OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Quick

Links

Past Charts

Home » Illiquidity vs Insolvency

Chart of the Week

Chart of the Week

The Viridian Capital Chart of the Week highlights key investment, valuation and M&A trends taken from that week’s Deal Tracker that we believe are impactful for investors, companies and acquirers.

Week ended 02/17/2023

Illiquidity vs Insolvency

-

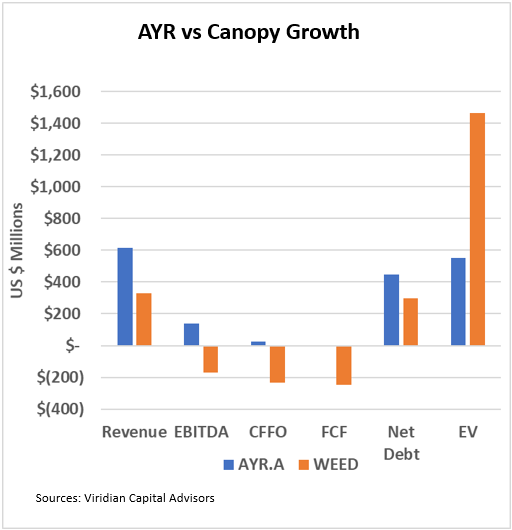

- The graph shows the consensus operating estimates for the calendar year ended 12/31/23 and Viridian Capital estimates of current net debt and enterprise value for AYR Wellness (AYR.A: CSE) and Canopy Growth (WEED: TSX)

-

- Both companies’ debt is trading at stressed/distressed levels

- AYR’s 12.5% notes due 12/10/24 have traded as low as 56.5% of par to yield around 65%.

- Canopy’s Supreme Cannabis 8% notes due 9/15/25 traded as low as 61% of par to yield close to 30% in December 2022. The company’s Sr. Secured Term loan was recently quoted at 81.

- Both companies have upcoming liquidity challenges

- AYR has relatively manageable debt maturities in 2023, but its $110M 12.5% notes maturity in December 2024 is problematic. The company has significant time to deal with refinancing, and at some time in the next 18 months, the capital markets will likely be more hospitable. The problem, however, is the sheer size of the required refinancing, representing over 100% of the company’s current market cap.

- Canopy has approximately US$ 249M of unsecured notes that mature on 7/15/23. The company currently has about $592M of cash, a negative free cash flow of around $50M per quarter, and a $100M minimum liquidity covenant in its senior debt. At its current run rate, this spells potential trouble by year-end 2023. Canopy’s net debt of $298M represents only about 20% of enterprise value giving the company flexibility to do debt/equity swaps and other financial engineering to produce liquidity, at least for the next twelve months.

- The market is valuing the companies very differently, and AYR seems relatively undervalued

- AYR is trading at EV/2023 Revenues and EV/2023 EBITDA of .92x and 3.94x, respectively, well below its peer group.

- Canopy is trading at EV/ 2023 Revenues of 4.57x, and Projected EBITDA is negative $169M. We find it difficult to support this valuation.

- AYR is the classic distressed asset situation: a good company with solid assets and positive EBITDA. It’s a bit over-levered and has looming liquidity problems, but it seems like a situation begging for creative financial solutions.

- Both companies’ debt is trading at stressed/distressed levels

-

- Canopy faces a far more complex problem. It’s been traveling the road to insolvency for years with no signs of a turnaround. Consensus estimates show over $700M of negative cash flow from operations over the next four years, significantly more than the company’s remaining cash. Sooner or later, Canopy’s ability to dilute its shareholders to fund itself will be exhausted, and it will start to hit bank covenants before then. The problem will be restructuring a negative cash flow company; we all know how well that works.