Each week, Viridian publishes insights and analysis on completed M&A transactions in the prior week. Our analysis includes:

-

- M&A Market Commentary

- Public and Private Companies

- Buyers & Sellers

- YTD M&A Analysis

- M&A by Industry Sector

- Deal Structure and Valuation Analysis

- Pending Deal Risk Arb Analysis

- Valuation Gap Analysis

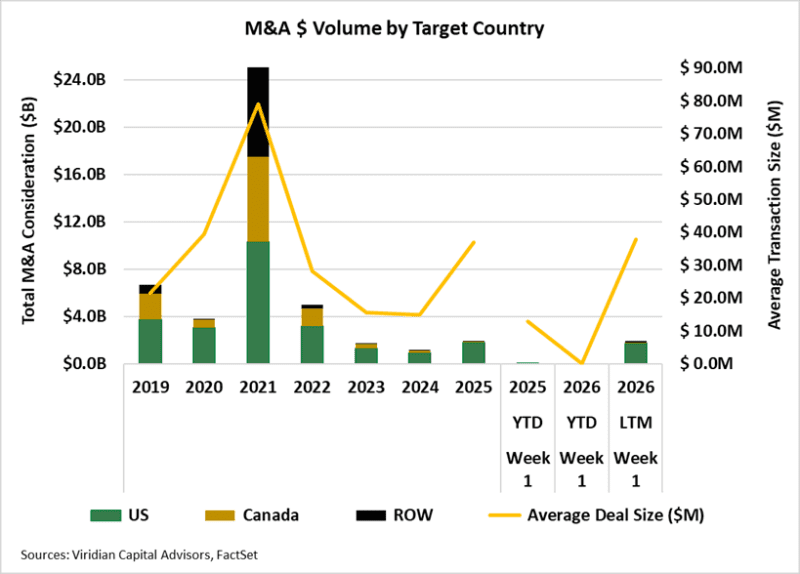

- For the LTM period, total M&A consideration is down 1.3% from the same period in 2025, while the deal count is down approximately 3.8%. Transactions targeting the U.S. are down 1.4% from roughly $1.78 billion to $1.75 billion. LTM, 50 M&A transactions have closed, totaling $1.9B in disclosed value.

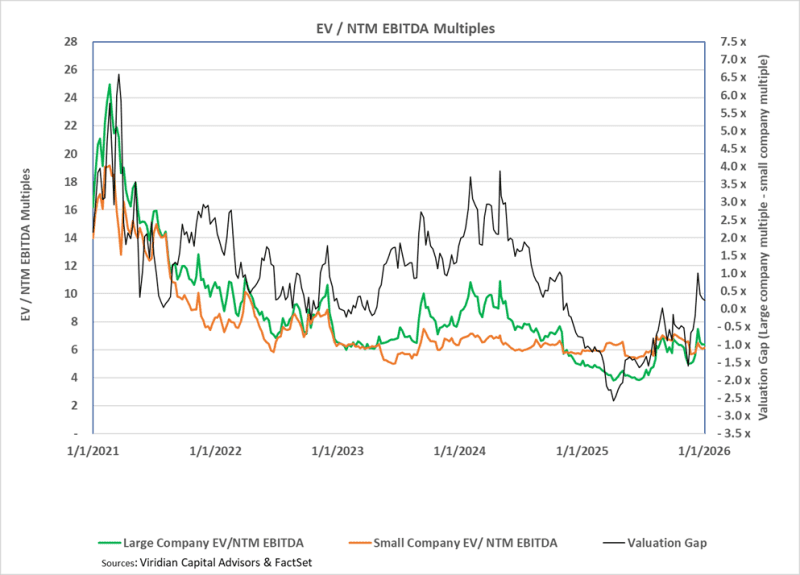

- The Valuation Gap

-

- The Valuation Gap measures the difference between the EV/NTM EBITDA multiple for the largest MSOs and that for the next-smallest group of MSOs. This measure has been a significant driver of M&A activity, as a larger gap creates opportunities for more accretive transactions.

- The companies included in the large-cap index are Cresco (CL: CSE), Curaleaf (CURA: CSE), Green Thumb (GTII: CSE), TerrAscend (TSND: TSX), Trulieve (TRUL: CSE), and Verano (VRNO: CSE). The small company index now includes Ascend (AAWH: OTCQX), Cannabist (CBST: CBOE), and Jushi (JUSHF: OTCQX). The gap declined from .301 to .289 on January 2, 2026. At 0.289, the gap suggests that, in aggregate, the climate is not yet hospitable for Tier one companies acquiring Tier two This may not be the case for individual combinations, however, as there are wide valuation-metric spreads between companies in each tier. For example, TerrAscend, GTI, and Curaleaf all trade well above the Tier 1 average, while Ascend trades well below the Tier 2 average. The overlap of licenses has been a major restraining factor inhibiting public/public acquisitions. The difficulty of selling duplicated operations in a capital-tight environment is a key reason. Eventually, however, we believe the industry will consolidate. To achieve this, MSOs may need to accept that valuation multiples will not return to 2021 levels, even if S3 is enacted. The upside catalysts of S3 and SAFER are currently stalling any movement in that direction, much like they are locking up the equity market.

- Historically, the vast majority of M&A transactions in the Cannabis Industry have involved public companies acquiring private companies, and the recent Vireo transactions continue this trend.