OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Viridian publishes weekly data and analysis on debt capital raises in the Cannabis/CBD/Psychedelic industries. This data includes information about the company issuing debt (public/private, state/country location), deal size, deal structure, pricing, warrants, and credit data.

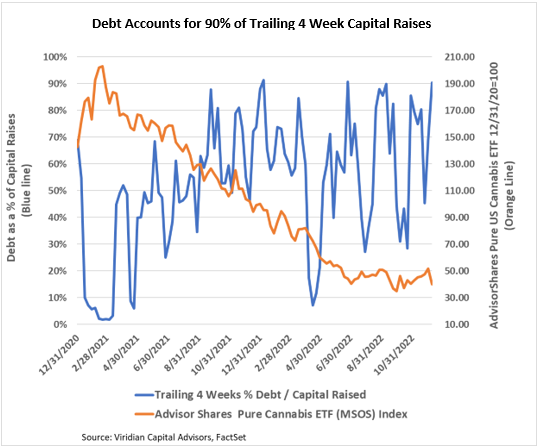

- Debt accounted for 90% of trailing 4-week capital raises. We expect this ratio to be volatile because of the limited capital raise activity. Still, we expect it to average well over 50%, especially since many companies are trading close to their 52-week lows.

The Week’s Largest Debt Raise:

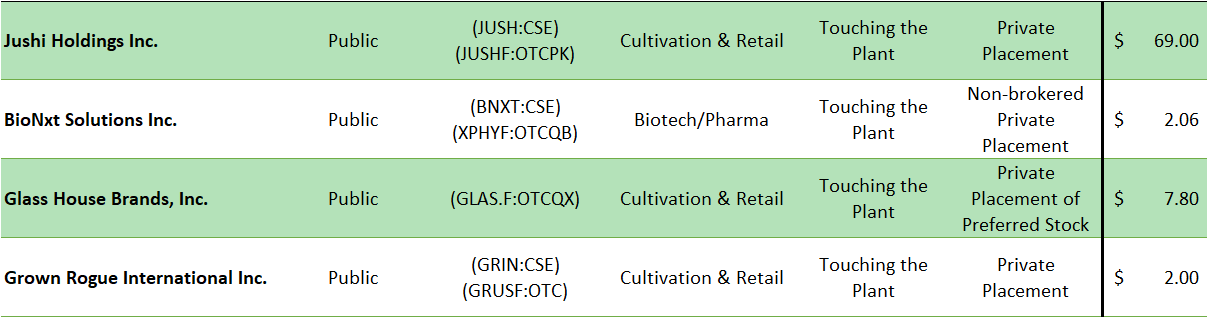

- On December 8, 2022, Jushi Holdings (JUSH: CSE)(JUSHF: OTCQX), the eighth largest U.S. MSO by market cap, closed a private offering of approximately $69M.

-

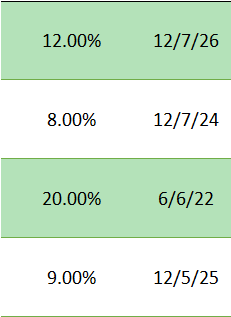

- The notes bear interest at 12.0% and mature on 12/7/2026.

- The notes are secured by second-priority liens and guarantees, subordinate to the company’s $65M first-priority facility with Sunstream. In conjunction with the transaction, Sunstream modified its covenants by removing the total leverage ratio covenant and replacing it with a minimum total revenue covenant. Sunstream received 2M warrants with the same expiry and exercise price as the warrants attached to the new notes.

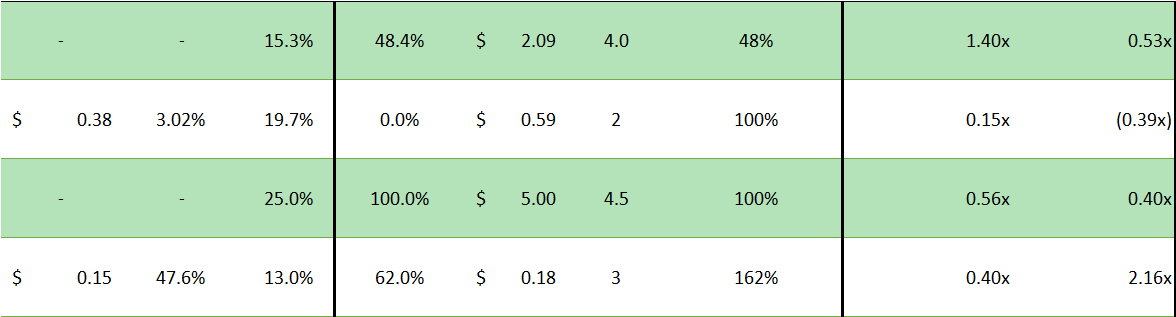

- The new notes have approximately 16M warrants with four-year expiry and an exercise price of $2.086 per share (about 18% premium and 50% coverage).

