OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Quick

Links

Past Charts

Home » Viridian Capital Chart of the Week: Who’s Growing in Florida, and Has the State Gotten Ahead of Itself?

Chart of the Week

Chart of the Week

The Viridian Capital Chart of the Week highlights key investment, valuation and M&A trends taken from that week’s Deal Tracker that we believe are impactful for investors, companies and acquirers.

Week ended 01/26/2024

Viridian Capital Chart of the Week: Who’s Growing in Florida, and Has the State Gotten Ahead of Itself?

- Florida is often considered one of the most critical states in terms of growing legal cannabis sales. The State is estimated to have approximately $2.6B in 2023 legal sales, representing a per capita consumption of about $118 based on the total population or $145 based on adult population.

- The State has a highly developed medical cannabis market. As of 1/26/24, Florida had 871,459 registered active medical cannabis patients, representing 4.9% of its over-18-year-old population, significantly exceeding Pennsylvania, another state teetering on Adult Recreational Use allowance with approximately 4.0%.

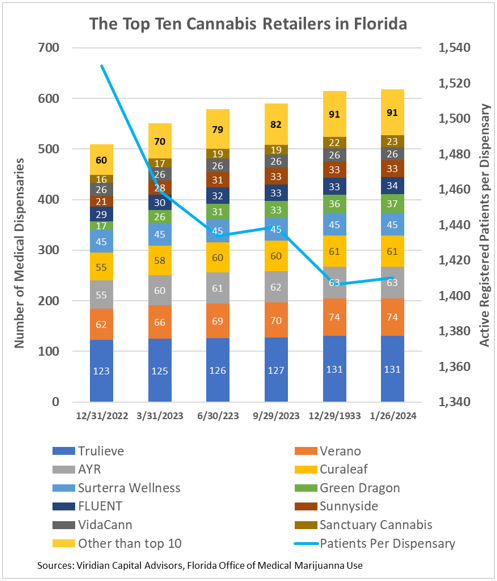

- The bars on the graph show the number of open dispensaries for the top ten competitors in Florida. These companies account for approximately 85% of the total dispensary count, with the following five accounting for an additional 10.5%. Interestingly, neither Green Thumb (GTII: CSE) nor Cannabist (CBST: CBOE) is in the top ten, and other significant MSOs, including Cresco (CL: CSE), TerrAscend (TSND: TSX) and Ascend (AAWH: OTCQX) have no presence in Florida.

- The top five competitors in Florida have made outsized bets on the State with disproportionate percentages of their total national dispensary portfolios: Surterra (88.0%), AYR (70.0%), Trulieve (67.5%), Verano (54.0%), and Curaleaf (41.5%).

- The companies with the highest growth in stores over the last year include Green Dragon (20), Verano (VRNO: CSE) and Sunnyside (12 each), and Trulieve (TRUL: CSE), and AYR (AYR.A: CSE) (8 each). Florida is and will remain a mandatory integrated production state, and as such, the growth in stores is limited by the cultivation capacity of each company.

- Has the State gotten ahead of itself? The blue line on the graph depicts the number of active patients per dispensary, which has dropped by approximately 8% over the last year as dispensary locations grew by 21% while patient counts grew by 12%. Florida’s 1410 patients per dispensary figure compares to 2445 in Pennsylvania, indicating that FL may be temporarily overstored.

- The store growth partially reflects a bet that Florida will become an adult rec market. Florida’s Governor DeSantis believes that adult rec will be on the 2024 ballot in Florida, but the road ahead is still difficult. The state attorney general continues challenging the initiative’s wording and legality under the Florida Constitution. The initiative also needs to achieve a 60% supermajority as it requires an amendment to the State’s constitution. Still, polling indicates support at even higher levels.

- What’s the upside from Adult Rec? Many analysts project a state will at least double its legal cannabis revenues when switching to adult rec. But doubling Florida’s already high medical revenue would require a per capita consumption of approximately $234, significantly higher than that of Illinois or Massachusetts. If Florida matched Massachusetts, sales would only rise by about 70%.

- The top companies in Florida are making a massive bet on the State, with it accounting for more than ½ of their combined national dispensary portfolios. The State has many advantages, and the required vertical integration limits the downside risk of new entrants. Still, it is far from clear that the bet will pay off as handsomely as expected.