OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Viridian publishes weekly data and analysis on debt capital raises in the Cannabis/CBD/Psychedelic industries. This data includes information about the company issuing debt (public/private, state/country location), deal size, deal structure, pricing, warrants, and credit data.

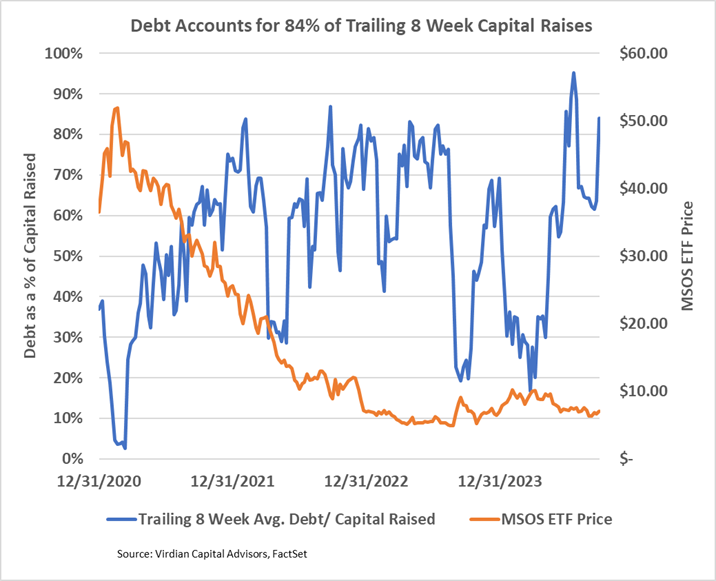

- Debt accounted for 84% of trailing 8-week capital raises. The ratio may go down if companies are able to utilize favorable regulatory-induced stock price increases to complete equity issues. However, equity pricing has remained stubbornly low while the cannabis debt capital markets have reopened.

- The Week’s Debt Transactions

- On September 25, 2024, 4Front Ventures (FFNT: CSE)(FFNTF: OTCQX), the 17th largest U.S. MSO by market cap, closed a $.850M financing with Altmore Capital and an amendment of its loan agreement dated October 16, 2023. An additional $1.75M will be available to the company at the lender’s discretion.

- FFNT also announced that it had retained Canaccord Genuity to lead its ongoing efforts to “consolidate and streamline its capital structure.” Canaccord’s immediate focus will be to explore refinancing existing debt and raising new growth capital.

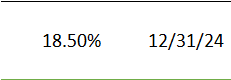

- The debt has an initial maturity date of 12/31/24 but can be extended in certain circumstances, such as the extension of the maturity of subordinated debt. In connection with the loan, the company agreed to double the number of restricted stock units issued to the lender to 49.96M.

- Interest on the debt accrues at a minimum rate of 18.5% plus an additional 5% in PIK interest for a total rate of 23.5%.

- The extension seems aimed at providing FFNT with sufficient liquidity to allow Cannacord to come up with a more global restructuring of the company’s liabilities.

- FFNT is ranked #20/31 on the Viridian Credit Tracker model due to poor liquidity and leverage rankings.

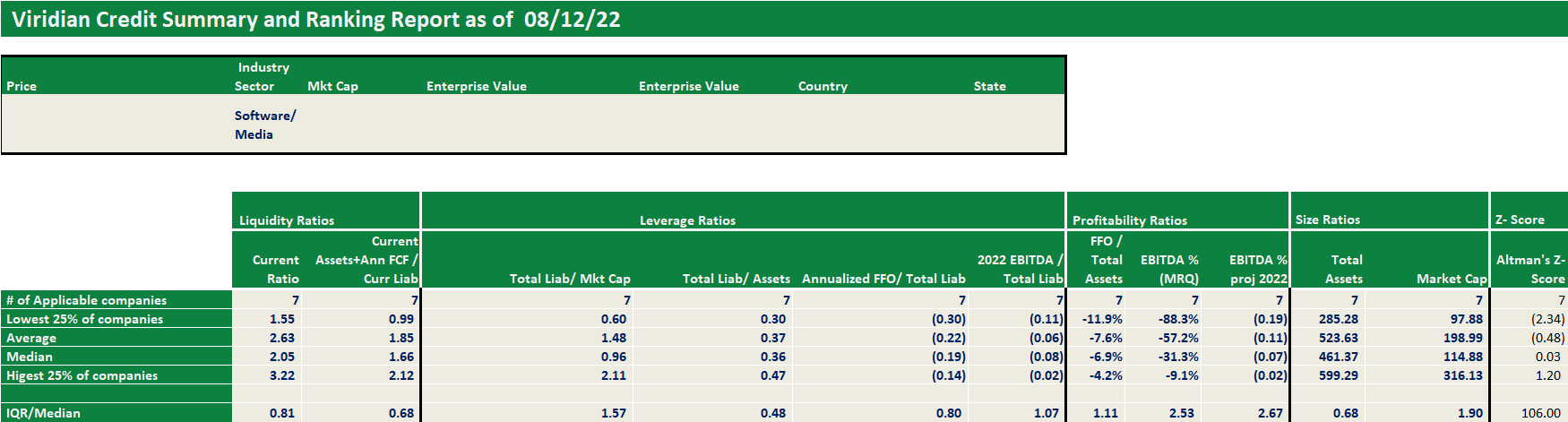

Each week, Viridian highlights a specific industry sector and provides a deep dive into credit metrics and comparable company credit rankings for public companies operating in that sector. Credit ratings are not currently available for public cannabis companies leaving companies, lenders, and investors with a gap of information. The Viridian Cannabis Credit Tracker fills this gap. The model uses 11 market and financial statement variables to discern 4 key credit factors: Liquidity, Leverage, Profitability, and Size, to provide credit/liquidity analysis for over 370 public Cannabis/Hemp companies.

Viridian publishes weekly insights on debt capital raises in the Cannabis/CBD/Psychedelic industries. These insights typically highlight the most interesting/meaningful debt transactions of that week, and commentary on market conditions, debt deal structures, and lenders.