OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Viridian publishes weekly data and analysis on debt capital raises in the Cannabis/CBD/Psychedelic industries. This data includes information about the company issuing debt (public/private, state/country location), deal size, deal structure, pricing, warrants, and credit data.

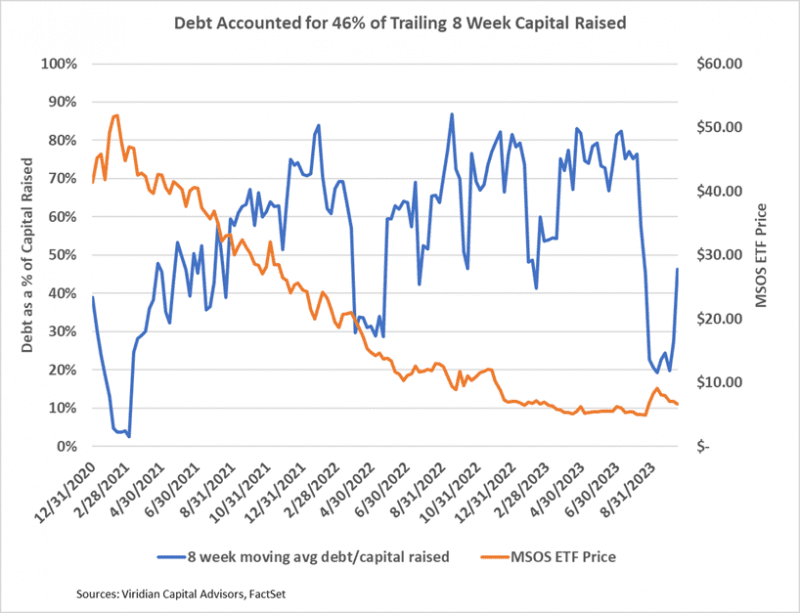

- Debt accounted for 46% of trailing 8-week capital raises, up sharply from last week. We expect this ratio to remain lower than in recent history as companies use the more robust market to issue equity.

- The Week’s Most Interesting Closed Debt Issues

- On October 16, 2023, 4Front Holdings (FFNT: CSE)(FFNTF: OTCQX), the fourteenth largest U.S. MSO by market cap, closed on a $10M senior secured credit facility with Almore Capital’s ALT Debt II, L.P.

- $6M of the facility is immediately available, and the lender has agreed, subject to certain provisions, to make the additional $4M available.

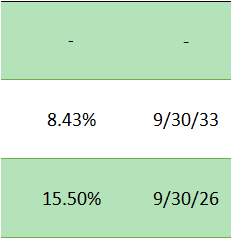

- The loan is priced at the greater of WSJ prime +7% or 15.5%

- The original maturity of the loans is set to December 1, 2023; however, the maturity will be extended, provided the company can extend the maturity of certain other subordinated debt. The loans will mature no later than September 30, 2026. Month amortization payments on the loans begin six months after each loan is made,

- The facility is secured by substantially all of the assets of the company.

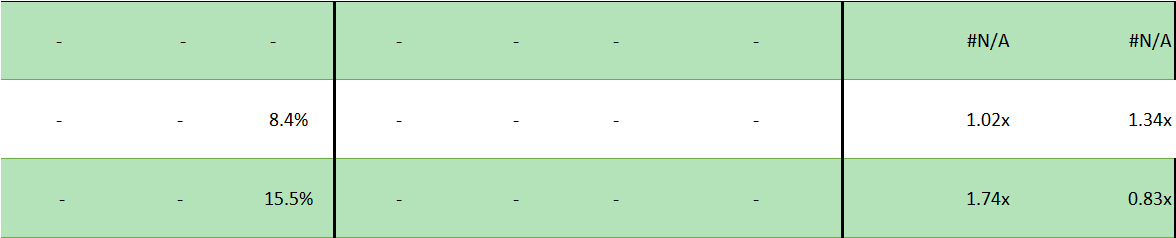

- The loans contain financial covenants, including a minimum liquidity of $3M, a minimum fixed charge coverage of 1.1x, and a maximum consolidated leverage ratio of 3x.

- Under the requirement to extend maturities of other debt, On October 23, 2023, 4Front announced a restructuring of its convertible note with Navy Capital to extend the maturity to October 6, 2024. In exchange for the extension, 4Front increased the interest rate from 6% to 10% and reduced the conversion price from $1.03 to $0.23 (0% premium to current trading prices).

