OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

The Viridian Capital Chart of the Week highlights key investment, valuation and M&A trends taken from that week’s Deal Tracker that we believe are impactful for investors, companies and acquirers.

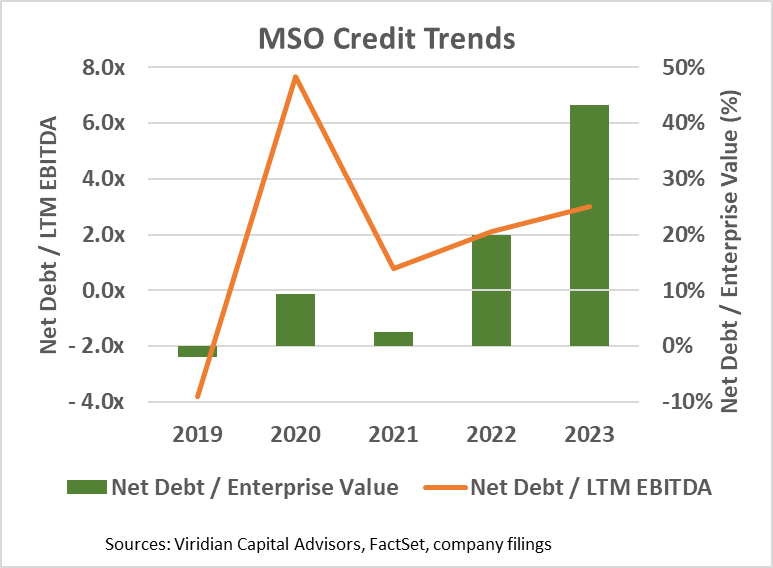

- Aggregate net debt to LTM EBITDA for the top MSOs is now 3.0x with five of the eleven over 5x, arguably unsustainable in a 280e world.

- The graph shows two essential indicators of cannabis company leverage and credit quality: Net debt/ LTM EBITDA and Net Debt/ Enterprise Value. The chart depicts Memorial Day figures using net debt and LTM EBITDA from the March quarter for each year.

- The group of companies summed in the data includes Ascend (AAWH: OTCQX), AYR (AYR.A: CSE), Columbia Care (CCHW: CSE), Cresco (CL: CSE), Curaleaf (CURA: CSE), 4Front (FFNT: CSE), Green Thumb (GTII: CSE), Jushi (JUSHF: OTCQX), TerrAscend (TER: CSE), Trulieve (TRUL: CSE), and Verano (VRNO: CSE). Note: Ascend, AYR, 4Front, and Verano data was unavailable for the period ending 5/24/19.

- The orange line (measured on the left axis) depicts Net Debt / LTM EBITDA. The green bars show Net Debt / Enterprise Value (measured on the right axis).

- As of 5/24/19, the companies included in the chart had aggregate net cash of $178M, with only TerrAscend and Trulieve carrying net debt. In 2020 net debt rose to $938M, 7.7x LTM EBITDA of $122M. Despite this jump, net debt remained below 10% of enterprise value.

- Soaring market caps and EBITDA made Memorial Day 2021 the peak of aggregate cannabis credit quality with Net Debt / LTM EBITDA of .77x and Net Debt / Enterprise Value of 2%.

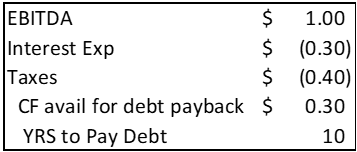

- Aggregate credit quality has deteriorated over the last two years. With the equity financing window essentially shut, MSOs have increasingly financed with debt while inflation and wholesale price pressures have stalled EBITDA growth. Net Debt is up 31% to $5.4B from $4.1B last year, while LTM EBITDA is down 7% to $1.8B from $1.94B last year. Net Debt/ LTM EBITDA is now 3.0x for the group, which doesn’t appear high in the context of leveraged finance; however, 280e substantially impacts the amount of debt that is supportable by plant-touching enterprises. Assuming 10% interest rates and 40% taxes on EBITDA (both of which seem low), a 3x Debt/ EBITDA implies a nearly 10-year debt payback period.

- Some of the group members are much better credits than others. Green Thumb and Verano have less than two turns of net debt, while Jushi and 4Front have over 10x. Still, five of the eleven companies now have net debt of over 5x LTM EBITDA.

- What is the answer? A re-equitization is needed. However, the group is now trading at an enterprise value of only $12B, down from $38B on Memorial Day 2021, and EV / LTM EBITDA is 6.8x compared to well over 20x in 2021. Given its growth prospects, the industry is incredibly cheap, but the issue is the catalyst. SAFE? Rescheduling/ Descheduling? 280e reform? None of them seem tangibly close. In the near term, debt remains the only game in town, but there are limits. Careful credit analysis is more critical in cannabis investing than ever.