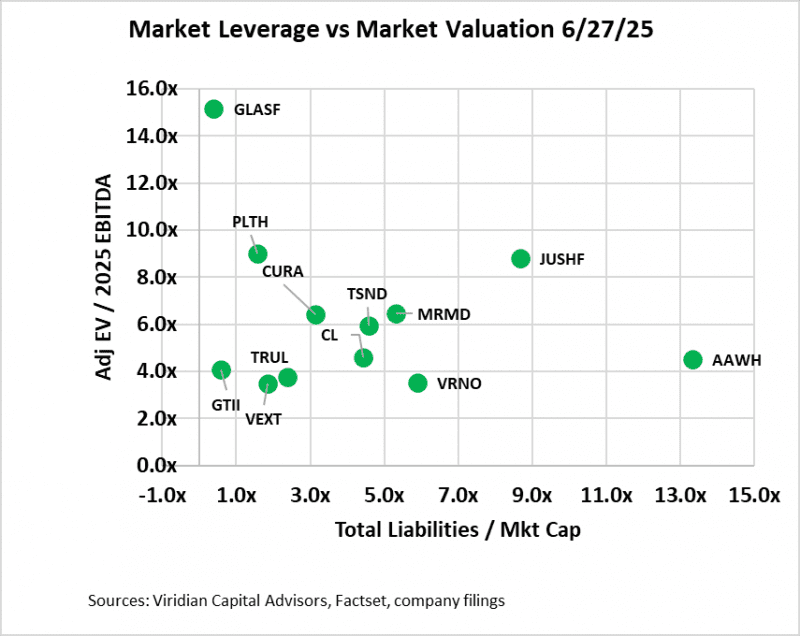

- The third graph examines leverage through the lens of total liabilities to market capitalization. We believe this is the single best measure of leverage because it is a direct reflection of the market’s assessment of a company’s assets in excess of its liabilities, and it is sensitive to changes in the market’s perception of a company’s future prospects.

- On the bottom left are companies with an Adj. EV/2025 EBITDAR ratio of under 6x and total liabilities to market cap of under 2x. The group includes GTI and Trulieve. Companies in this quadrant are right to consider stock repurchases or using cash in acquisitions. They can afford some additional debt and can take advantage of the ongoing dislocation in equity prices.

- Between 2x and 5x total liabilities to market cap, we find Verano, Curaleaf, Cresco, and MariMed. Verano, Curaleaf, and Cresco all have significant 2026 maturities; however, we do not believe they are likely to face difficulties refinancing their debt.

- On the right lies Jushi and Ascend, both between 6x and 12x, a range that signals stress if not distress.

- AYR, 4Front, Cannabist, and Schwazze are now off the chart to the right, signaling profound credit risk. Our recent work, which utilized option modeling of equity prices, showed that the market believes each of these companies has significantly less asset value than its liabilities.

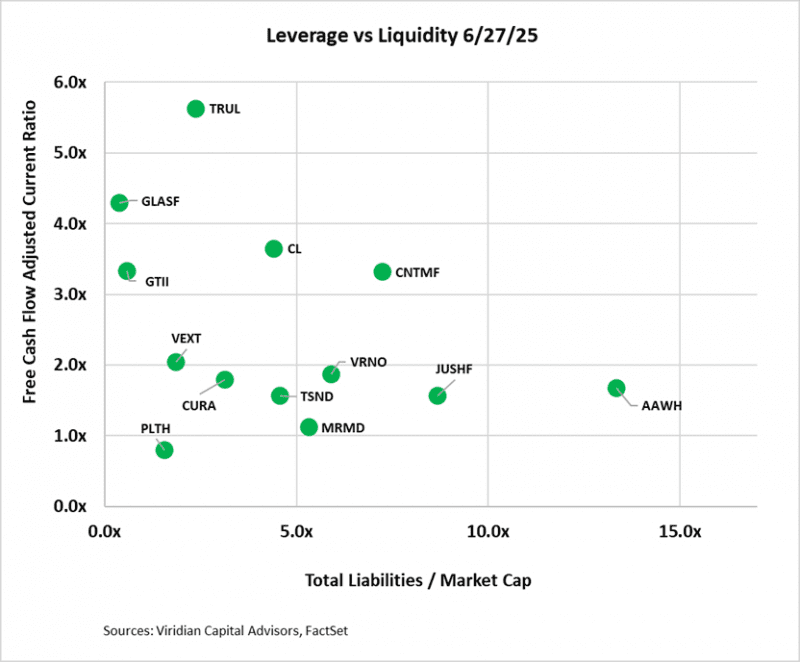

- The fourth graph introduces the free cash flow adjusted current ratio liquidity measure into the mix. Note that we have recently modified our treatment of this ratio by removing uncertain tax liabilities from current liabilities, where they were previously placed. The result is that no company is currently significantly below 1x free cash flow adjusted current ratio.

