OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Viridian publishes weekly data and analysis on debt capital raises in the Cannabis/CBD/Psychedelic industries. This data includes information about the company issuing debt (public/private, state/country location), deal size, deal structure, pricing, warrants, and credit data.

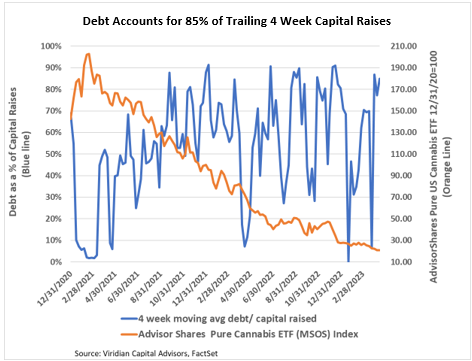

- Debt accounted for 85% of trailing 4-week capital raises. We expect this ratio to be volatile because of the limited capital raise activity. With cannabis stocks trading at or near their 52-week lows, we expect debt to continue to account for more than 50% of capital raises. Since year-end, debt costs have significantly increased because of higher treasury rates and risk spreads. We expect continued increases in equity-linked structures.

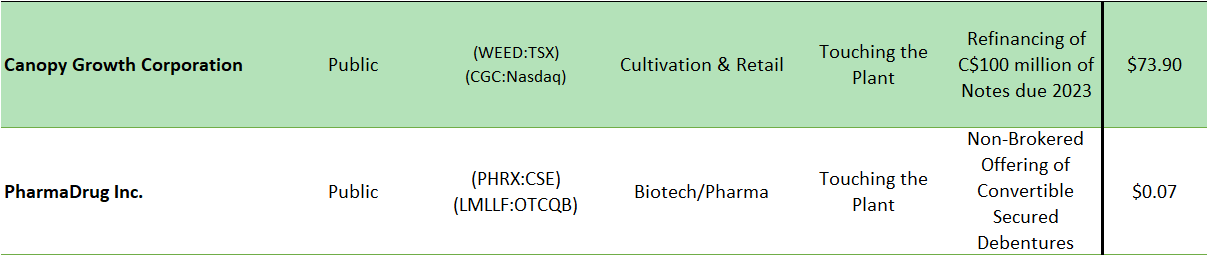

The Week’s Largest Debt Raise:

-

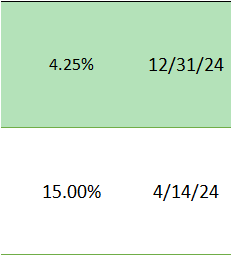

- On April 14, 2023, Canopy Growth Corporation (CGC: Nasdaq)(WEED: TSX), the second largest Canadian L.P. by market cap, agreed with a subsidiary of Constellation Brands to exchange C$100M (US$73.9) of its 4.25% unsecured notes due 2023 for an equal principal note due 12/31/24. Canopy paid all accrued interest on the 2023 notes as part of the refinancing.

- The company announced its intention to create a new class of non-voting, non-participating shares into which it will negotiate to exchange C$100M of the new notes. Details of the exchange have not yet been announced, but it will be interesting to see what value will be placed on the unsecured 4.25% notes.

