OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Quick

Links

Past Charts

Home » Viridian Capital Chart of the Week: Which Leverage Metric Should Investors Keep a Close Eye On?

Chart of the Week

Chart of the Week

The Viridian Capital Chart of the Week highlights key investment, valuation and M&A trends taken from that week’s Deal Tracker that we believe are impactful for investors, companies and acquirers.

Week ended 08/16/2024

Viridian Capital Chart of the Week: Which Leverage Metric Should Investors Keep a Close Eye On?

-

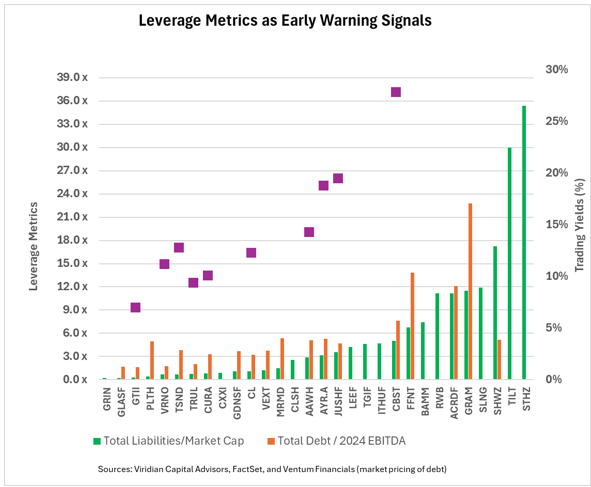

- The cannabis credit markets have come back to life with several major refinancings, including Ascend (AAWH: CSE), TerrAscend (TSND: TSX), and Jushi (JUSHF: CSE). The market has become more sophisticated with a tremendous spread of yields required based on perceived credit quality, ranging from well under 10% for Green Thumb (GTII: CSE) to over 25% for Cannabist (CBST: Cboe).

- The graph shows two leverage metrics: Total Liabilities to Market Cap (green bar) and Total Debt/ 2024 EBITDA (orange bar). The purple squares show offered side trading yields for the debt of each company.

- The graph clearly shows that trading yields are much better correlated with total liabilities to market cap than with Debt/ EBITDA, and the former is an excellent early warning sign of credit difficulties.

- Viridian uses Total Liabilities to Market Cap as the most important of our four leverage ratios for several reasons:

- The metric can be calculated for all public companies, not just the minority of them with sell-side analyst coverage

- The measure is responsive to all information driving equity prices on a daily basis, as opposed to Debt/ EBITDA, which generally changes only quarterly.

- Total liabilities takes into account all balance sheet lease liabilities as well as all recognized tax liabilities.

- The ratio figures prominently in the credit research literature, and a variant is included in several important bankruptcy prediction models, including Altman’s Z-score.

- We view companies with total liabilities to market cap of less than 2x as having significant financial flexibility and strong asset value coverage of liabilities. Companies between 2x and 7x typically do not have high near-term default risk; however, they have lower financial flexibility to withstand an unexpected adverse event and may have significant refinancing risk at debt maturities.

- Investors should monitor total liabilities to market cap as an early warning indicator. It is essential to watch the weekly change in the ratio for consistency in the direction and magnitude of movement. We have been noting, for example, a severe deterioration in the ratio for Schwazze (SHWX: CSE) over the last month.

- We view 7x as a signal of serious risk of default or restructuring. Investors should devote analytical resources to evaluate investment positions in companies over 7x as these companies may have liquidity pressures that may trigger the need for highly dilutive “rescue financing.”

- There is no substitute for a detailed, sophisticated, and regularly updated financial model to anticipate credit pressure points. However, monitoring a straightforward ratio on a consistent basis can provide investors with a valuable early warning sign.