OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Quick

Links

Past Charts

Home » Viridian Capital Chart of the Week: How Aggressive Are 2nd Quarter EBITDA Margin Estimates?

Chart of the Week

Chart of the Week

The Viridian Capital Chart of the Week highlights key investment, valuation and M&A trends taken from that week’s Deal Tracker that we believe are impactful for investors, companies and acquirers.

Week ended 08/04/2023

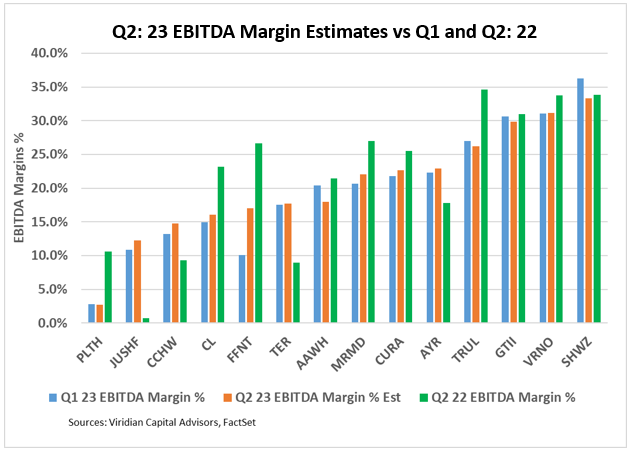

Viridian Capital Chart of the Week: How Aggressive Are 2nd Quarter EBITDA Margin Estimates?

- The chart shows analyst estimates of EBITDA margins for the second quarter vs. the first quarter and the 2nd quarter of 2022 for the fourteen largest MSOs for which we have consistent analyst projections.

- The blue bars show Q1: 23 EBITDA margins; the red bars show Q2: 23 projected EBITDA margins, and the green bars show) Q2: 22 EBITDA Margins.

- We expect 2nd quarter margins (red) to be higher than 1st quarter margins (blue), which is the case for nine of the fourteen companies on the chart. Outliers include Planet 13 (PLTH: CSE), reflecting continuing pressures in Nevada and the relative lack of seasonality between Q1 and Q2 in the market. Ascend (AAWH: CSE) also had production issues in New Jersey, causing them to lose a significant percentage of their crop. Trulieve (TRUL: CSE) is projected to have lower Q2 margins as they discount old product in Florida and clear out product to exit Massachusetts. The company also appears to be losing market share in Florida. Green Thumb (GTII: CSE) is getting more aggressive in working capital management by discounting inventory. Finally, Schwazze (SHWZ: CSE) is projected to have a lower 2nd quarter margin as Colorado and New Mexico pricing continues under pressure.

- We also expect that most companies will have lower Q2: 23 EBITDA margins than Q2: 22 based on commodification-based wholesale pricing pressures and inflation-driven cost increases. Ten of the fourteen companies on the chart follow this pattern. Outliers include Jushi (JUSHF: OTCQX), whose Q2: 22 EBITDA of $0.5M missed estimates by 86%. EBITDA has beat expectations for the last two quarters, but Q2: 23 estimates may still prove aggressive. Columbia Care (CCHW: CSE) has been ratcheting down costs in case the CL deal doesn’t happen. Terrascend (TSND: TSX) has dramatically improved its situation by scaling up in New Jersey and rationalizing its Michigan operations. Finally, AYR (AYR.A: CSE) has higher expectations based on new management, scaling in New Jersey, leaving Arizona, and gaining share in Florida.

- Analyst estimates for Q2: 23 seem mainly in line with our expectations. We will keep a close eye on the abovementioned outliers and, as always, pay close attention to full-year 2023 and 2024 revenue and EBITDA revisions. As previously discussed, we believe 2nd half 23 margin projections may still be a tad optimistic.