OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Viridian publishes weekly data and analysis on debt capital raises in the Cannabis/CBD/Psychedelic industries. This data includes information about the company issuing debt (public/private, state/country location), deal size, deal structure, pricing, warrants, and credit data.

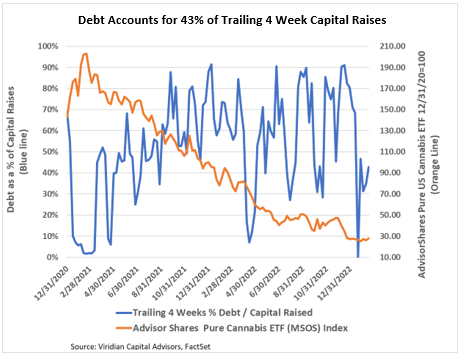

- Debt accounted for 43% of trailing 4-week capital raises. We expect this ratio to be volatile because of the limited capital raise activity. Debt should average over 50% of capital raised, especially since many companies are trading at or close to their 52-week lows. We expect more companies to need to add equity kickers to their debt deals in the current capital-constrained environment.

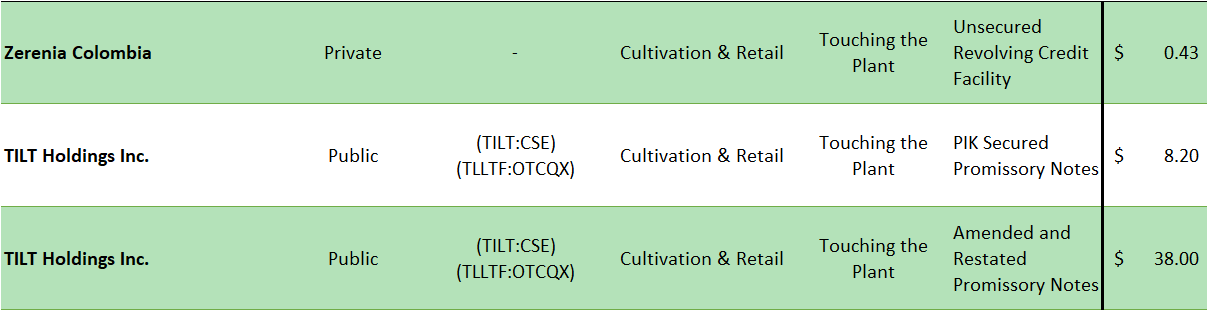

The Week’s Largest Debt Raise:

-

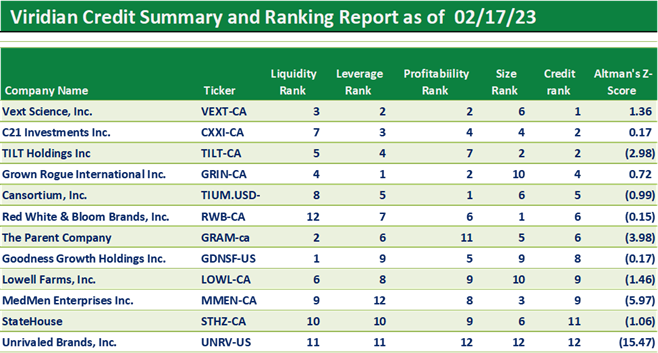

- On February 16, 2023, Tilt Holdings (TILT: NEO)(TLLTF: OTCQX), a diversified enterprise with businesses in vape technology, cultivation, manufacturing, processing, brand development, and retail, announced the completion of three refinancing transactions for total gross proceeds of $61.2M.

- Tilt completed its previously announced $15M sale-leaseback transaction with Innovative Industrial Properties (IIPR: NYSE) on its White Haven, Pennsylvania Facility.

- The company issued $8.2M of PIK secured promissory notes carrying the same interest rate as the notes below. The PIK notes were issued to satisfy outstanding aged accounts payable held by the company’s former Junior Noteholders.