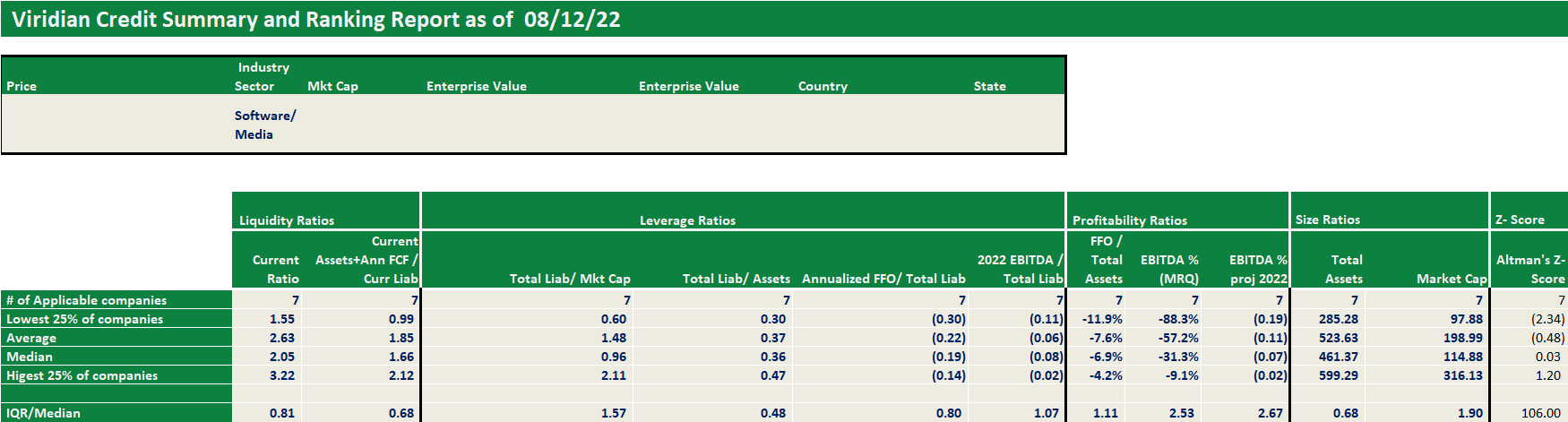

- The Viridian Credit Tracker model ranks Canopy as the thirteenth-best credit among our database’s 22 Canadian Cultivation & Retail companies with market caps over $10M. (See our weekly credit tracker for the detailed ranking.)

- A Tiny But Interesting Second Debt Deal

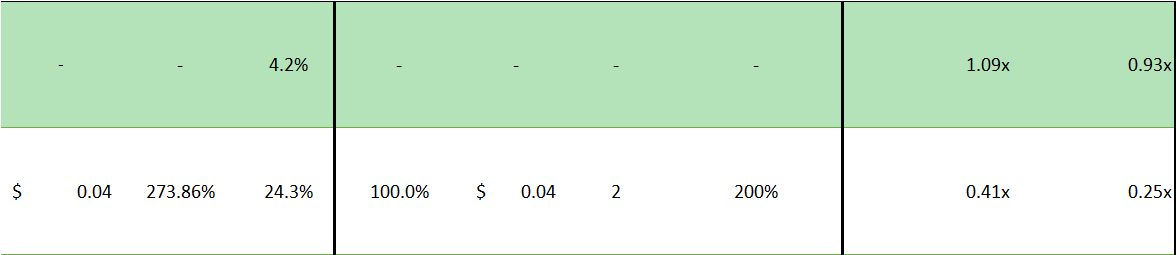

- On April 14, 2023, PharmaDrug Inc. (PHRX: Nasdaq)(LMLLF: OTCQB) closed a $100,000 convertible secured debenture unit deal with some intriguing features that combine to produce an eye-popping effective cost of 24.27%.

- The interest rate of 15% is unusually high for a convertible note; however, the conversion premium of 274% renders the conversion option virtually worthless, given the one-year maturity.

- The units also included 100% warrant coverage with two-year maturities. Curiously, the exchange premium on the warrants is also set at 274%, reducing the value of the warrants to 1 basis point of bond value.

- The conversion feature and the warrants combine to give 200% total coverage but are both nearly worthless, affecting the total bond net price by less than two basis points.

- The additional feature that does matter is the closing fee of 8%, payable as an offset to the purchase price. This is essentially an 8% OID on a one-year note!

- Just when we thought we had seen it all!

Each week, Viridian highlights a specific industry sector and provides a deep dive into credit metrics and comparable company credit rankings for public companies operating in that sector. Credit ratings are not currently available for public cannabis companies leaving companies, lenders, and investors with a gap of information. The Viridian Cannabis Credit Tracker fills this gap. The model uses 11 market and financial statement variables to discern 4 key credit factors: Liquidity, Leverage, Profitability, and Size, to provide credit/liquidity analysis for over 370 public Cannabis/Hemp companies.

Viridian publishes weekly insights on debt capital raises in the Cannabis/CBD/Psychedelic industries. These insights typically highlight the most interesting/meaningful debt transactions of that week, and commentary on market conditions, debt deal structures, and lenders.