OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Viridian publishes weekly data and analysis on debt capital raises in the Cannabis/CBD/Psychedelic industries. This data includes information about the company issuing debt (public/private, state/country location), deal size, deal structure, pricing, warrants, and credit data.

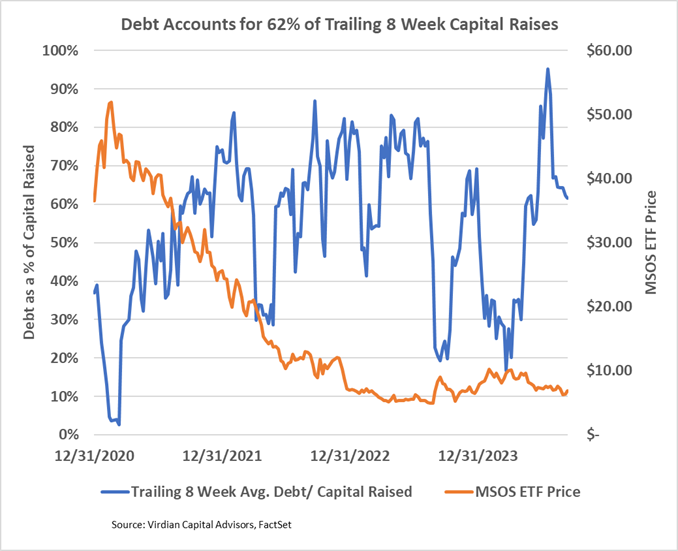

- Debt accounted for 62% of trailing 8-week capital raises. The ratio may go down if companies are able to utilize favorable regulatory-induced stock price increases to complete equity issues. However, equity pricing has remained stubbornly low while the cannabis debt capital markets have reopened dramatically.

- The Week’s Debt Transactions

- On 9/12/24, Green Thumb (GTII: CSE)(GTBIF: OTCQX), consistently ranked as the strongest credit in the cannabis universe by the Viridian Capital Credit Tracker model, closed a $150M term loan with a bank syndicate led by Valley Bank.

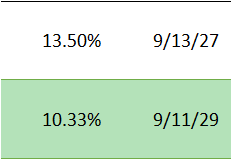

- The loan has a five-year term and is priced at SOFR plus 500bps for an initial rate of 10.33%. Based on the five-year SOFR to fixed swap curve, we estimate that this equates to a fixed rate of around 9.06%. Although this is an eye-popping great cannabis debt rate, it still represents a spread of 560 bps over the five-year Treasury, a spread considerably in excess of what we see appropriate for what we view to be a solid B.B. credit. As a reference point, the BofA B.B. yield index is now approximately 186 bps over the curve. This gap is a good indication of the amount of credit spread improvement that the top-ranked cannabis credits can expect as cannabis becomes normalized.

- The loan includes quarterly amortization payments and standard maintenance covenants, including a minimum debt service coverage ratio, a maximum debt to EBITDA ratio, and a minimum liquidity ratio. The levels of these covenants were redacted from the filing, so it is impossible to know how tight the covenants are.

- The bank group is obviously pretty comfortable with GTI, though, as it allows the company’s announced $50M share repurchase program, which admittedly is relatively small given the company’s market cap.

-

- On 9/13/24, Acreage Holdings (ACRG.A: CSE)(ACRHHF: OTCQX), ranked 28/31 in credit quality on the Viridian Capital Credit Tracker model, closed an amended and restated three-year credit facility for a face amount of $65M.

- The debt was issued with a 10-point OID for net proceeds of $58.5M. The 13.5% coupon and the OID produce a yield of 17.88%

- This seems like an excellent deal for Acreage, especially given that no equity kickers were involved. This transaction, along with the recent Jushi deal, is a clear sign that the cannabis debt capital markets have come a long way and are willing to dip down into relatively risky credits.

- Of course, it is not fair to evaluate Acreage without reference to the implied support of Canopy. Acreage is pretty central to Canopy U.S., and we think Canopy would go to considerable lengths to provide support if required. Of course, Canopy itself is a bit of a melting ice cube of credit, so different observers can reasonably weigh the value of this support differently.

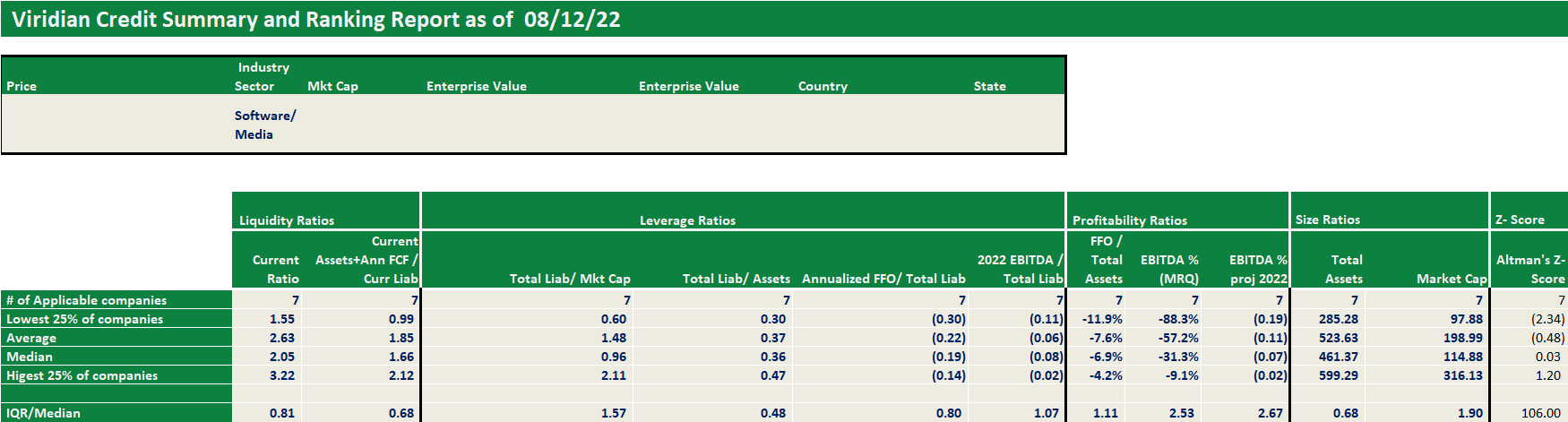

Each week, Viridian highlights a specific industry sector and provides a deep dive into credit metrics and comparable company credit rankings for public companies operating in that sector. Credit ratings are not currently available for public cannabis companies leaving companies, lenders, and investors with a gap of information. The Viridian Cannabis Credit Tracker fills this gap. The model uses 11 market and financial statement variables to discern 4 key credit factors: Liquidity, Leverage, Profitability, and Size, to provide credit/liquidity analysis for over 370 public Cannabis/Hemp companies.

Viridian publishes weekly insights on debt capital raises in the Cannabis/CBD/Psychedelic industries. These insights typically highlight the most interesting/meaningful debt transactions of that week, and commentary on market conditions, debt deal structures, and lenders.