OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Quick

Links

Past Charts

Home » Viridian Capital Chart of the Week: Cannabis Debt Volumes are Increasing and Costs are Declining

Chart of the Week

Chart of the Week

The Viridian Capital Chart of the Week highlights key investment, valuation and M&A trends taken from that week’s Deal Tracker that we believe are impactful for investors, companies and acquirers.

Week ended 08/23/2024

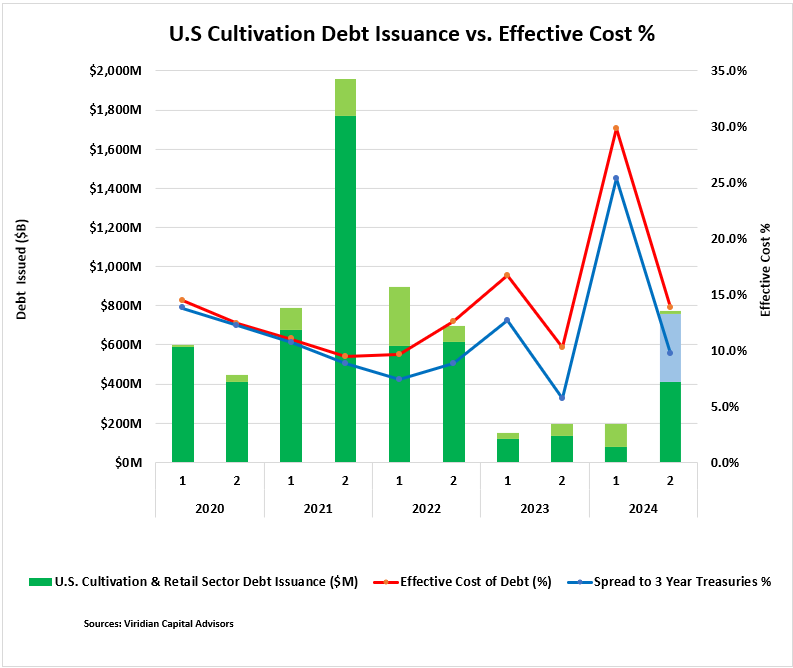

Viridian Capital Chart of the Week: Cannabis Debt Volumes are Increasing and Costs are Declining

-

- Debt issuance for the U.S. Cultivation & Retail sector in H2:24 is already ahead of any period since H2:22. With the additional financing expected for the remainder of the year, issuance should top all periods except the second half of 2021 and the first half of 2022.

- The large majority of H2:24 debt issuance has been refinancing activity, including Ascend (AAWH: Cboe), Jushi (JUSHF: CSE), and Terrascend (TSND: TSX). Each of these was priced at attractive rates despite all of them having tax-adjusted net debt well above 3x Debt/EBITDA. Debt investors are willing to believe 280e relief is on the way.

- The dark green bars on the graph depict the dollar amount of debt issuance on which sufficient data is available to calculate the effective cost. The light green bars represent the issuance where insufficient data was available. The blue bar in H2:24 depicts the additional refinancing activity we believe is likely for the remainder of the year, composed mainly of Green Thumb (GTII: CSE) and Curaleaf (CURA: TSX) maturities. The red line shows the dollar-weighted average effective cost of the raises. The blue line shows the yield spread to the 3-year treasury.

- Viridian evaluates all debt issuance on a common basis, taking into account coupon, maturity, OID, convertibility, and attached warrants. We explicitly value the embedded conversion options and warrants as additional original issue discounts in order to calculate the effective cost.

- H2: 23 effective costs were unusually low due to the high concentration of bank debt financings, including a $25M, 8.31% Trulieve, a $58.7M, 8.43% Marimed, a $25.5M, a $25M, 8.4% Cresco, and a $40M, 8.26% AYR.

- H1: 24 average effective costs were high due to two costly deals. AYR raised $50M in an add-on, which included a 13% coupon at a 20-point OID with 122% warrant coverage with -7% exercise premiums, producing an effective cost of 29.9%. The $19.5M Cannabist 9% convert was sold with a 20-point OID and a conversion premium of only 13% to create a 28.6% effective cost.

- The average effective cost has come down sharply to 13.8% in H2: 2024. The transactions in H2 included $222M Ascend at 14.24% cost, $140M TerrAscend at 12.75% cost, and $47.5M Jushi at 14.88%.

- Spreads to treasuries are nearly back to the halcyon dates of 2021, but with favorable action on rescheduling, we believe an additional tightening of 200-300bps is possible.