OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Viridian publishes weekly data and analysis on debt capital raises in the Cannabis/CBD/Psychedelic industries. This data includes information about the company issuing debt (public/private, state/country location), deal size, deal structure, pricing, warrants, and credit data.

- Debt accounted for 90% of trailing 8-week capital raises. The ratio may go down if companies are able to utilize favorable regulatory-induced stock price increases to complete equity issues. However, equity pricing has remained stubbornly low while the cannabis debt capital markets have reopened.

- The Week’s Debt Transactions

- On October 23, 2024, Chicago Atlantic Real Estate Finance Inc. (REFI: Nasdaq) close a $50M unsecured four-year term loan with a fixed rate of 9%.

- The lenders were two institutional private lending platforms

- Proceeds will fund future investments and other general corporate purposes.

- The debt was rated BBB+ by Egan Jones.

- Our first impression was that 9% is relatively high for a BBB+ rated debt instrument, and indeed, the BofA BBB corporate bond index is now at 5.29%.

- Despite the yield spread, we congratulate REFI on its ability to attract unsecured credit, a feat that very few cannabis-related credits have achieved.

- On October 24, Entourage Health Corp (ENTG: TSXV)(ETRGF: OTCQX) closed a $1.8M add-on to its Senior Secured Credit Facility with LiUNA Pension Fund of Central and Eastern Canada.

- The new credit extension comes in the context of a forbearance letter waiving the company’s breaches under the facility to October 31, 2024.

- LPF owns more than 10% of the stock of ENTG, giving one plausible, if illogical, reason for LPF’s continued lending.

-

- The Entourage/LPF credit relationship strains the imagination of any credit-trained observer. Starting as a CDN$30M loan in September 2020, the loan has been increased and amended seven times, and now LPF is on the hook for CDN$167.9M, which is one of the clearest examples of good money after bad we have ever witnessed.

- Since 2020, the company has racked up a total of 141.5M in negative EBITDA.

- The company’s CDN$174.8M of debt is now over 7x its total assets! The total liabilities to market cap is over 72x, which is possibly the worst reading we have ever seen. Total assets of CDN$23.9M include only $4.5M of PPE, $11.1M of inventory, and $3M of receivables. In the improbable event that all assets on ENTG’s balance sheet are worth 100% of their stated value, ENTG’s debt would average out to 14% of par value.

- Why in the world would someone be lending new 100-cent dollars that are immediately worth 14 cents? It simply boggles the mind!

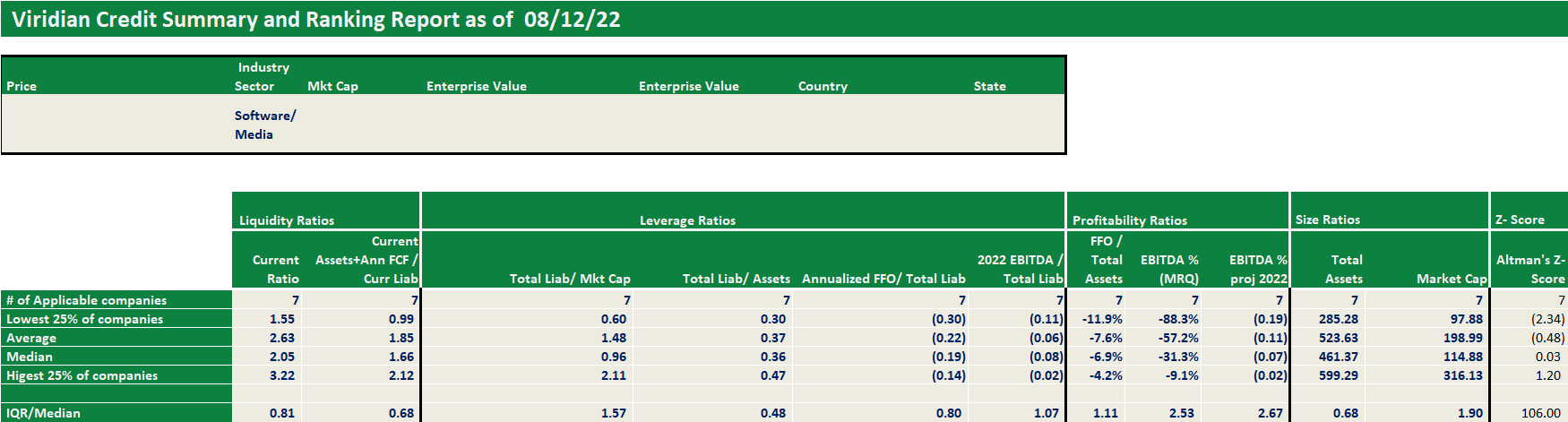

Each week, Viridian highlights a specific industry sector and provides a deep dive into credit metrics and comparable company credit rankings for public companies operating in that sector. Credit ratings are not currently available for public cannabis companies leaving companies, lenders, and investors with a gap of information. The Viridian Cannabis Credit Tracker fills this gap. The model uses 11 market and financial statement variables to discern 4 key credit factors: Liquidity, Leverage, Profitability, and Size, to provide credit/liquidity analysis for over 370 public Cannabis/Hemp companies.

Viridian publishes weekly insights on debt capital raises in the Cannabis/CBD/Psychedelic industries. These insights typically highlight the most interesting/meaningful debt transactions of that week, and commentary on market conditions, debt deal structures, and lenders.