OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Quick

Links

Past Charts

Home » The Changing Composition of Cannabis Debt

Chart of the Week

Chart of the Week

The Viridian Capital Chart of the Week highlights key investment, valuation and M&A trends taken from that week’s Deal Tracker that we believe are impactful for investors, companies and acquirers.

Week ended 12/16/2022

The Changing Composition of Cannabis Debt

-

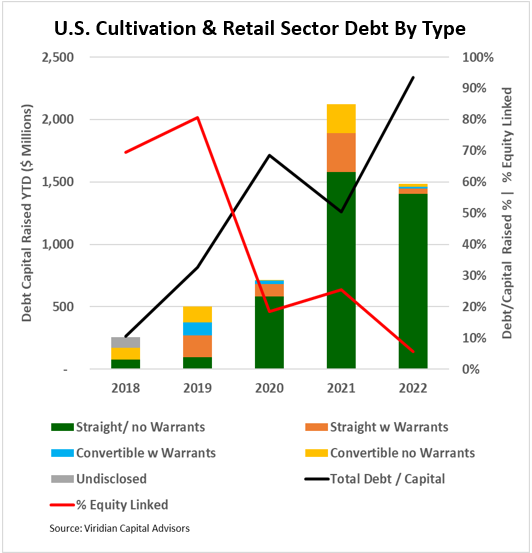

- The widespread belief that financing has dried up for U.S. Cultivation & Retail sector companies is not entirely true. Equity issuance was down sharply to only $104M YTD in 2022 from $2.1B in 2021, but luckily, debt issuance has not been as affected.

-

- The graph shows cannabis debt issuance since 2018 on a YTD basis through December 12th. Total debt issuance YTD is down 30% from record 2021 levels. Still, raises are more than twice any previous year.

-

- What has changed significantly over the years is the type of debt issued. In the early debt days of 2018, most debt issued was convertible debt. In 2019 we started to see convertible issues with additional attached warrants to achieve total coverages over 100%. High equity participation was required because the companies mainly were EBITDA negative and could not pay interest rates high enough to compensate lenders for taking essentially equity risk.

-

- As the U.S. MSOs became EBITDA positive in 2020 and 2021, issuance of straight coupon debt began in earnest, led by the $300M Curaleaf (CURA: CSE) deal in December 2020 and followed shortly after that by $100M and $120M deals by Cresco (CL: CSE) and TerrAscend (TER: CSE, respectively. Most of the top MSOs have now completed straight coupon issues, many over $100M in size.

-

- Although overall issuance is robust, 93% of it has been senior secured debt. Debt financing is available only if you have solid collateral coverage, like real estate. Cash flow lending and mezzanine debt are strikingly absent. Perhaps this is a reaction to the industry’s current challenges, the lack of legislative breakthroughs, and the impending recession. Alternatively, maybe mezzanine lenders perceive better risk/reward tradeoffs in more settled industries. It strikes us as odd that potential lenders do not more highly prize the embedded options associated with equity-linked structures.

-

- Where is cannabis debt headed long term? The development of the U.S. High Yield market is instructive:

- Credit ratings are fundamental to the development of the market as many funds have limits to the amount of unrated debt they can hold. An augmented Safe Act with cover for up-listing to major U.S. exchanges is probably a prerequisite for this.

- Standardization – Loan/bond structures, documents, and covenants will become more standardized as they did in High Yield in the mid-1980s, facilitating trading liquidity.

- Bifurcation – As in High Yield, larger Issues will migrate towards the public capital markets through public or 144A issuance. Issues less than $100 million will remain the providence of private placements and financial institution underwriting.

- Derivatives – CDS and more listed equity options will facilitate credit hedging.

- Transparency – public and private debt trades will be TRACE-eligible, providing market transparency on trading levels and spreads.

- Where is cannabis debt headed long term? The development of the U.S. High Yield market is instructive: