OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Quick

Links

Past Charts

Home » Viridian Capital Chart of the Week: Are There Opportunities For Investors In Cannabis Debt?

Chart of the Week

Chart of the Week

The Viridian Capital Chart of the Week highlights key investment, valuation and M&A trends taken from that week’s Deal Tracker that we believe are impactful for investors, companies and acquirers.

Week ended 08/04/2023

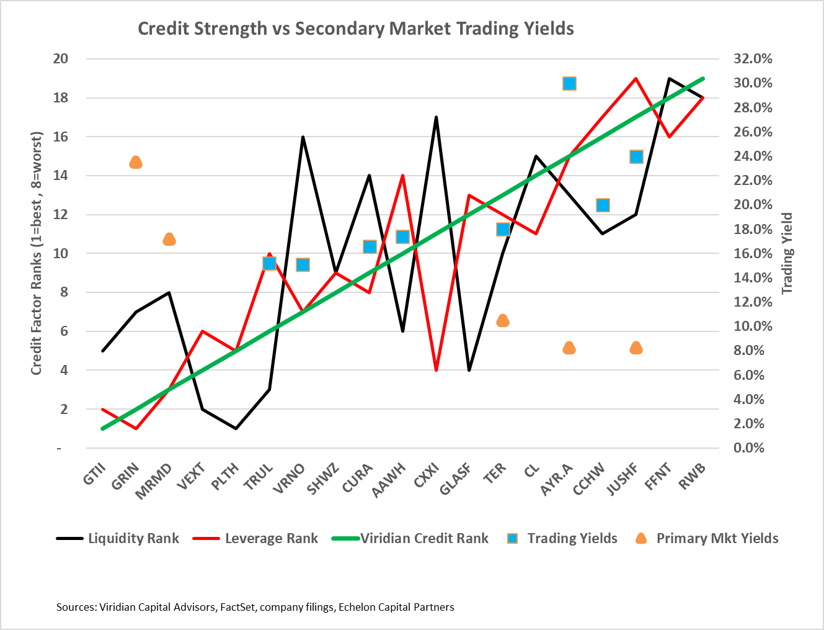

Viridian Capital Chart of the Week: Are There Opportunities For Investors In Cannabis Debt?

- The chart shows Viridian Capital Advisors Credit Tracker rankings of credit quality for nineteen public U.S. cannabis companies with market caps over $25M, along with the offered-side trading yield of the company’s debt (blue squares) or the effective cost at the closing of the company’s 2023 debt issue (orange triangle). Two companies, Columbia Care (CCHW: NEO) and Trulieve (TRUL: CSE), have more than one trading bond, and we have chosen the one with the lowest offered yield, corresponding to the shortest maturity in each case.

- Investors are struggling to decide if the cannabis equity market has finally bottomed. The MSOS has been trading in the $5-6 range since April leading investors to become more comfortable with the idea, but nagging doubts remain. Equity analysts have reduced 2023 EBITDA estimates for the top 10 MSOs by 22% since the beginning of the year, and Q2 23 aggregate EBITDA for the group is expected to be nearly 10% lower than Q2 22. SAFE and rescheduling appear possible but uncertain. Investors are left wondering where and how to ride out the storm. Viridian suggests investors look at the senior secured cannabis debt market. Stronger credits like Trulieve, Verano, and Curaleaf are trading between 15% and 16.5%, while weaker credits like AYR, Columbia Care, and Jushi trade from 20% to 30%.

- The graph shows that the pricing of cannabis debt in the secondary market generally follows the Viridian Capital Credit Tracker credit rankings. The Viridian system can be an important tool to spot pricing inefficiencies. For example, the AYR 12.5% notes of December 2024 are offered at a 30% yield, over 600bp higher than Columbia Care or Jushi (JUSH: NEO), two companies we view as worse credits. Columbia Care bonds benefit from the company’s moves to entice holders to exchange into lower coupon longer maturity bonds, and we believe similar moves by AYR to refinance or extend maturities will highlight the attractiveness of the AYR bonds.

- The orange triangles in the top left of the chart show that small companies or small issues tend to have higher effective costs even if they have good credit quality. For instance, Grown Rogue is among the top credit quality companies in the industry, but it had to pay a 23.5% effective yield to sell a $5M debt tranche. Similarly, MariMed issued debt earlier in the year with an effective cost of over 17% despite its outstanding credit quality. Investors may be able to achieve higher risk-adjusted returns in smaller names.

- The orange triangles on the lower right point out one of the ways higher-risk companies are reducing interest costs and improving liquidity. AYR Wellness received an 8.26% mortgage for its Gainesville cultivation facility while its public bonds were being traded at distressed levels. Similarly, Jushi obtained a 5-year 8.25% loan from FVCbank, while its public bonds were yielding low at 20%. TerrAscend (TSND: TSX), a better credit, secured a 10.5% financing from Needham Bank during the same week that it paid effective yields of 17.34% on a private placement. Regional banks will likely continue to edge into cannabis lending, offering benefits for lower-tier cannabis credits.

- Cannabis investors should diversify their portfolios with debt. The debt on the chart will not produce the doubling or tripling of money investors hope to achieve from cannabis equities, but these positions are significantly less risky. And getting paid 15-20% to see if this is the bottom isn’t so bad, is it? Remember, those equity doubles cannot happen unless these bonds get paid first.