- The notes are prepayable for the first 24 months after issuance at 105% of the principal plus a make-whole of unpaid interest up through month 24. These prepayment terms make it essentially prohibitive to prepay the notes for the first 18 months at least. After 24 months, the prepayment premium drops to a more manageable 105%.

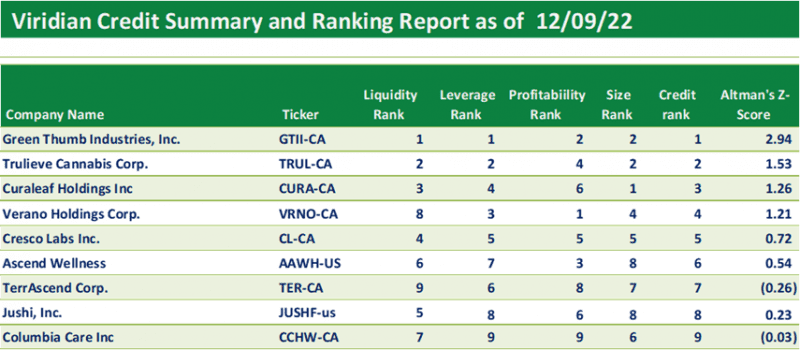

- We estimate the effective cost of this transaction to be 15.27% before any financing fees, which strikes us as appropriate given that Jushi ranks as the 8th strongest credit of the 9 U.S. MSOs with market caps over $300M. This transaction significantly increases Jushi’s financial flexibility by curing a looming debt maturity. The company’s credit profile continues to be penalized by high leverage and small size relative to its peer group, mitigated by its 5th place liquidity ranking and 6th place profitability ranking. We expect Jushi/s credit profile to improve throughout 2023 as it begins to benefit from recent expansionary expenditures.

- Our rankings of the nine largest MSOs are presented in the chart below

-

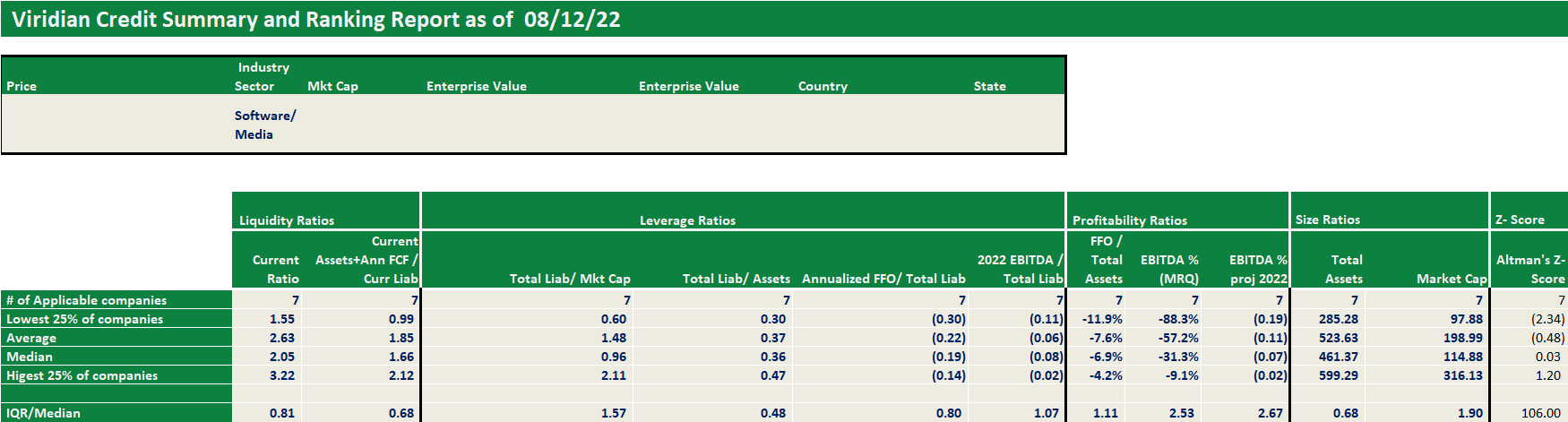

Each week, Viridian highlights a specific industry sector and provides a deep dive into credit metrics and comparable company credit rankings for public companies operating in that sector. Credit ratings are not currently available for public cannabis companies leaving companies, lenders, and investors with a gap of information. The Viridian Cannabis Credit Tracker fills this gap. The model uses 11 market and financial statement variables to discern 4 key credit factors: Liquidity, Leverage, Profitability, and Size, to provide credit/liquidity analysis for over 370 public Cannabis/Hemp companies.

Viridian publishes weekly insights on debt capital raises in the Cannabis/CBD/Psychedelic industries. These insights typically highlight the most interesting/meaningful debt transactions of that week, and commentary on market conditions, debt deal structures, and lenders.