OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Viridian publishes weekly data and analysis on debt capital raises in the Cannabis/CBD/Psychedelic industries. This data includes information about the company issuing debt (public/private, state/country location), deal size, deal structure, pricing, warrants, and credit data.

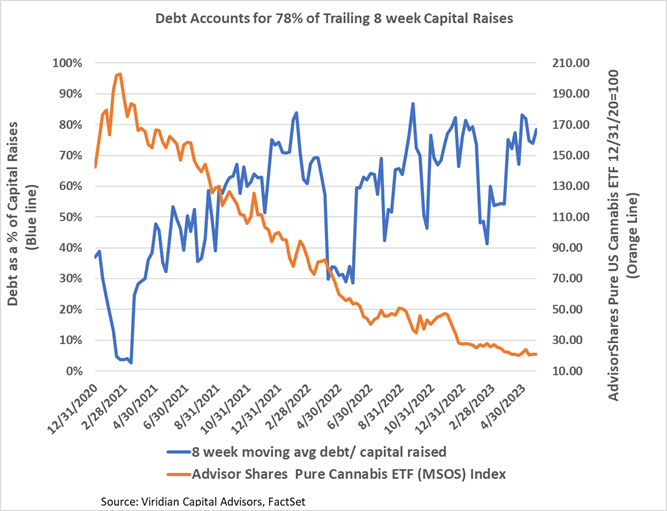

- Debt accounted for 78% of trailing 8-week capital raises. We expect this ratio to be volatile because of the limited capital raise activity. With cannabis stocks trading at or near their 52-week lows, we expect debt to continue to account for more than 50% of capital raises. Several large MSOs have now come close to maxing out their debt capacity and may be forced to issue equity, even at the cost of dilution. See our Insights section for more explanation.

The Week’s Largest Closed Debt Issue:

- On 5/25/23, Tilray Brands, Inc. (TLRY: Nasdaq)(TLRY: TSX), the world’s third largest cannabis company by market cap, raised $150M through a registered offering of Unsecured Convertible Senior Notes.

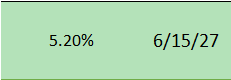

- The notes have a coupon of 5.2%, a maturity date of June 15, 2027, and a conversion price of $2.66 (a 12.7% premium to the pre-announcement stock price).

- The low-premium and long-dated conversion option is worth nearly 22 points of bond value, raising the effective cost to 12.3%.

- Tilray will use $138M of the proceeds to fund a repurchase of $135M principal amount of Tilray’s Convertible Senior Notes due in 2023 and 2024 in a transaction negotiated with the holders of the notes.

- Our credit ranking model ranks Tilray as the 3rd best credit among the nine global cannabis companies with market caps over $500m. The company has relatively good liquidity, low leverage, and many ancillary assets that it might be able to peel off if necessary. Still, there is plenty of room for skepticism: Tilray has stagnant sales and declining market shares in its home cannabis market and has maintained its liquidity by selling over $1B in stock over the last five years. Its core strategy of moving into the U.S. market as soon as possible is deeply flawed. Legislation that would allow this is likely for years, and more importantly, there is no reason to believe Tilray could compete successfully against entrenched U.S. competitors. It’s a reasonable credit, but we view it as a melting ice cube, insufficiently cash generative to maintain itself without ongoing dilutive equity issues.

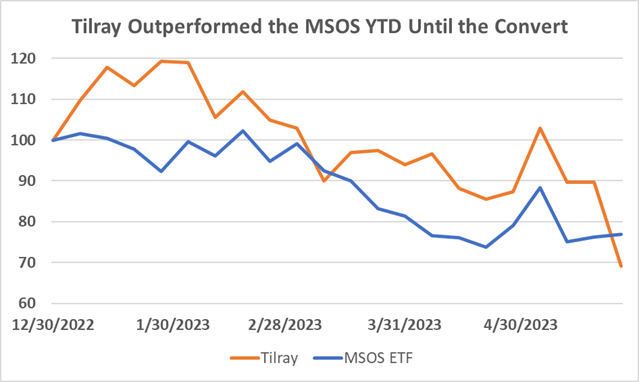

- The market treated Tilray more favorably than the MSOS ETF for most of this year, but the graph below shows that the company’s stock has collapsed by around 30% since the end of April.

- One of the reasons the market reacted so negatively to this week’s convertible debt issue was an unusual feature of the deal. Tilray entered into a share lending arrangement with an affiliate of Jeffries (“The Share Borrower”), under which it will lend to the SB 38.5M shares. Purchasers of the Notes can separately sell up to the 38.5M shares of the company that they borrow from the S.B. This facility basically promotes shorting of Tilray’s stock as a hedge for the purchase of the Converts. It is no secret that arbs frequently buy converts and short shares against their investment, but setting up a facility to promote this activity is rare. It is tantamount to an admission that there are insufficient real investors in Tilray securities. No wonder the stock traded off sharply!

Each week, Viridian highlights a specific industry sector and provides a deep dive into credit metrics and comparable company credit rankings for public companies operating in that sector. Credit ratings are not currently available for public cannabis companies leaving companies, lenders, and investors with a gap of information. The Viridian Cannabis Credit Tracker fills this gap. The model uses 11 market and financial statement variables to discern 4 key credit factors: Liquidity, Leverage, Profitability, and Size, to provide credit/liquidity analysis for over 370 public Cannabis/Hemp companies.

Viridian publishes weekly insights on debt capital raises in the Cannabis/CBD/Psychedelic industries. These insights typically highlight the most interesting/meaningful debt transactions of that week, and commentary on market conditions, debt deal structures, and lenders.