- On the top left, we find companies with adequate Liquidity and low market leverage, including both GTI and Planet 13.

- Companies in the lower middle-to-right generally have constrained Liquidity and high leverage, a potentially dangerous combination in a capital-constrained environment. Five, including Schwazze, Cannabist, Ascend, MariMed, and 4Front. These companies are characterized by high market leverage and low Liquidity, making them high-risk. Note: SHWZ, CBST, AYR, and 4Front are now off the chart to the right, with extreme market leverage indicating significant distress.

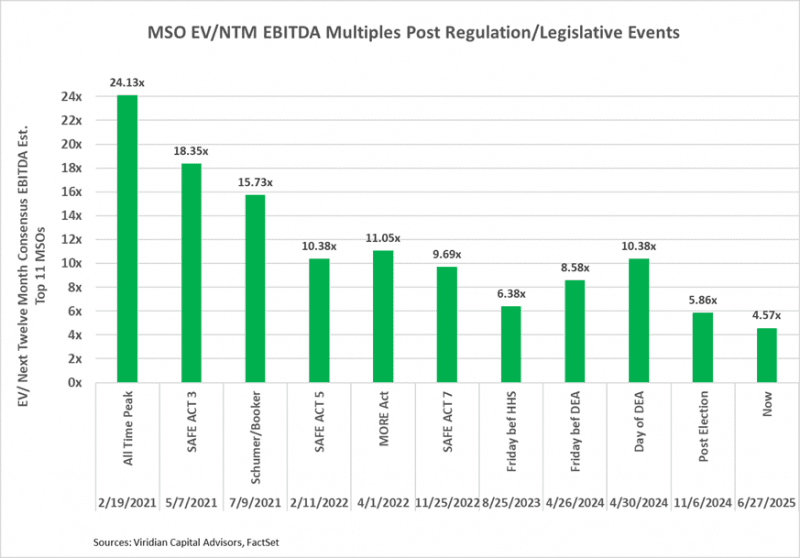

- VALUATION METRICS SUGGEST STRONG UPSIDE POTENTIAL FROM ANY REGULATORY REFORM, BUT EQUALLY POWERFUL MARKET SKEPTICISM

- The chart below shows that cannabis companies are trading at historically low valuation metrics, significantly lower than before S3 was a gleam in HHS’s eyes. Granted, there are a host of industry-specific problems that extend beyond regulatory reform, including slowing growth, wholesale pricing pressure, and a weary consumer.

- We continue to believe that at current levels, U.S. MSOs have enormous upside potential. We are not Pollyannish about the issues and recognize that the industry faces several deep-seated problems, including competition with Hemp, wholesale price compression, and a reliance on new markets for growth. Moreover, it likely requires some political catalysts to achieve significant gains, and the market is beyond worrying about timing and is concerned that these reforms may never transpire. The graph below illustrates the multiples achieved following various past legislative and regulatory events. It makes clear that a doubling of prices is a reasonable possibility.

- However, it’s increasingly important to focus on building a diversified portfolio of companies that can operate independently of Washington, as it’s anyone’s guess when that will arrive. Focus on the top 10 companies in our credit rankings. There ARE investable companies besides GTI. Add them to your portfolio and track the total liabilities to market cap indicator, as well as the credit tracker rankings.