- On October 23, the company also announced that it intends to enter into a restricted stock unit agreement with Altmore for the issuance of a total of 15.9M RSU (which convert to one share each) for C$0.31 per unit (US$0.22)

- 4Front currently has a total debt/2024 EBITDA of approximately 7.0x and ranks nineteen of the twenty-seven U.S. MSOs with market caps over $20M on the Viridian Capital Credit Tracker model. Companies that are ranked as having higher credit quality, including 14th ranked Jushi (JUSHF: OTCQX), 16th ranked Cannabist (CBST: CBOE), and 17th ranked Cansortium (TIUM.USD: CSE) trade at 22.4%, 21.6%, and 18.9% respectively, suggesting the 15.5% pricing on the Altmore debt facility is quite attractive for 4Front.

- The size of the proposed related equity issue is too small to reduce the company’s leverage ratio significantly, and to meet the 3x covenant, the company will likely have to do more extensive equity issuance or debt restructuring. Conversion of the Navy Capital loan should reduce leverage by about .5 turns.

- On October 19, 2023, Cresco Labs (CL: CSE)(CRLBF: OTCQX), the fifth largest U.S. MSO by market cap, closed on a $25.3M conventional mortgage on its three Ellenville, NY properties.

- Approximately $20M of the loan was funded at close, with the remaining held to fund future CAPEX.

- The ten-year mortgage is priced at FHLBank Boston 5-year rate plus 375 bps, resulting in an initial rate of 8.43%

- Cresco is ranked tenth of the twenty-seven MSOs with market caps over $20M in the Viridian Credit Tracker model. Cresco has a total debt/ 2024 EBITDA of approximately 3.9x and should be looking to raise equity. We can’t, however, argue with incurring 8.43% debt, particularly when the company’s 9.5% notes maturing in 2026 are offered at a 16.4% yield.

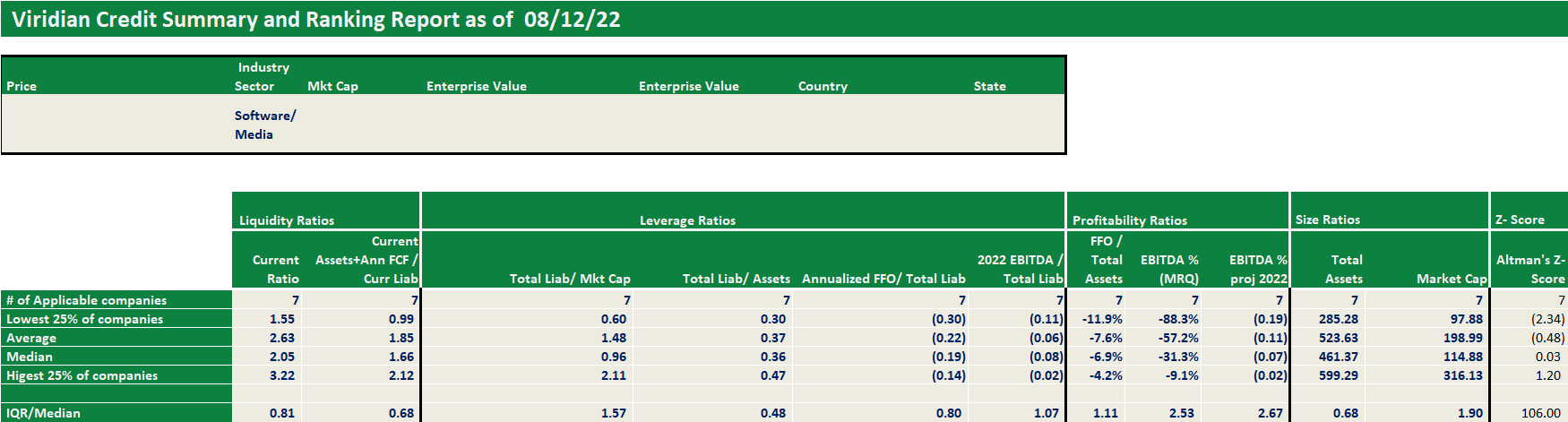

Each week, Viridian highlights a specific industry sector and provides a deep dive into credit metrics and comparable company credit rankings for public companies operating in that sector. Credit ratings are not currently available for public cannabis companies leaving companies, lenders, and investors with a gap of information. The Viridian Cannabis Credit Tracker fills this gap. The model uses 11 market and financial statement variables to discern 4 key credit factors: Liquidity, Leverage, Profitability, and Size, to provide credit/liquidity analysis for over 370 public Cannabis/Hemp companies.

Viridian publishes weekly insights on debt capital raises in the Cannabis/CBD/Psychedelic industries. These insights typically highlight the most interesting/meaningful debt transactions of that week, and commentary on market conditions, debt deal structures, and lenders.