OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Viridian publishes weekly data and analysis on debt capital raises in the Cannabis/CBD/Psychedelic industries. This data includes information about the company issuing debt (public/private, state/country location), deal size, deal structure, pricing, warrants, and credit data.

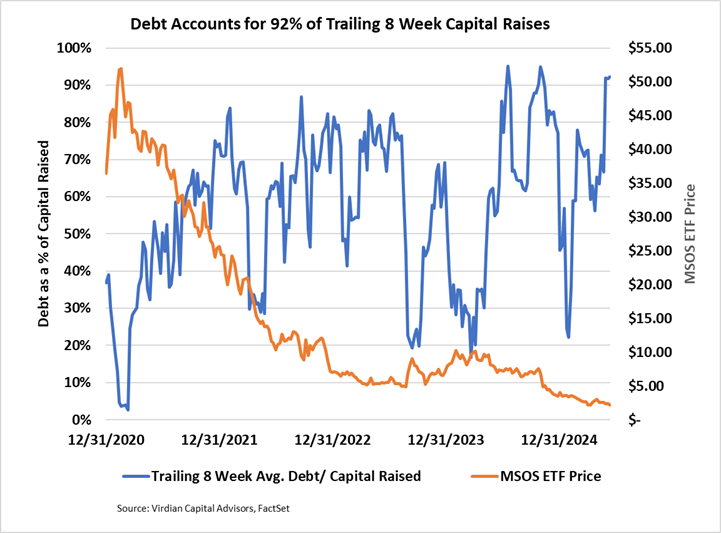

- Debt accounted for 92% of trailing 8-week capital raises. The ratio may go down if companies are able to utilize favorable regulatory-induced stock price increases to complete equity issues. However, equity pricing has remained stubbornly low while the cannabis debt capital markets have reopened.

- The Week’s Debt Transactions

- On June 9, 2025, Advanced Flower Capital (AFCG: Nasdaq) closed a $20 million increase in its senior secured revolving credit facility, bringing the total to $ 50 million.

- The credit facility, with a lead commitment from a $ 75 billion+ FDIC-insured bank, can be expanded up to $100 million, subject to lender participation and the availability of the borrowing base.

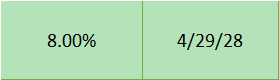

- The loan matures on 4/29/28 and is priced at Prime + 0.50%, subject to a Prime floor of 6.50 (currently resulting in an 8% rate)

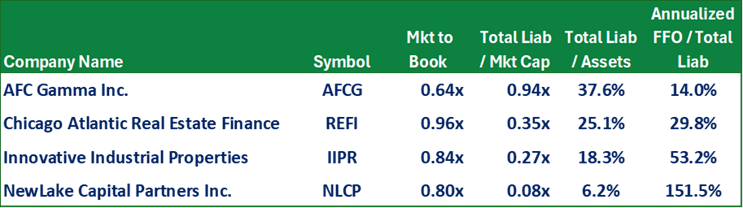

- The chart below displays key credit metrics for the four primary competitors in Viridian’s Real Estate sector, listed in ascending order of creditworthiness according to the Viridian Credit Tracker model. AFCG is the weakest based on all three leverage indicators: total liabilities to market cap, Total liabilities to assets, and Annualized funds from operations to total liabilities. Similarly, AFCG’s market-to-book ratio is the lowest among the four. This indicator can be confusing. On the one hand, it can be an indicator of the market’s view on the adequacy of loan loss reserves, as all other things being equal, with relatively short maturities, one would expect both REFI and AFCG to trade near par. A significant discount could indicate an expectation of future write-offs. Another way to interpret this ratio is that, in theory, the market-to-book ratio should be close to one if the firm’s Return on Equity is close to the required Return on Equity. In that reading, a sharp discount could mean that the company’s earnings do not meet its risk-adjusted required return.

- The 8% pricing of this loan seems attractive given our ranking of AFCG’s relative credit quality. Also, the company’s. 5.75% notes due 2027 were offered at a yield of about 8.69% last week. Chicago Atlantic priced a $50 million unsecured term loan at 9% in October 2024; however, it is challenging to account for the value of AFCG’s senior secured position. Meanwhile, IIPR 5,5s of 2026 are offered at around 7.17%

Each week, Viridian highlights a specific industry sector and provides a deep dive into credit metrics and comparable company credit rankings for public companies operating in that sector. Credit ratings are not currently available for public cannabis companies leaving companies, lenders, and investors with a gap of information. The Viridian Cannabis Credit Tracker fills this gap. The model uses 11 market and financial statement variables to discern 4 key credit factors: Liquidity, Leverage, Profitability, and Size, to provide credit/liquidity analysis for over 370 public Cannabis/Hemp companies.

Viridian publishes weekly insights on debt capital raises in the Cannabis/CBD/Psychedelic industries. These insights typically highlight the most interesting/meaningful debt transactions of that week, and commentary on market conditions, debt deal structures, and lenders.