OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Quick

Links

Past Charts

Home » Viridian Capital Chart of the Week: Most MSOs Have Amended and Extended 2024 Maturities, But De-Levering is Undone

Chart of the Week

Chart of the Week

The Viridian Capital Chart of the Week highlights key investment, valuation and M&A trends taken from that week’s Deal Tracker that we believe are impactful for investors, companies and acquirers.

Week ended 11/03/2023

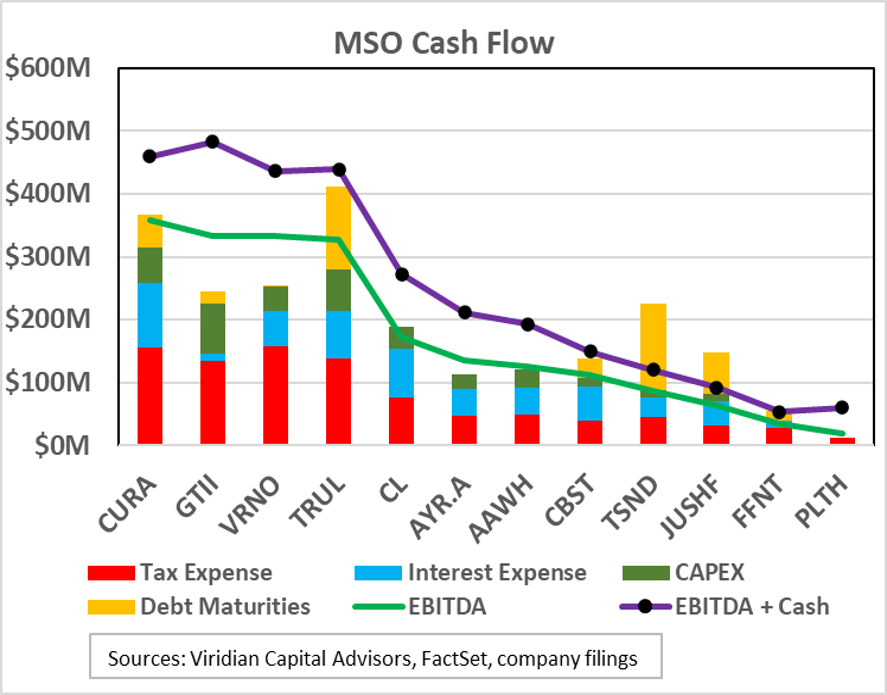

Viridian Capital Chart of the Week: Most MSOs Have Amended and Extended 2024 Maturities, But De-Levering is Undone

- The twelve MSOs shown on this week’s Viridian Chart of the Week have made significant headway on balance sheet repair; however, several still have significant 2024 maturities requiring refinancing or extensions.

- The bars in the chart show the estimated 2024 uses of cash. The red bars are consensus estimates of tax expense. The blue bars show consensus estimates of 2024 interest expense. Green bars show estimated CAPEX. The yellow bars show debt maturities adjusted for payoffs, conversions, and extensions since the June quarter’s end.

- The lines on the graph show the sources of cash: the green line is the consensus estimate of 2024 EBITDA. The purple line shows EBITDA plus June quarter cash adjusted for capital markets transactions since June.

- Several companies have made significant improvements in their balance sheets and liquidity:

- Curaleaf (CURA: CSE) issued $16M of equity in October to satisfy the TSX listing requirements and bolster liquidity.

- Cresco (CL: CSE) closed a $25M mortgage facility and sold its Arizona operations for $6.5M.

- AYR Wellness (AYR.A: CSE) completed a dramatic restructuring of its debt, extending its 12.5% issue due in December 2024 into 2026, along with several purchase money notes. The move cost the company over 25% of its equity but assured liquidity until 2026.

- Cannabist (CBST: CBOE) issued $25M of equity and used the proceeds to repurchase $25M of its 13% notes due in 2024. The company also negotiated to purchase $25M of its 6% convertible notes due 2025 for stock.

- 4Front closed on a $10M new debt facility and a $3.2M equity financing from Atmore. The company also issued warrants to extend a $2M debt maturity.

- Some MSOs still have to work through refinancing or extending maturities.

- Trulieve (TRUL: CSE) has enough cash, along with its EBITDA, to fully pay off its maturities, but it is tight. Look for further financing moves to gain some additional flexibility.

- TerrAscend (TSND: TSX) has enough cash flow to take care of its operating liabilities but has about $137M of maturities it will need to extend or refinance. Most of this debt is term loans, which may make negotiations for extensions easier.

- Jushi (JUSHF: OTCQX) has a $65M Senior Secured Credit facility that matures in December 2024.

- The top MSOs on the chart have largely fixed their 2024 liquidity issues, but investors should remain vigilant. Leverage has not been reduced; debt has been amended and extended. Re-equitization is still needed for the industry’s long-term health.