OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Viridian publishes weekly data and analysis on debt capital raises in the Cannabis/CBD/Psychedelic industries. This data includes information about the company issuing debt (public/private, state/country location), deal size, deal structure, pricing, warrants, and credit data.

-

- We saw two odd debt stories this week relating to debt retirement (but maybe we are just too cynical):

- Aurora Cannabis (ACB: Nasdaq)(ACB: TSX) reported repurchasing $102.5M of convertible senior debt at 95.5% of par. Aurora’s stock reacted positively, gaining over 2% on the news. Don’t the stockholders realize what the source of this cash is? Aside from some minor asset sales, stock issuance is the only cash source the company has ever had. For a company that has been negative cash from operations for 15 consecutive quarters to repurchase bonds that are yielding 9.45% doesn’t seem like a reason to cheer! Granted, the bonds mature in Feb 2024 and need to be dealt with, but 95.5% doesn’t seem like enough of a discount.

- In a similar vein, HEXO (HEXO: Nasdaq)(HEXO: TSX) announced that it had repaid the total $40M outstanding amount on its 8% unsecured convertible debentures that matured 12/5/22. “Repaying this debt marks a key milestone as we continue to build investor confidence,” said Charlie Bowman, CEO. Ok, so repaying maturing debt and thereby avoiding bankruptcy is rebuilding investor confidence? How about reversing a 15-quarter string of negative cash flow from operations? That would start to build some confidence.

- We saw two odd debt stories this week relating to debt retirement (but maybe we are just too cynical):

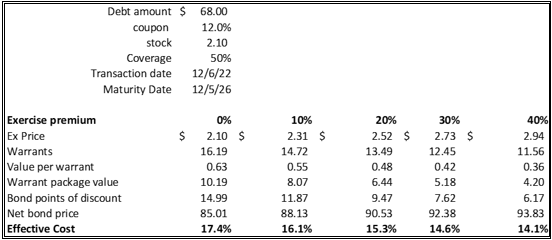

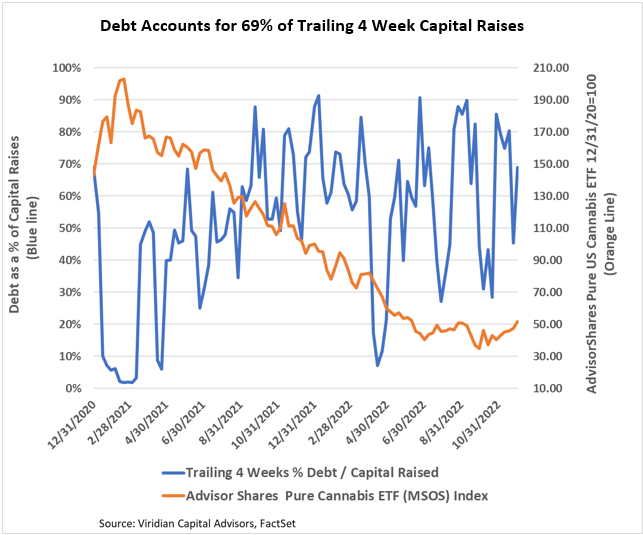

- Debt accounted for 69% of trailing 4-week capital raises. We expect this ratio to be volatile because of the limited capital raise activity but average above 50%. We are still awaiting the final closing of the Jushi (JUSHF: CSE) refinancing, and one critical missing detail is the pricing of the attached warrants. The company expects that the package will include 50% warrant coverage. The table below shows the effective cost of the deal based on a range of warrant exercise premiums.

The Week’s Largest Debt Raise:

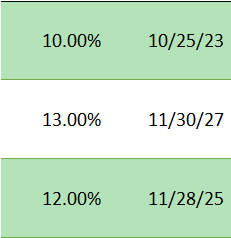

- On November 30, 2022, TerrAscend Corp. (TER: CSE)(TRSSF: OTCQX), the seventh largest U.S. MSO by market cap, announced a $25M borrowing under its amended credit facility with Chicago Atlantic as the agent.

-

-

- The loan bears interest at the greater of Prime plus 6% or 13% and matures on November 1, 2024.

- The loan is prepayable without penalty after 18 months.

- The debentures have a 10% interest rate, mature on November 21, 2024, and are convertible at approximately US$0.037 per share (a 0.5% premium)

- The loan proceeds, plus $30M of cash on hand, were used to repay the $55M outstanding balance on an existing senior secured term loan of $55M from November 2021.

