OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

The Viridian Capital Chart of the Week highlights key investment, valuation and M&A trends taken from that week’s Deal Tracker that we believe are impactful for investors, companies and acquirers.

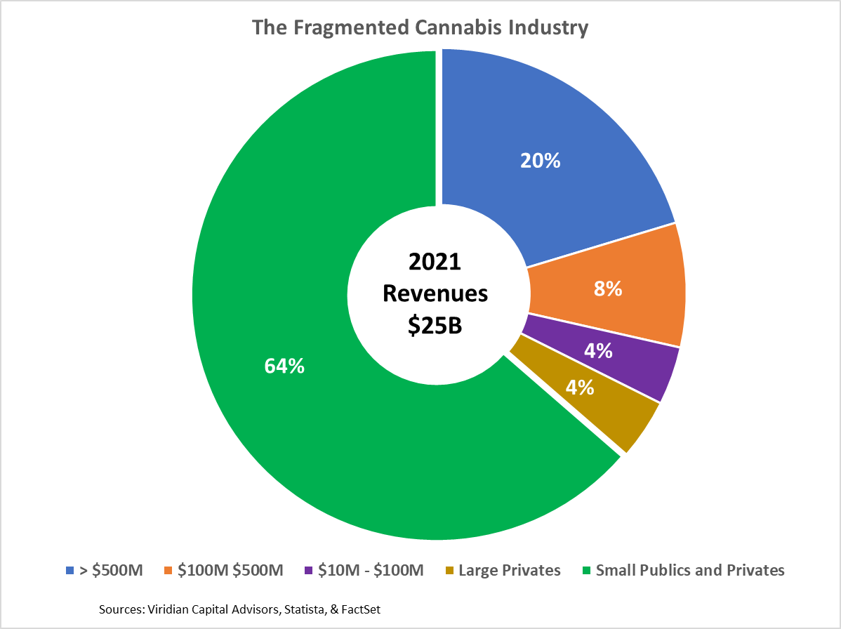

- The six largest U.S. MSOs combined accounted for approximately $5.0B (20%) of cannabis industry revenue in 2021. No single competitor represented as much as 5% of the total.

- Approximately 9,900 small companies with average revenues of around $1.6M accounted for over 60% of total industry sales.

- In contrast, the 9,100 U.S. craft beer companies in 2021 represented only 27% of beer revenues.

- As cannabis approaches legalization, the necessary scale of businesses will increase. The industry is capital-intensive, and tremendous sums will need to be spent to establish national brands, distribution systems, and centralized production facilities.

- The size of likely new entrants to the industry dwarfs current competitors. The average enterprise value of the top 5 alcoholic beverage companies is about $23B, over four times the size of the largest MSO. Similarly, the smallest of the big three tobacco companies has an enterprise value of more than twice as large as all cannabis companies combined.

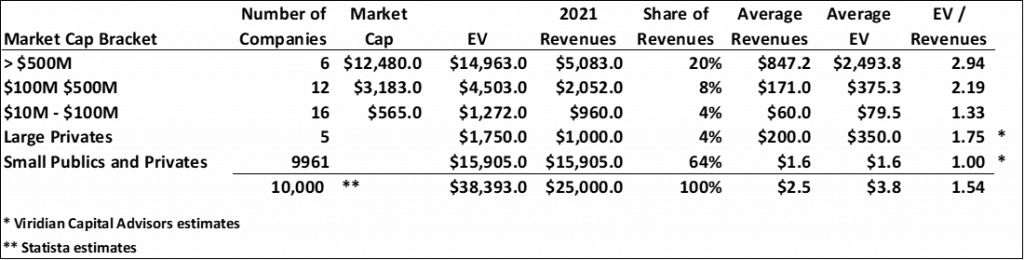

- Another powerful driver of consolidation is the cost of capital. The table’s rightmost column shows the EV / Revenue multiples of the market cap brackets. The average valuation multiple for the largest MSOs is more than twice that of the tier 3 competitors, implying ang enormous cost of capital advantage that makes it nearly impossible for the smaller companies to maintain growth.

- As the industry gets closer to federal legalization, we anticipate a wave of consolidation as companies seek to position themselves to achieve economies of scale in production, marketing, and logistics that are not yet available in the state regulatory regimes.

- As in the beer industry, there will always be thousands of craft cannabis companies, but the share of revenues earned by the largest competitors is likely to double over the next five years.