Each week, Viridian publishes insights and analysis on completed capital raise transactions in the prior week, focusing on all equity and debt deals. Our analysis includes:

- Summary

- Outlook

- Best & Worst Perfromers

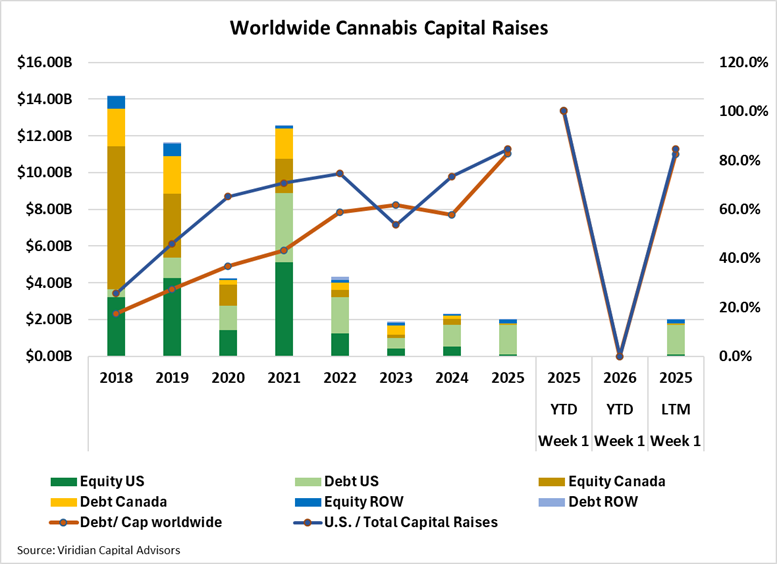

- From an LTM view, capital raises totaled $2.0B, down 13.4% from the same period in 2025. Debt as a percentage of capital raised worldwide is 82.6%, compared to 57.8% in the previous year. U.S. raises LTM accounted for 84.6% of total funds, up from 73.4% at the same point in 2025. Raises from outside Canada and the U.S. accounted for 11.2% of total funds raised, more than double the average of 5.3% over the six previous years.

- Public company raises accounted for 93.1% of total raises in the LTM period, the highest in at least the last 7 years.

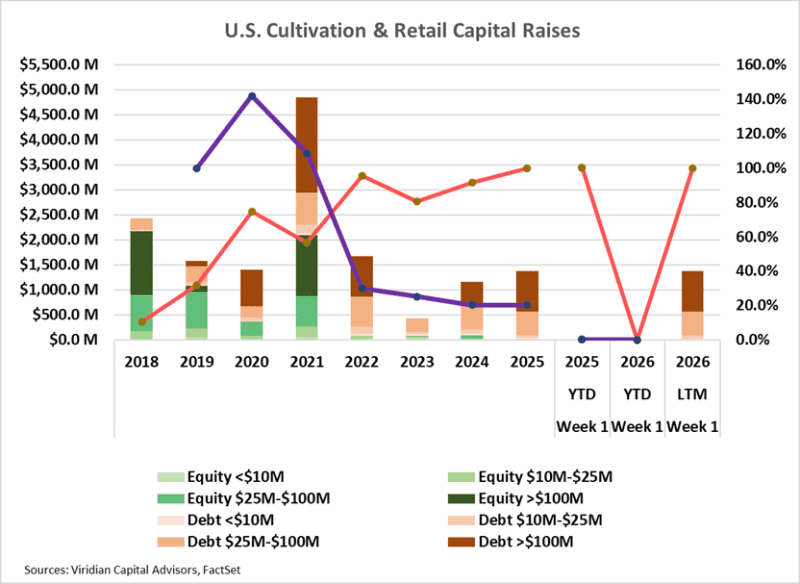

- For the LTM period, the capital raised in the cultivation and retail sector was $1.37B, 18.5% higher than in 2024, which in turn was 160% higher than in 2023.

