OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Viridian publishes weekly data on M&A transactions in the Cannabis/CBD/Psychedelic industries. This data includes information about the buyer and seller (public/private, state/country location), deal size, deal structure (cash, stock, earn-out), pricing, share information, and deal implied valuation.

The Largest Closed and Disclosed M&A Deal of the Week:

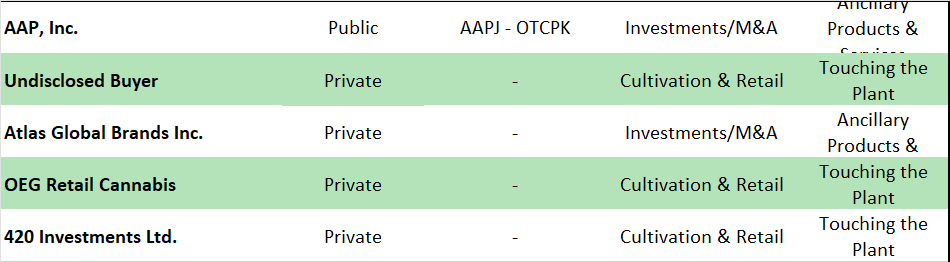

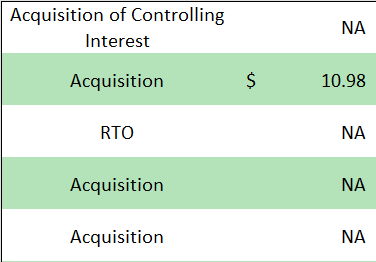

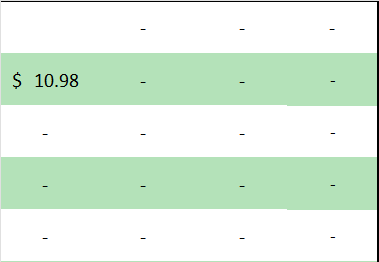

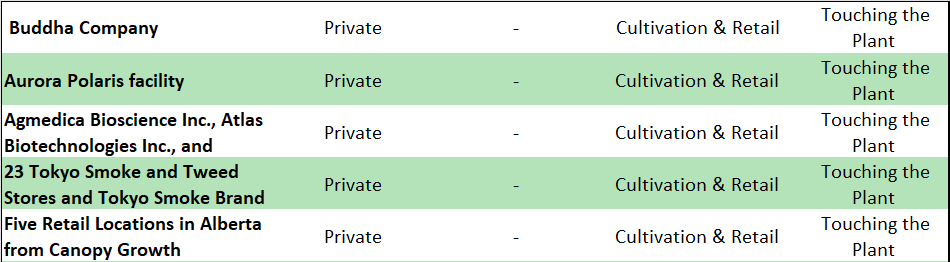

- On January 4, 2023, Aurora Cannabis (ACB: Nasdaq)(ACB: TSX), the sixth largest Canadian LP by market cap, announced the closing of the sale of its Aurora Polaris facility for approximately US$11.0M.

- Aurora recently repurchased $76M of its senior convertible notes for approximately $74M in a transaction we criticized because we believed it represented an inadequate discount to reflect the company’s credit risk. The company now has proforma cash of approximately $320M and roughly $114M of debt.

- Aurora has maintained that it will achieve a positive EBITDA run rate by December 31, 2022. We are a bit skeptical, having heard this from Aurora before. Still, a breakeven EBITDA would leave the company with an estimated negative $10-15M free cash flow per quarter, giving them less than a year of a cushion given their net cash position. The risk in this scenario is that the aggressive cost-cutting program may accelerate the continued erosion of the company’s sales. It isn’t easy to project a path to significant profitability. The best hope for ACB is it can capitalize on growing medical markets in Europe. However, competition from other Canadian producers and new competition from South America makes this far from a sure bet.

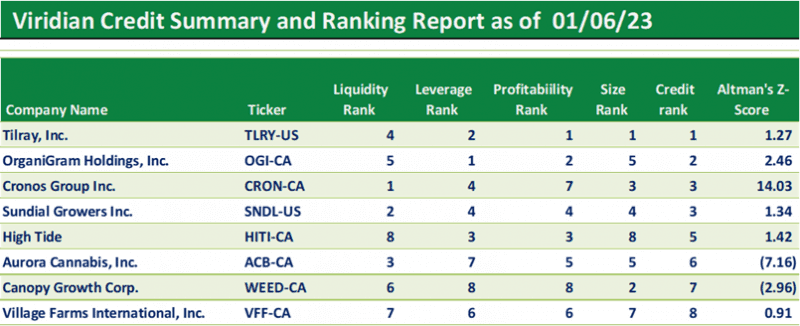

- The Viridian Capital Credit model ranks Aurora # 6 out of the 8 Canadian LPs with market caps over $100M. The company has relatively strong liquidity but high market value leverage and poor profitability.

Viridian publishes weekly insights on the M&A landscape in the Cannabis/CBD/Psychedelic industries. These insights typically highlight the most interesting/meaningful M&A transactions for that week, and commentary on market conditions, M&A deal structures, target regions for acquirers, and industry sectors ripe for consolidation.