OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Quick

Links

Past Charts

Home » Viridian Capital Chart of the Week: The Market is Showing Healthy Skepticism Regarding Rescheduling and SAFE

Chart of the Week

Chart of the Week

The Viridian Capital Chart of the Week highlights key investment, valuation and M&A trends taken from that week’s Deal Tracker that we believe are impactful for investors, companies and acquirers.

Week ended 03/08/2024

Viridian Capital Chart of the Week: The Market is Showing Healthy Skepticism Regarding Rescheduling and SAFE

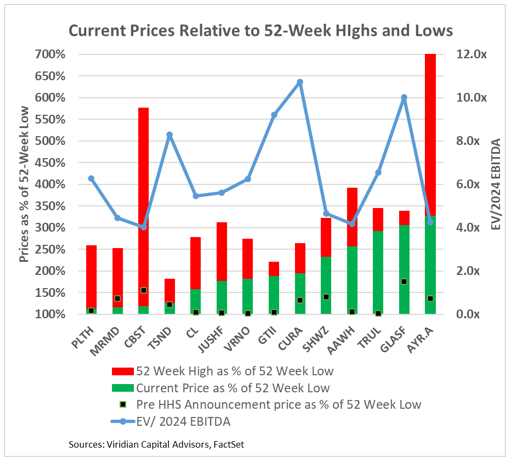

- Cannabis stocks (as measured by the MSOS ETF) hit their 52-week lows on 8/25/23, just before the HHS rescheduling announcement. Over the next two weeks, they gained approximately 85% before beginning to slide. By year-end 2023, the gains from rescheduling talk had dwindled to around 43%. Optimism returned in early 2024, and the ETF was up 108% by 2/2/24. However, as the anticipated DEA announcement dragged on, enthusiasm waned, and the ETF was only up 65% from its low point on 3/8/24. We generally view this as healthy skepticism.

- Individual stock performance has diverged widely. The graph shows where stocks now trade (green bars) and where the 52-week high has been (red bars) as a percent of the 52-week low. The black dot depicts the price on 8/25/23, the last Friday before the HHS rescheduling announcement, as a percentage of the 52-week low.

- The blue line indicates the company’s current EV/consensus 2024 EBITDA valuation metric.

- The graph is arranged in increasing order of gains from 52-week lows. The companies on the far left, Planet 13 (PLTH: CSE), MariMed (MRMD, CSE), Cannabist (CBST: CBOE), and TerrAscend (TSND: TSX), are up by the smallest percentage (less than 50%) from their respective 52-week lows.

- The black dots in the red indicate that MariMed and Cannabist are trading lower than before the HHS announcement.

- Companies with small red bars, including Glass House (GLASF: OTCQX), Trulieve (TRUL: CSE), and Green Thumb (GTII: CSE), are trading closest to their 52-week highs and also have amongst the highest valuation ratios. Investors are confident that each of these companies can succeed with or without Schedule 3.

- Two companies, Cannabist and AYR, are trading significantly off their highs and at low EV/EBITDA multiples, likely due to dilutive actions each took to solve debt maturity issues. Both continue to have challenging credit profiles, with significant debt maturing in 2026. Similarly, Ascend has large debt maturities in 2025 that are likely impacting its valuation. These companies are likely to be significant winners from rescheduling.

- The current environment of considerable uncertainty calls for a barbell portfolio. Investors should have a healthy concentration in the large free cash flow positive names like GTI, Curaleaf, Verano, and Trulieve as they are self-funding, and their higher multiples are still low relative to their growth and margin profile. Part of the portfolio should also be devoted to names like Cannabist, Ascend, and AYR, with lower multiples and high optionality regarding rescheduling and state legalizations in Ohio, Pennsylvania, and Florida.