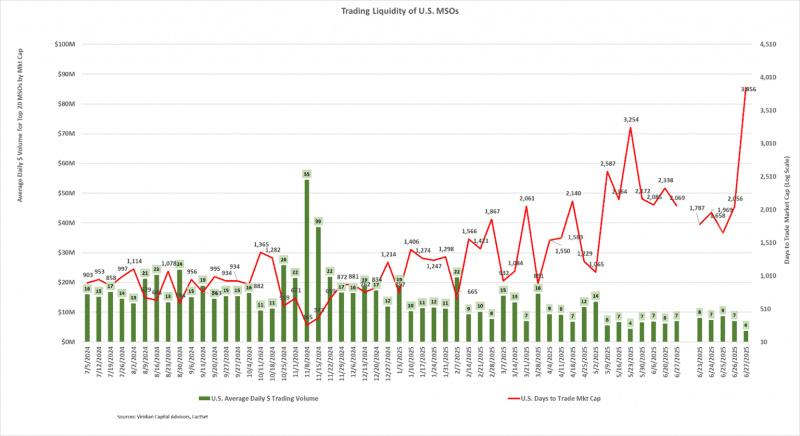

- CANNABIS STOCK VOLUME AND LIQUIDITY STILL NEAR 52-WEEK LOWS

- The average daily dollar volume of $ million for the week ending June 27, 2025, tied for the lowest volume for the last twelve months. The current DTTMC of 2,069 represents the third-lowest Liquidity we have measured. A DTTMC of 2,039 implies that an investor who acquired a 5% position in the stock, assuming they wanted to be less than 25% of the average daily dollar volume, would require 414 days to trade out of their position. A market with this lack of Liquidity is virtually uninvestable by institutional capital. Liquidity has been trending downward since the election in response to stalled cannabis reform and general economic uncertainty.

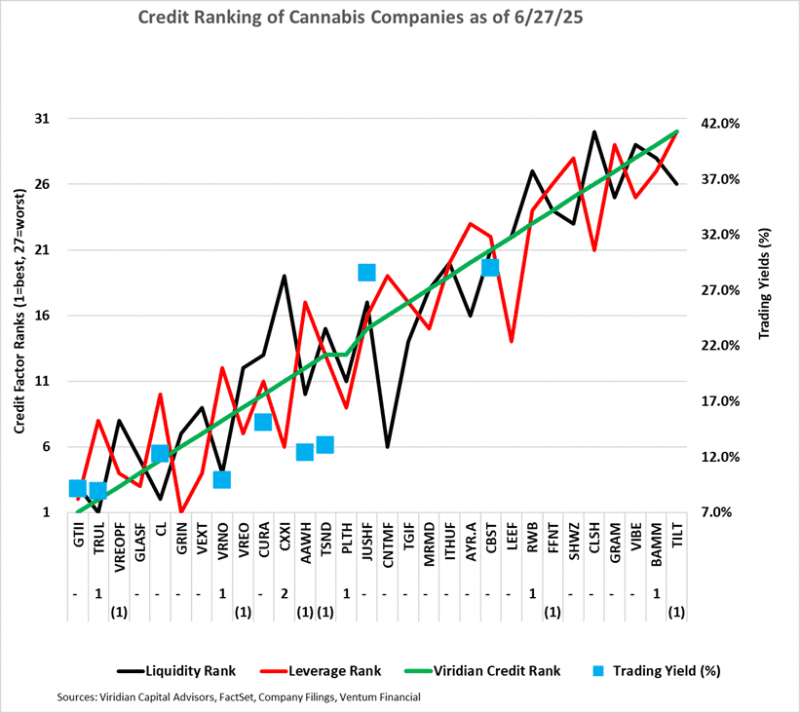

- GIVING CREDIT WHERE CREDIT IS DUE

- The chart below displays our updated credit rankings for 31 U.S. cannabis companies as of June 27, 2025. The number below the ticker symbol indicates the change in credit ranking since last week. A negative number suggests credit deterioration, while a positive number indicates improvement.

- The blue squares show the offered-side trading yields for each Company. Cresco and Curaleaf are both trading at higher yields than their credit quality warrants. This suggests several possible trades: sell Ascend and TerrAscend and buy Curaleaf. Sell Verano and buy Cresco.

- For investors with a significantly higher risk tolerance, we note that AYR 13s of 2026 are now trading flat and are offered at 55. While this aligns directly with our option-based asset value coverage metric, we believe that a restructuring has the potential to produce a significantly higher value for the senior secured debt.