- Debt accounts for a whopping 99.7% of the funds raised over the last 12 months (LTM). Large debt issues (over $100M) accounted for 59.3% of capital raised, up from 0% in 2023.

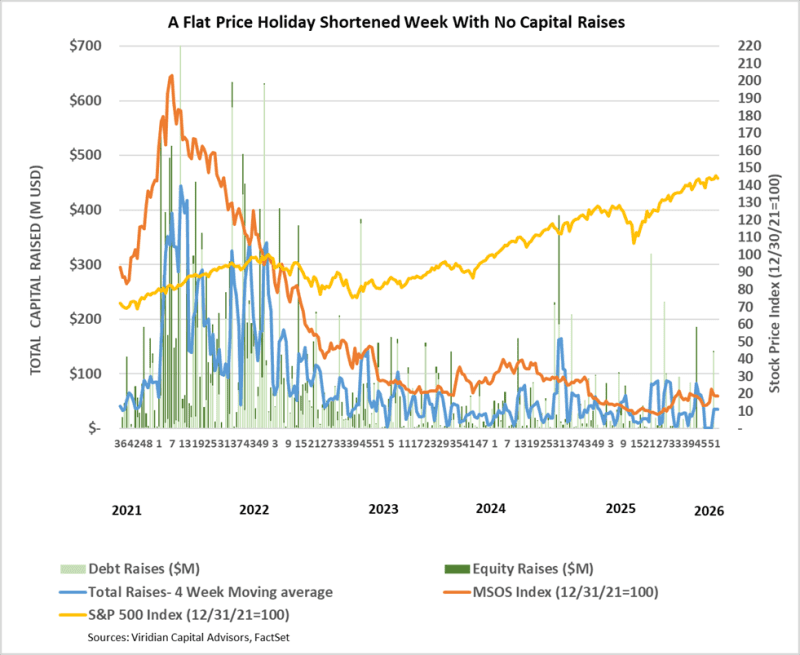

- Cannabis equity prices (as measured by the MSOS ETF) fell by 0.4% for the week.

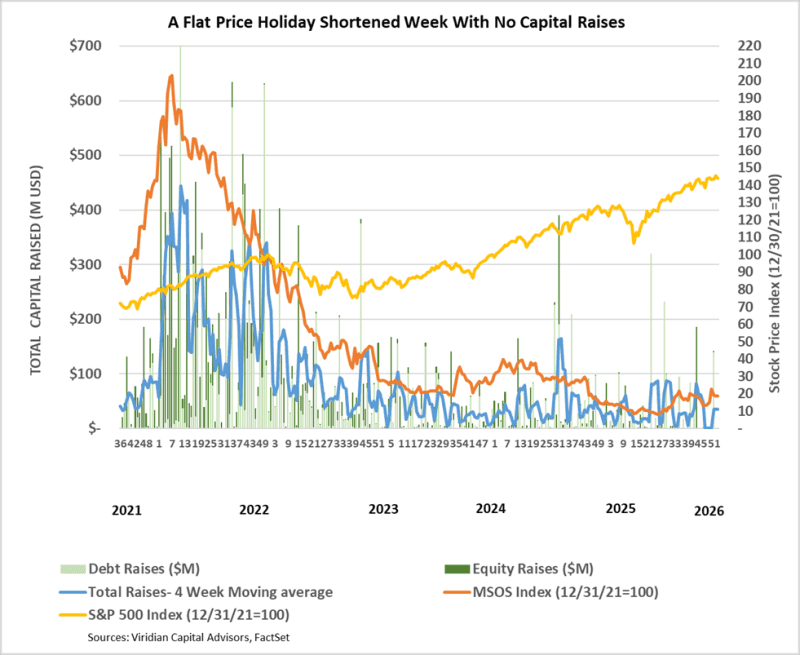

- Cannabis equity prices (as measured by the MSOS ETF) fell by 0.4% for the week.