OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Quick

Links

Past Charts

Home » Viridian Capital Chart of the Week: Will Debt Maturities Trip up the MSOs?

Chart of the Week

Chart of the Week

The Viridian Capital Chart of the Week highlights key investment, valuation and M&A trends taken from that week’s Deal Tracker that we believe are impactful for investors, companies and acquirers.

Week ended 10/06/2023

Viridian Capital Chart of the Week: Will Debt Maturities Trip up the MSOs?

- Nine of the ten largest debt raises ever completed for U.S. Cultivation & Retail companies were closed in 2021 and 2022. Over $4.3B of debt was sold over this period, far more than in any similar period in U.S. Cannabis history. Debt became the largest source of capital to the industry in 2022, and its percentage of total capital raised has increased further in 2023 YTD.

- Corporate financial officers were justifiably reluctant to issue equity during the most severe drawdown the industry has faced. However, this has resulted in several companies with more debt than is sustainable on a long-term basis, particularly in the face of IRS rule 280e. Investors are paying close attention to the MSOs’ ability to repay, extend, or refinance upcoming debt maturities.

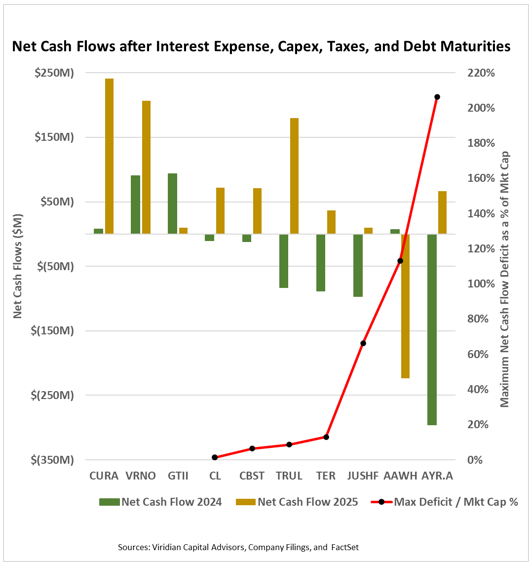

- This week’s graph looks more deeply at MSO liquidity, including debt maturities. We utilized consensus analyst estimates for 2024 and 2025 EBITDA and Capex and 2024 taxes. We assumed that by 2025, rule 280e would be eliminated and calculated taxes at 27% of consensus pre-tax income estimates. 2024 Interest expense was estimated by annualizing 2023 2nd quarter interest expense. We reduced 2025 interest expense by 10% of each company’s projected 2024 debt reduction. Company filings and FactSet provided debt maturity schedules.

- The graphs’ bars represent net cash flows after interest, taxes, CAPEX, and debt maturities. The green bars show the 2024 net cash flow, while the brown bars show the 2025 net cash flow.

- In 2024, Cresco (CL: CSE), TerrAscend (TSND: TSX), and Jushi (JUSHF: OTCQX) were the only three companies to have slight cash flow deficits before debt maturities. All companies on the graph had solidly positive net cash flow before debt maturities in 2025.

- The red line on the graph (measured on the right axis) shows the maximum net cash flow gap as a percent of current market capitalization. Three of the ten companies, including Curaleaf (CURA: CSE), Verano (VRNO: CSE), and Green Thumb (GTII: CSE), have no projected shortfalls in either 2024 or 2025

- Cresco (CL: CSE), Cannabist (CBST: Cboe), Trulieve (TRUL: CSE), and TerrAscend (TSND: TSX) have maximum shortfalls after debt maturities of between 1% and 13% of market cap, levels we believe to be readily financeable.

- Three of the companies on the right have somewhat more worrisome shortfalls. Jushi has a net cash flow shortfall of about $97M in 2024, representing about 66% of its market cap. Ascend (AAWH: OTCQ has a projected shortfall of $224M in 2025, representing 113% of its market cap, and AYR Wellness (AYR.A: CSE) has a 2024 gap of $295M, representing 206% of its current market cap.

- The three companies with significant deficits are likely to temporarily solve the problem by using fees and warrants to induce holders to extend maturities. Lenders are likely to be amenable as none want to face a default on such sizeable outstandings.