OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Viridian publishes weekly data and analysis on debt capital raises in the Cannabis/CBD/Psychedelic industries. This data includes information about the company issuing debt (public/private, state/country location), deal size, deal structure, pricing, warrants, and credit data.

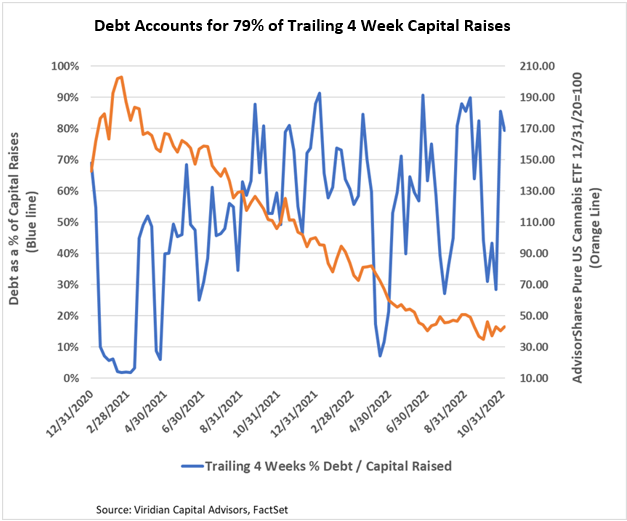

- Debt accounted for 79% of trailing 4-week capital raises. We expect this ratio to be volatile because of the limited capital raise activity but average above 50%. We have noted recently that several MSOs, including TerrAscend, Jushi (JUSH: CSE), and AYR (AYR.A: CSE), have significant refinancings to do based on their debt maturity schedules. Several smaller tier 2 and tier 3 companies have upcoming financing needs that we believe will spur an increase in debt financing.

The Week’s Largest Debt Raise:

- On October 31, 2022, Entourage Health Corp (ENTG: TSX-V)(ETRGF: OTCQX) announced that the amendment and upsized credit agreement with an affiliate of the LiUNA Pension Fund of Central and Eastern Canada providing an additional US$10.99M (C$15M) with the second tranche of C$15M available on January 31, 2023.

-

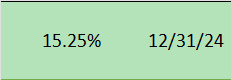

- The facility has a 15.25% rate with a PIK option and matures on December 31, 2024.

-

-

-

- A second lien secures the credit facility on the company’s assets behind Bank of Montreal, the company’s senior lender, whose facility matures on June 30, 2024.

-

-

-

- LiUNA has now amended and increased the loan to Entourage on four separate occasions:

- 12/21 $15.6M

- 4/22 $11.7M

- 6/22 $6.9M

- 10/22 $11.0M

- Proforma for this transaction, LiUNA has lent Entourage approximately $77M, which sits behind about $24M first-priority debt. The pattern is pretty straightforward, Entourage will need more cash in around four months, and the 2nd tranche of this transaction will be ready just in time. We suspect that an arms-length lender would be trying to find ways to get out of this credit. LiUNA owns approximately 20% of Entourage, and its equity would quickly become worthless if it refused to extend more credit. Perhaps, they missed the finance class about “sunk costs.”

- LiUNA has now amended and increased the loan to Entourage on four separate occasions:

-

-

-

- Entourage has had 15 consecutive quarters of negative gross profit, a record we find pretty remarkable. Proforma debt to market cap is approximately 11x, which generally indicates severe distress. Operations cash flow is running about negative $7M per quarter despite not paying interest on the LiUNA facility in cash. These are certainly an ugly set of numbers, and a 15.25% interest rate is not even close to capturing the risk of this debt.

-

-

-

- The obvious question is, what are likely recoveries in this situation? The average EV / annualized revenues for Entourage’s peer group is 1.17x. If we apply this to Entourage’s June quarter, we get an enterprise value of $30.3M. Adding $14M of cash (generous given the cash burn) and subtracting the 1st priority debt of $24M gives a value to the LiUNA debt of $20.3M, a recovery of about 26%. These numbers are only indicative, and we do not have access to the company’s projections. Still, if we were the lending officer responsible for this credit, we would be calculating the “yield to our next job.”

-

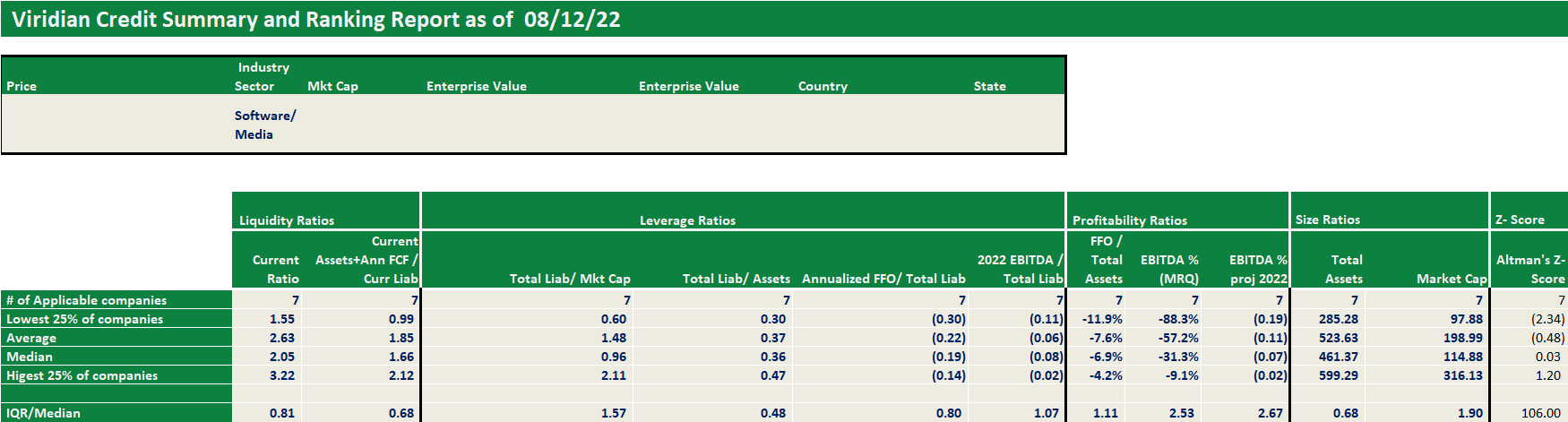

Each week, Viridian highlights a specific industry sector and provides a deep dive into credit metrics and comparable company credit rankings for public companies operating in that sector. Credit ratings are not currently available for public cannabis companies leaving companies, lenders, and investors with a gap of information. The Viridian Cannabis Credit Tracker fills this gap. The model uses 11 market and financial statement variables to discern 4 key credit factors: Liquidity, Leverage, Profitability, and Size, to provide credit/liquidity analysis for over 370 public Cannabis/Hemp companies.

Viridian publishes weekly insights on debt capital raises in the Cannabis/CBD/Psychedelic industries. These insights typically highlight the most interesting/meaningful debt transactions of that week, and commentary on market conditions, debt deal structures, and lenders.