OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Quick

Links

Past Charts

Home » Viridian Capital Chart of the Week: Where Should MSOs Invest – Distressed Investing in Their Own Stocks?

Chart of the Week

Chart of the Week

The Viridian Capital Chart of the Week highlights key investment, valuation and M&A trends taken from that week’s Deal Tracker that we believe are impactful for investors, companies and acquirers.

Week ended 04/04/2025

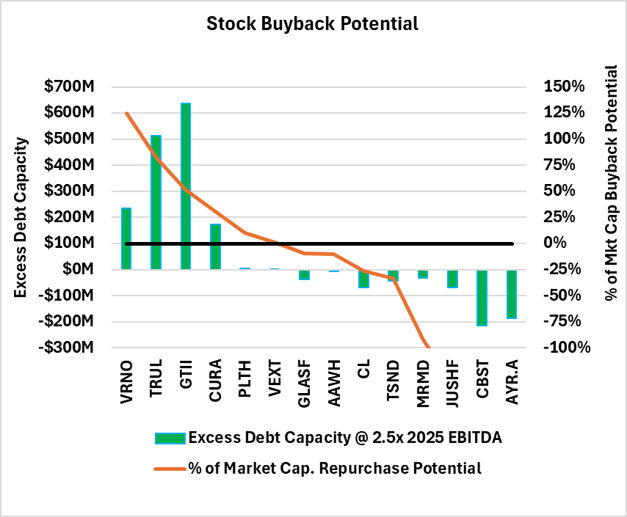

Viridian Capital Chart of the Week: Where Should MSOs Invest – Distressed Investing in Their Own Stocks?

- The Viridian Chart of the Week examines an unpopular hypothesis: Is it possible that the best investment available for several MSOs is stock repurchases?

- First, let’s examine the potential buybacks, and then we will explore the rationale.

- The chart examines the use of excess debt capacity to repurchase stock. We calculated excess debt capacity (indicated by the green bars on the chart) by multiplying consensus 2025 EBITDA estimates by 2.5 and then subtracting existing debt. The 2.5x multiple represents our estimate of maximum sustainable debt capacity in a 280e environment. We did not include leases in our calculation because EBITDA already deducts operating lease costs.

- The orange line divides excess debt capacity by current market cap to determine the theoretical maximum amount of stock that each company could repurchase using its full debt capacity. Note we are not advocating for companies to repurchase anywhere close to these maximum levels.

- On this basis, five companies have sufficient excess debt capacity to repurchase substantial amounts of their own stock. Verano (VRNO: Cboe)(VRNOF: OTCQX) has the theoretical ability to conduct a full share repurchase, while Trulieve (TRUL: CSE)(TCNNF: OTCQX) and GTI (GTII: CSE)(GTBIF: OTCQX) can theoretically repurchase more than 50% of their stock.

- Why is this opportunity available, and why should these companies consider expanding their buyback programs?

- The stock prices of the companies on the chart have declined between 1.9% for Vext (VEXT: CSE)(VEXTF: OTCQX) and 72.0% for AYR (AYR.A: CSE)(AYRWF: OTCQX), with a median decline of 37.5% and an aggregate decline in total market value of 41.3%.

- Analysts have reduced 2025 Estimates for the group by 8.9% since the beginning of 2025 and now project 2025 EBITDA to be 3.9% lower than 2024. The bottom line is that cash flows are down much less than stock prices.

- Recent financings by Verano (VRNO: Cboe)(VRNOF: OTCQX) and Grown Rogue (GRIN: CSE)(GRUSF: OTC) confirm that the cannabis debt capital markets remain open for business. Conversely, the cannabis equity capital market for plant-touching companies is arguably closed.

- The five companies on the left side of the graph, Verano, Trulieve, GTI, and Curaleaf (CURA: TSX)(CURLF: OTCQX), are arguably underleveraged with debt-to-2025 EBITDA ratios ranging from 0.72x for GTI to 1.93x for Curaleaf.

- So what should a company do? The obvious and generally held opinion is to hunker down, strive to maximize free cash flow, and wait for the storm to pass. Another possibility is to invest in non-traditional areas:

- Curaleaf, GTI, and Trulieve are all investing in the hemp-based THC beverage market.

- Curaleaf stands virtually alone in its investment in international markets.

- However, there is one area of potential investment where the risks of new products and the risks of M&A integrations are not present: buying back your own stock.

- Company management has an informational asymmetry advantage. No outside analyst can match the information available to management regarding the set of investable projects available to the company and the IRRs associated with those projects. They are in the best position to calculate the intrinsic value of their shares and assess the potential return from repurchases.

- Investors should pay close attention to what companies do regarding share buybacks. Increasing repurchases is a powerful signal that management believes in its strategy and potential. When stocks are down this much, companies should consider this option.