OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Quick

Links

Past Charts

Home » Challenging Operating & Financing Climate Alters M&A Consideration

Chart of the Week

Chart of the Week

The Viridian Capital Chart of the Week highlights key investment, valuation and M&A trends taken from that week’s Deal Tracker that we believe are impactful for investors, companies and acquirers.

Week ended 02/10/2023

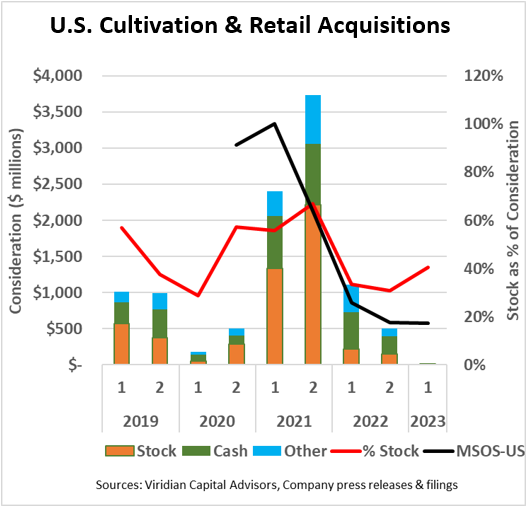

Challenging Operating & Financing Climate Alters M&A Consideration

-

- The graph shows the makeup of merger consideration for all Cultivation & Retail sector transactions where terms were disclosed.

-

- Orange bars show total consideration paid in stock, green indicates cash consideration, and blue depicts other consideration, including earn-outs and seller notes.

-

- Stock as a percentage of consideration is highly correlated with deal size. In the first half of 2021, there were seven transactions over $100M with total consideration of $1.4B, and the average stock component was 69%. Similarly, in the second half of 2021, there were ten transactions over $100M, and stock averaged 70% of the total consideration. The most significant transactions in this period, including the $398M purchase of Liberty Health Science (LHS: CSE) by AYR (AYR.A: CSE) in February 2021 and the $1.4B purchase of Harvest Health and Rec (HARV: CSE) by Trulieve (TRUL: CSE) in October 2021, were all stock transactions.

-

- Stock prices have been another significant determinant of the makeup of M&A consideration. The black line on the graph shows the price of the MSOS ETF indexed sot that its price at the end of the first half of 2021 = 100%. Prices at the end of 2022 were approximately 17% of their H1 2021 levels. As stock prices plunged, potential acquirers were less excited to use their stocks as currency, and potential sellers, looking at the recent pricing plunges, were less willing to accept stock.

-

- The 2nd half of 2022 and early 2023 have produced conditions that we believe are likely to increase the percentage of stock in M&A consideration:

- Potential acquirers are husbanding their cash more carefully as capital costs and availability have deteriorated. A good example is the recent Chicago deal cancelation by AYR. The large MSOS also perceive that the lack of federal legislation and the challenging capital markets and operating conditions put them in stronger negotiating positions relative to their potential targets.

- Target companies are having differentially more trouble accessing the capital markets, and inflationary cost pressures and commoditization-driven price declines are squeezing operating margins. We expect an increase in distressed sellers who are not in a position to dictate deal terms.

- The challenging operating environment and lack of federal legalization will likely accelerate industry consolidation. We expect to see several more significant public/public deals, with primarily stock consideration

- MSO stocks are widely believed to be trading below intrinsic value and are more palatable to targets.

- The 2nd half of 2022 and early 2023 have produced conditions that we believe are likely to increase the percentage of stock in M&A consideration: