OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Credit ratings are not currently available for public cannabis companies leaving companies, lenders and investors with a gap of information. The Viridian Cannabis Credit Tracker fills this gap. The model uses 11 market and financial statement variables to discern 4 key credit factors: Liquidity, Leverage, Profitability, and Size, to provide credit/liquidity analysis for over 370 public Cannabis/Hemp companies.

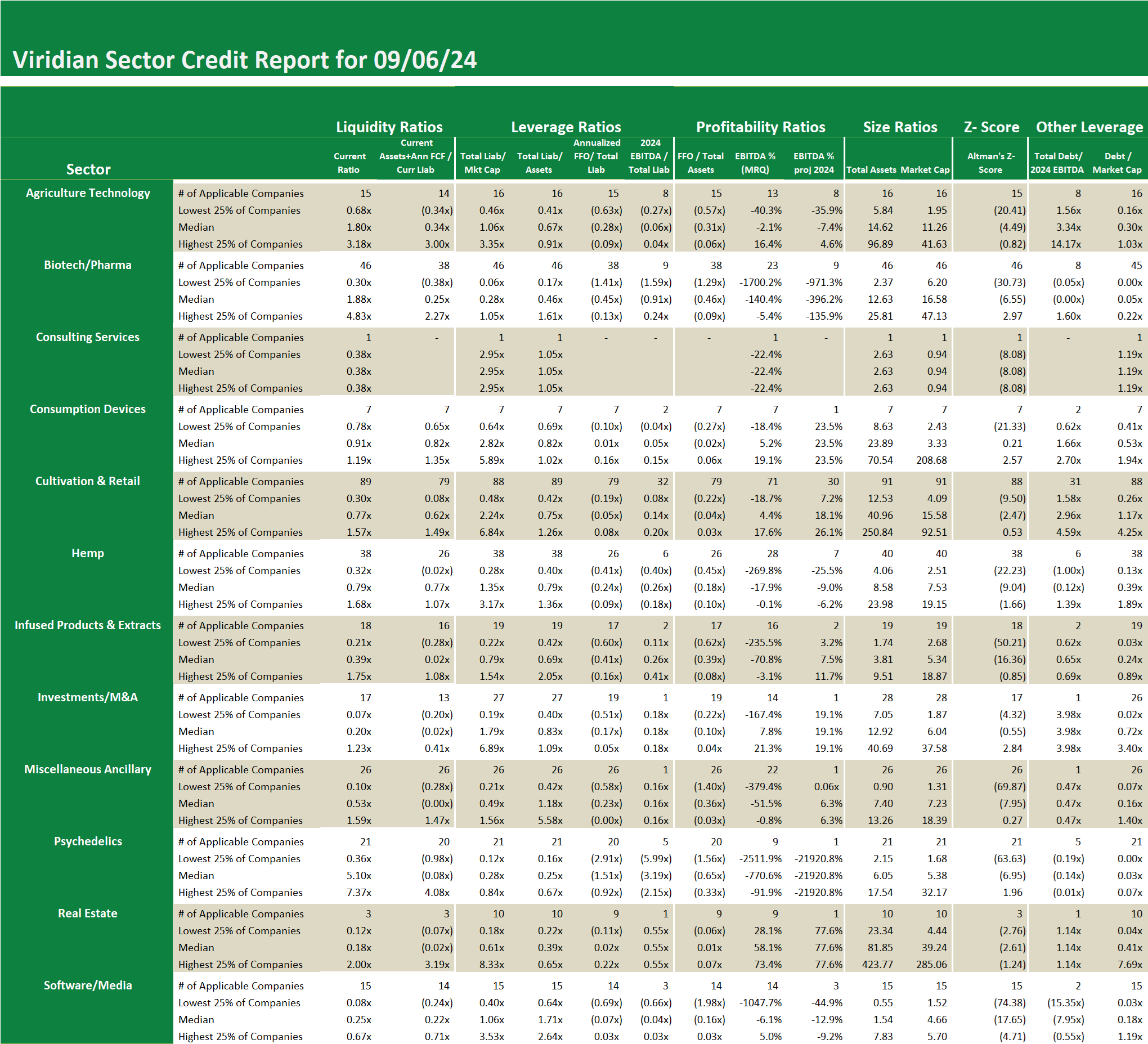

Weekly Sector Credit

- Viridian divides the cannabis universe into twelve subsectors. We continue to note a strong correlation between the liquidity of the subsectors and their leverage.

