OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Quick

Links

Past Charts

Home » Viridian Capital Chart of the Week: Maybe It Really IS All About Earnings

Chart of the Week

Chart of the Week

The Viridian Capital Chart of the Week highlights key investment, valuation and M&A trends taken from that week’s Deal Tracker that we believe are impactful for investors, companies and acquirers.

Week ended 03/10/2023

Viridian Capital Chart of the Week: Maybe It Really IS All About Earnings

-

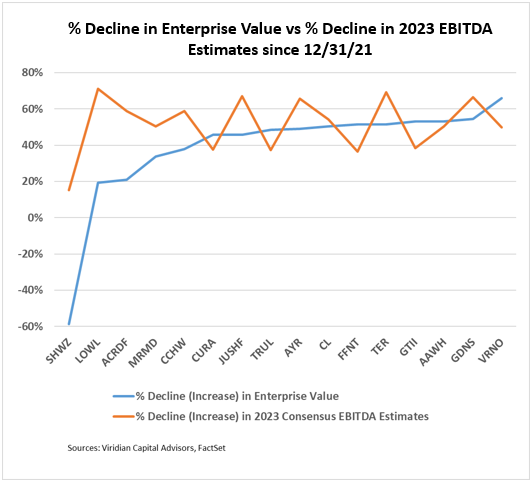

- Earnings season is upon us again, and most public cannabis companies will release results for the 4th quarter of 2022 in the next few weeks. Only two of the companies in the graph have reported to date. Green Thumb (GTII: CSE) beat consensus revenue estimates by 1% and EBITDA estimates by 1.2%, while MariMed (MRMD: 2CSE) beat revenue estimates by 2% but missed EBITDA by 33.8%.

-

- In digesting the releases, investors will pay particular attention to EBITDA and cash levels—achieving positive cash flow and maintaining liquidity trump growth in this environment.

-

- We will also be focusing on estimate revisions. We have been tracking consensus analyst estimates for 2023 since the beginning of 2022. The orange line on the graph shows the percentage reduction in 2023 consensus EBITDA estimates from 12/31/21 to 3/3/23. The average EBITDA estimate reduction is 51.6%.

-

- The blue line on the graph shows the percentage decrease in enterprise value over the same period. Schwazze (SHWZ: OTC) is the only company on the chart with increased enterprise value over the period. Interestingly, SHWZ also has the smallest 2023 estimate reduction over the period.

-

- Many explanations for the decline in cannabis company market caps and enterprise valuations center on the role of the failure of any federal legislation like the SAFE Act. The graph suggests another explanation: the percentage drop in enterprise values has primarily tracked the percentage reduction in forward EBITDA estimates. Valuations are down because expected EBITDAs are down.

-

- The causes for reduced EBITDA estimates are obvious: Commoditization-driven price declines and inflationary cost increases are pressuring margins. Companies with solid exposures to new markets like New Jersey have benefited via more robust sales and margins. However, the honeymoon period between the opening of a new market and the onset of wholesale price declines appears to be getting shorter. Unfortunately, despite some respite in California pricing, the general conditions will likely worsen before they get better, as the economy is unlikely to be headed for a soft landing.

-

- MSOs are doing the right things: cutting opex (people), tightening working capital, and reigning in capex while also seeking to take advantage of accretive acquisitions of distressed assets. The industry will emerge stronger from this stressful period, but not all competitors will make it to the other side.