OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Viridian publishes weekly data and analysis on debt capital raises in the Cannabis/CBD/Psychedelic industries. This data includes information about the company issuing debt (public/private, state/country location), deal size, deal structure, pricing, warrants, and credit data.

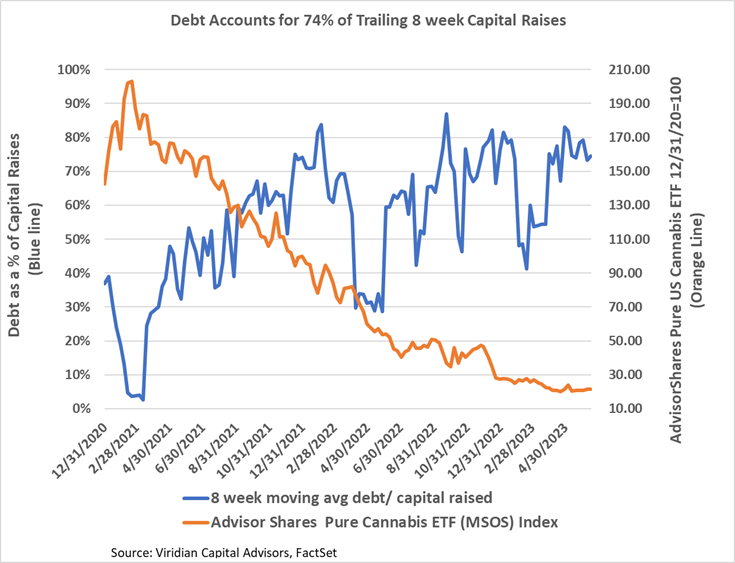

- Debt accounted for 74% of trailing 8-week capital raises. We expect this ratio to be volatile because of the limited capital raise activity. With cannabis stocks trading at or near their 52-week lows, we expect debt to continue to account for more than 50% of capital raises. Several large MSOs have now come close to maxing out their debt capacity and may be forced to issue equity, even at the cost of dilution. See our Insights section for more explanation.

The Week’s Only Closed Debt Issue:

- On June 13, 2023, Humble & Fume (HMBL: CSE)(HUMBF: OTCQX), a Canadian distributor of cannabis and cannabis-related products whose operations include distribution of cannabis accessories, contract manufacturing, packaging, and distribution of concentrate products, announced the closing of a US$1.1M private placement of convertible debenture units.

- The debentures have a 10% coupon, mature in three years, and are convertible at US$.045 (a 50.4% premium)

- The units include 50% warrant coverage with three-year maturities and an exercise price of US$.06 (a 100.54% premium)

- The conversion option and warrants are valued at approximately 8.46 points of bond value and produce an effective cost of 13.48%. This is a reasonable cost for a company with roughly $8M enterprise value, proforma debt/ market cap of 1.5x, and adequate proforma liquidity with a free cash flow adjusted current ratio of 2.5x. The fact that insiders purchased 1,150 of the 1,540 debenture units (74.7%) probably helped keep the effective cost down.

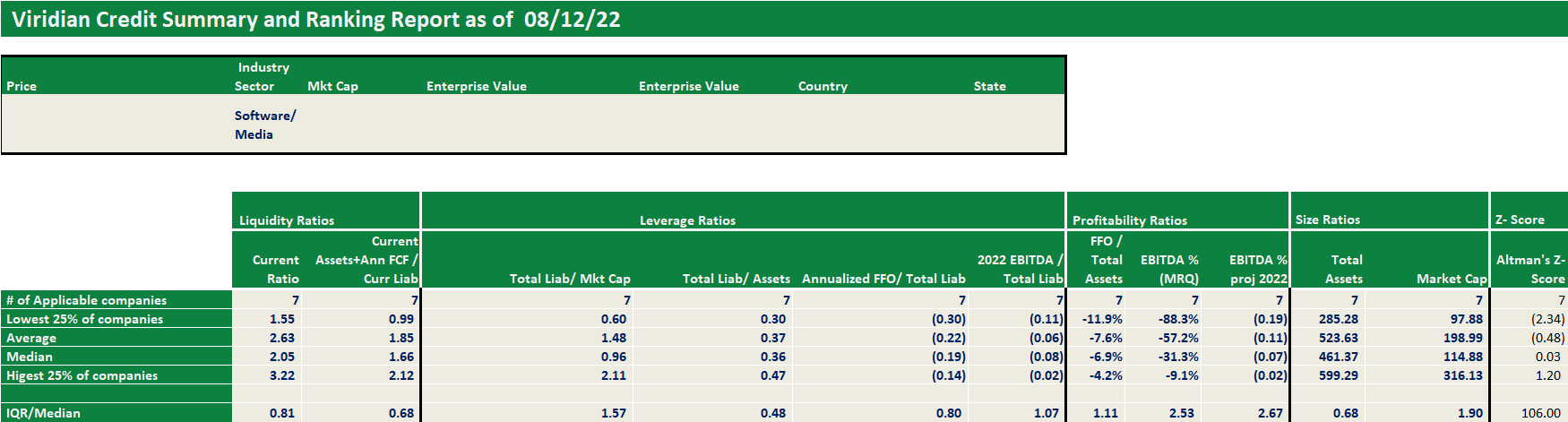

Each week, Viridian highlights a specific industry sector and provides a deep dive into credit metrics and comparable company credit rankings for public companies operating in that sector. Credit ratings are not currently available for public cannabis companies leaving companies, lenders, and investors with a gap of information. The Viridian Cannabis Credit Tracker fills this gap. The model uses 11 market and financial statement variables to discern 4 key credit factors: Liquidity, Leverage, Profitability, and Size, to provide credit/liquidity analysis for over 370 public Cannabis/Hemp companies.

Viridian publishes weekly insights on debt capital raises in the Cannabis/CBD/Psychedelic industries. These insights typically highlight the most interesting/meaningful debt transactions of that week, and commentary on market conditions, debt deal structures, and lenders.