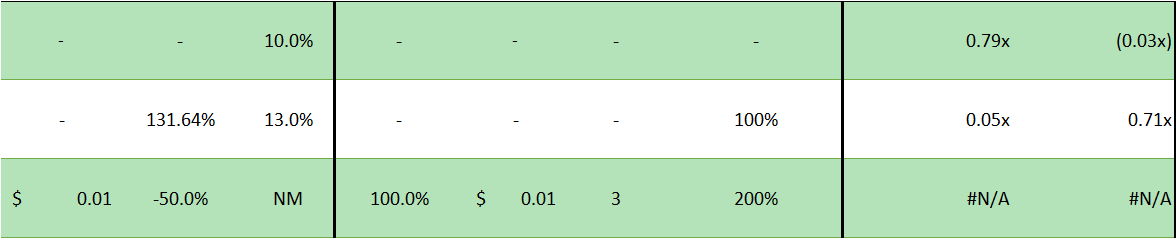

- TerrAscend ranks 6th out of the 8 U.S. MSOs with market caps over $500M on the Viridian Credit Tracker model. TER has the weakest liquidity ranking of the group, with a cash flow adjusted current ratio of only .71x proforma for this issue. TerrAscend also ranks 6th on each of the four leverage variables in the Viridian Credit model. Based on this credit analysis, the 13% rate and 18 months of call protection strike us as attractive terms in today’s credit market.

-

-

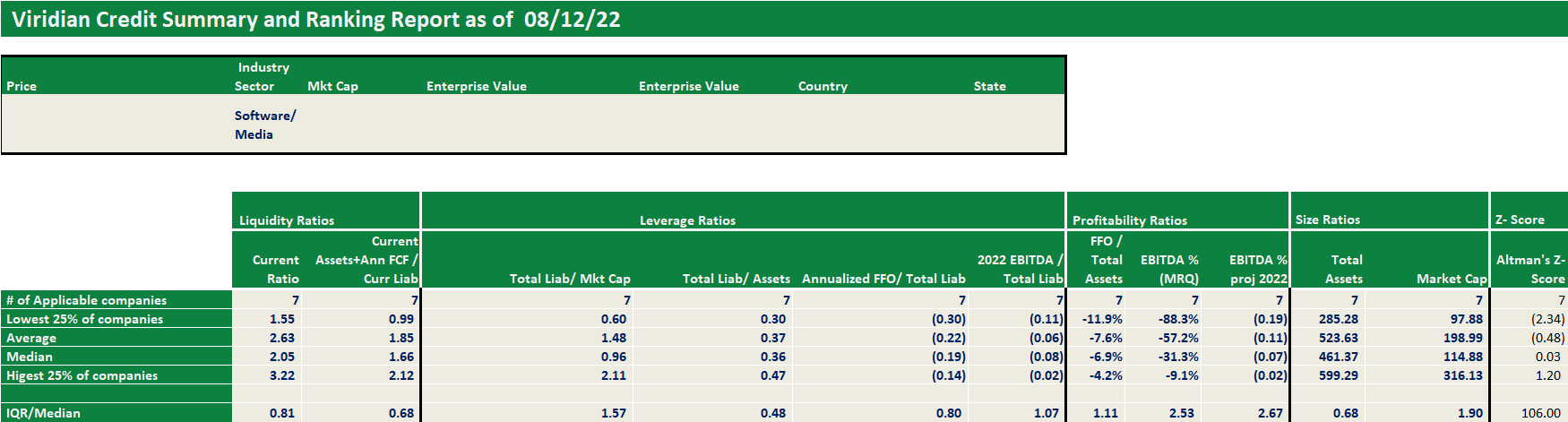

Each week, Viridian highlights a specific industry sector and provides a deep dive into credit metrics and comparable company credit rankings for public companies operating in that sector. Credit ratings are not currently available for public cannabis companies leaving companies, lenders, and investors with a gap of information. The Viridian Cannabis Credit Tracker fills this gap. The model uses 11 market and financial statement variables to discern 4 key credit factors: Liquidity, Leverage, Profitability, and Size, to provide credit/liquidity analysis for over 370 public Cannabis/Hemp companies.

Viridian publishes weekly insights on debt capital raises in the Cannabis/CBD/Psychedelic industries. These insights typically highlight the most interesting/meaningful debt transactions of that week, and commentary on market conditions, debt deal structures, and lenders.