- Tilt amended and extended terms with its junior noteholders to provide for new “amended and restated notes” with a principal balance of $38M.

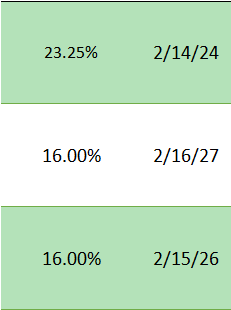

- The notes carry a floating rate at the higher of 16% of prime +8.5% and mature on February 15, 2026.

- Amortization payments of $5 million annually plus 50% of excess cash over $10M will begin in February 2024.

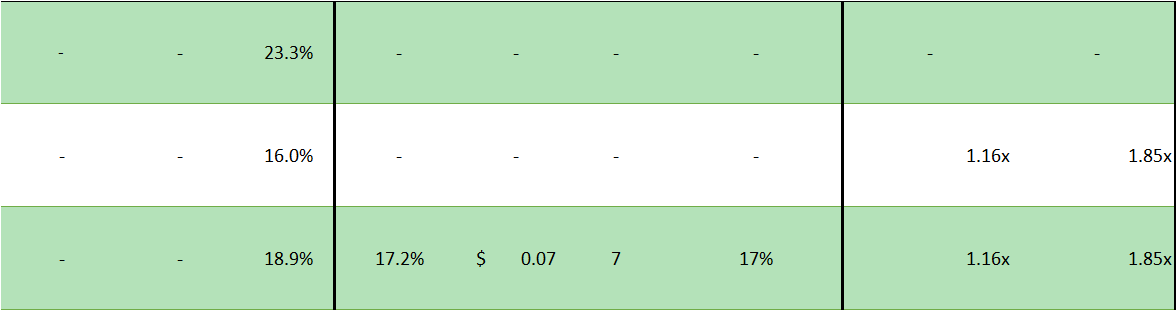

- Noteholders received 92M 7-year warrants with exercise prices of $.07084. The package represents 17.15% warrant coverage at a premium of 5.574%.

- We calculate a value of the warrant package of approximately $2.54M using Black Sholes and a 30% assumed volatility. We calculate effective cost by applying this warrant value as an implied original issue discount of 6.46% and then calculating a yield to maturity of 18.78% without the effect of the amortization payments and 19.14%, including the amortization payments.

- We consider this a good deal for Tilt as it compares favorably to the 19.7% effective yield we calculated for MariMed’s recent loan with Chicago Atlantic, even though MariMed is a superior credit by most objective measures to Tilt. The new Tilt notes contain no prepayment penalties, increasing the relative value vs. the MariMed transaction.

- Our Chart of the Week ranks Tilt as the third-best credit among the 12 U.S. Cultivation & Retail sector companies with market caps between $10M and $75M. The table below shows the Viridian Credit Tracker ranking of the peer group.

- Tilt got these terms partly because Mark Scatterday, a former Tilt CEO and board chairman, owns approximately ½ of the issue. It is unclear whether the concentrated ownership of the notes is positive or negative for the company going forward. Still, to the extent that the relationship with Mr. Scatterday remains friendly, it could make obtaining covenant amendments easier, should they be required.

- Tilt is an outstanding example of a company that spent nearly a year crafting and negotiating a resolution to a problematic liquidity issue and came out with significantly improved credit.

Each week, Viridian highlights a specific industry sector and provides a deep dive into credit metrics and comparable company credit rankings for public companies operating in that sector. Credit ratings are not currently available for public cannabis companies leaving companies, lenders, and investors with a gap of information. The Viridian Cannabis Credit Tracker fills this gap. The model uses 11 market and financial statement variables to discern 4 key credit factors: Liquidity, Leverage, Profitability, and Size, to provide credit/liquidity analysis for over 370 public Cannabis/Hemp companies.

Viridian publishes weekly insights on debt capital raises in the Cannabis/CBD/Psychedelic industries. These insights typically highlight the most interesting/meaningful debt transactions of that week, and commentary on market conditions, debt deal structures, and lenders.