- The graph below plots nine of the subsectors. We have left out Consulting (only one company) and Real Estate and Investments/M&A (the latter two sectors have financial metrics that are not comparable with the rest).

- Our favored leverage indicator is total liabilities to market cap. We chose this metric because it takes into account all lease and tax liabilities and is indicative of the market’s estimate of the market value asset coverage. The ratio reacts instantly to changes in equity prices rather than waiting for reported financial statements.

- Our chosen liquidity measure is the annualized free cash flow adjusted current ratio. In this bespoke ratio, we add annualized free cash flow to the numerator of the current ratio to adjust for the cash burn (or build) that the companies in the sector are experiencing.

- One notable observation is that the median for all sectors on the graph for liquidity is less than 1x. This indicates that more than ½ of the companies in every sector are likely to need additional financing to discharge their current liabilities. In other words, most cannabis universe companies are not self-funding

- The leverage measure tells a different story. The median total liabilities to market cap for the most levered sector (consumption devices) is still under 3x, a level that does not generally show distress. The median says that at least ½ of the companies are not showing distress, which is why we present the quartiles for each sector. Note that the third quartile measure of total liabilities to market cap for cultivation and retail companies is 6.84x, indicating that at least a quarter of the sector members are bordering on financial distress.

- Why are the two measures correlated? We think it relates to the cash flow and collateral characteristics of the sectors. The lowest levered and least liquid sector, Psychedelics, is generally not suited for leverage since virtually all companies are pre-revenue and have negative cash flow. They also typically lack hard assets like real estate to use as collateral. Without access to the debt markets, these companies need to continually raise new equity capital or sell themselves to stronger, larger concerns. On the other hand, cultivation companies generally have better debt capacity and have more flexibility to maintain liquidity.

Weekly Sector Credit

- Viridian divides the cannabis universe into twelve subsectors. We continue to note a strong correlation between the liquidity of the subsectors and their leverage.

- The graph below plots nine of the subsectors. We have left out Consulting (only one company) and Real Estate and Investments/M&A (the latter two sectors have financial metrics that are not comparable with the rest).

- Our favored leverage indicator is total liabilities to market cap. We chose this metric because it takes into account all lease and tax liabilities and is indicative of the market’s estimate of the market value asset coverage. The ratio reacts instantly to changes in equity prices rather than waiting for reported financial statements.

- Our chosen liquidity measure is the annualized free cash flow adjusted current ratio. In this bespoke ratio, we add annualized free cash flow to the numerator of the current ratio to adjust for the cash burn (or build) that the companies in the sector are experiencing.

- One notable observation is that the median for all sectors on the graph for liquidity is less than 1x. This indicates that more than ½ of the companies in every sector are likely to need additional financing to discharge their current liabilities. In other words, most cannabis universe companies are not self-funding

- The leverage measure tells a different story. The median total liabilities to market cap for the most levered sector (consumption devices) is still under 3x, a level that does not generally show distress. The median says that at least ½ of the companies are not showing distress, which is why we present the quartiles for each sector. Note that the third quartile measure of total liabilities to market cap for cultivation and retail companies is 6.84x, indicating that at least a quarter of the sector members are bordering on financial distress.

- Why are the two measures correlated? We think it relates to the cash flow and collateral characteristics of the sectors. The lowest levered and least liquid sector, Psychedelics, is generally not suited for leverage since virtually all companies are pre-revenue and have negative cash flow. They also typically lack hard assets like real estate to use as collateral. Without access to the debt markets, these companies need to continually raise new equity capital or sell themselves to stronger, larger concerns. On the other hand, cultivation companies generally have better debt capacity and have more flexibility to maintain liquidity.