OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Quick

Links

Past Charts

Home » Viridian Capital Chart of the Week: Which Cannabis Companies Have Better Trading Liquidity Compared to Last Year?

Chart of the Week

Chart of the Week

The Viridian Capital Chart of the Week highlights key investment, valuation and M&A trends taken from that week’s Deal Tracker that we believe are impactful for investors, companies and acquirers.

Week ended 04/05/2024

Viridian Capital Chart of the Week: Which Cannabis Companies Have Better Trading Liquidity Compared to Last Year?

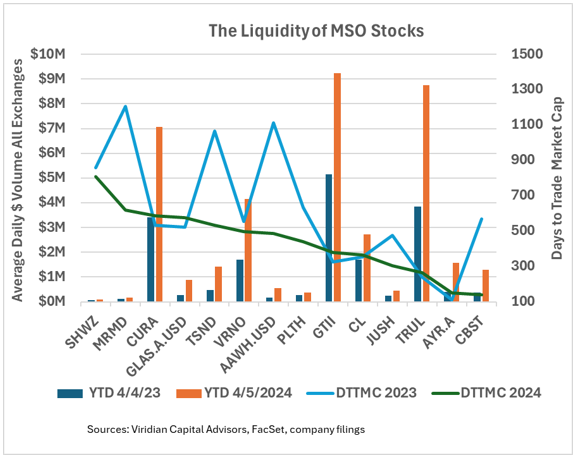

- With a firmer tone to the cannabis equity market and widespread expectations of a transition to Schedule 3, it is easy to assume that cannabis stock liquidity has improved. And for some measures like average daily dollar trading volume, that is doubtlessly true. However, a slightly more sophisticated measure, like the days required to trade the market cap, reveals that some of the largest MSOs have actually lost liquidity since last year.

- The bars on the graph show the average daily dollar trading volume for the YTD period ending 4/5/23 (blue bars) and the YTD period ending 4/5/24 (red bars). All fourteen companies have higher average dollar volume in 2024 than in 2023, and the increase ranges from 25% for Schwazze to 292% for AYR.

- One would expect, though, that at higher valuation levels, dollar trading volume should increase. The lines on the graph indicate the number of days that it would take to trade the ending market cap (DTTMC) of the stock for 2023 (blue line) and 2024 (green line).

- The graph shows that six of the MSOs, including Curaleaf, GlassHouse, GTI, Cresco, Trulieve, and AYR, have higher DTTMC values indicating a decline in actual liquidity. This is quite surprising since these companies are among the largest MSOs with some of the most significant recorded increases in dollar volume.

- Other MSOs like MariMed, TerrAscend, Ascend, and Cannabist have seen quite remarkable increases in liquidity.

- Despite the mixed results, one thing is clear: U.S. Cannabis equity liquidity remains horrendous. For example, if an investor took a 5% position in Curaleaf (DTTMC of 585) and wanted to liquidate their position while remaining under 25% of the daily trading volume, it would take approximately 117 days, which is certainly not the kind of liquidity an institutional investor would expect from a $4B market cap public company. Meanwhile, the equivalent calculation for Tilray is six days.

- All eyes are now on the DEA and the expected rescheduling announcement, but in order to get significantly more institutional investment in the industry, uplisting to senior exchanges remains a key gating item.

- Will a change to schedule 3 allow uplisting? It is not clear; however, we are doubtful. It will arguably take some combination of rescheduling, SAFER, and a Garland memo to do the job.

- Investors should not take their eyes off the broader landscape of cannabis reform. 280e relief is undoubtedly an important step, but it is essential not to lose sight of the long road ahead.