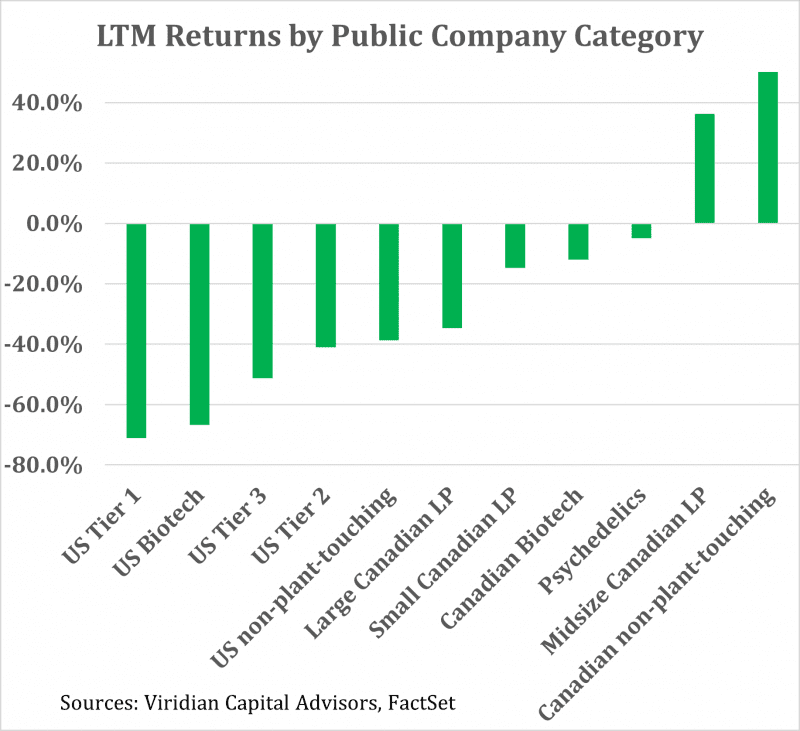

Trailing 52-Week Returns by Public Company Category:

-

- Plant-touching categories continue to trade at significant LTM losses.

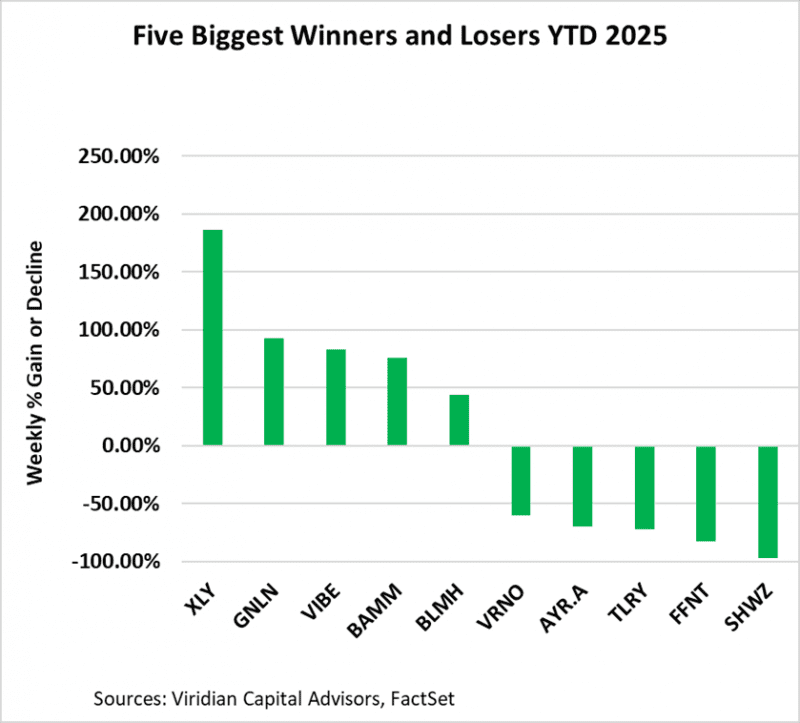

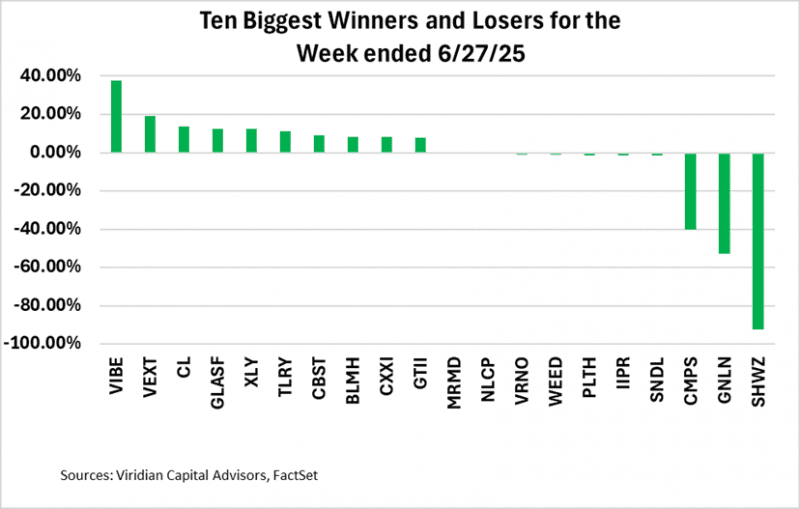

Best and Worst Performers for the week:

- AYR, 4Front, and Schwazze, three companies with significant solvency concerns, continue to exhibit substantial losses in their last 12-month (LTM) stock prices.