Viridian publishes weekly data and analysis on debt capital raises in the Cannabis/CBD/Psychedelic industries. This data includes information about the company issuing debt (public/private, state/country location), deal size, deal structure, pricing, warrants, and credit data.

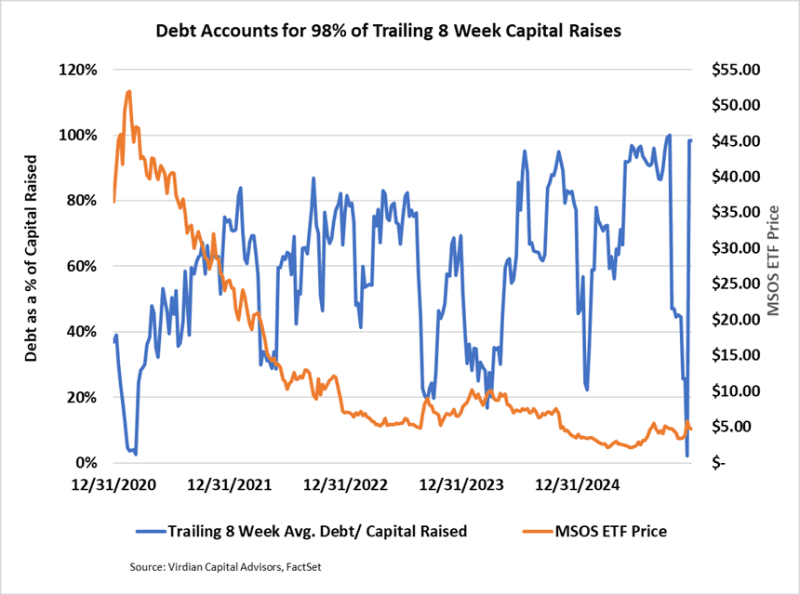

- Debt accounted for 98% of trailing 8-week capital raises.

- We believe that a successful move to S3 will increase the likelihood of other near-term regulatory moves, such as the SAFER or STATES. The real question is what kind of price increase it will take before cannabis companies are willing to issue equity. Will the change to S3 result in a lasting price pop that could lead to re-equitization?

Viridian publishes weekly insights on debt capital raises in the Cannabis/CBD/Psychedelic industries. These insights typically highlight the most interesting/meaningful debt transactions of that week, and commentary on market conditions, debt deal structures, and lenders.