OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Quick

Links

Past Charts

Home » Viridian Capital Chart of the Week: Not Every MSO Needs Rescheduling

Chart of the Week

Chart of the Week

The Viridian Capital Chart of the Week highlights key investment, valuation and M&A trends taken from that week’s Deal Tracker that we believe are impactful for investors, companies and acquirers.

Week ended 03/01/2024

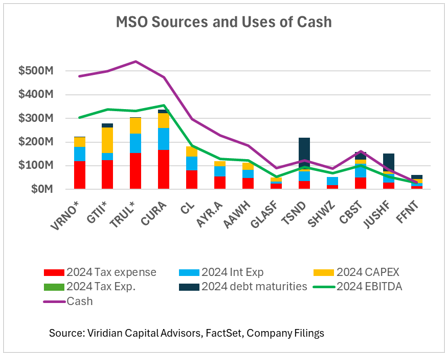

Viridian Capital Chart of the Week: Not Every MSO Needs Rescheduling

- After the first week of the 4th quarter 20243 earnings releases, several prominent MSOs have already shown their cards. GTI (GTII: CSE), Trulieve (TRUL: CSE), and Verano (VRNO: CBOE) all beat 4th quarter 2023 consensus EBITDA estimates handily. Analysts subsequently raised their 2024 EBITDA estimates for Trulieve and GTI but reduced them by about 4% for Verano after the company warned of a weaker Q1: 24.

- The most striking feature of the releases was the amount of free cash flow and balances each reported. The strength of these companies belies the pervasive claim that the industry cannot survive without 280e relief.

- The chart looks at the current cash balances and consensus 2024 EBITDA estimates against taxes, interest expense, and capex estimates. For interest expense, we have annualized the most recently reported quarter. The red bar represents tax expense, the blue bar depicts interest expense, the yellow bar shows 2024 capex, and the black bar shows 2024 estimated debt maturities. The chart is ordered in descending order of cash plus free cash flow before debt maturities.

- The companies on the left have significant free cash flow and large cash balances. They do not need rescheduling as they are doing well in the current environment. They can buy back stock, reduce debt, and fund capital spending. One could argue that the current climate gives them a competitive edge as they have capital flexibility while their competitors do not.

- The companies in the middle of the graph, including Curaleaf, Cresco, AYR, Ascend, Glass House, TerrAscend, and Schwazze, all have modest free cash flow before debt maturities. TerrAscend still shows significant maturities of senior term loans to deal with in 2024. The company is doing quite well, though, and we believe the company will successfully roll over these loans without too much stress. These companies appear to be stable in the current environment but are constrained in their capital spending and would be able to grow more if 280e was eliminated.

- The companies on the right, Cannabist, Jushi, and 4Front, have more significant issues. Each is negative free cash flow before debt maturities and all three have meaningful maturities in 2024. Rescheduling will help them; however, each has more leverage than is sustainable even in a post-280e environment. They possess significant optionality concerning state developments, and positive developments in Pennsylvania, Florida, and Virginia will be critical to their ongoing success.