OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Quick

Links

Past Charts

Home » Viridian Capital Chart of the Week: Are Ancillary Sectors Participating in the Rescheduling Price Upswing?

Chart of the Week

Chart of the Week

The Viridian Capital Chart of the Week highlights key investment, valuation and M&A trends taken from that week’s Deal Tracker that we believe are impactful for investors, companies and acquirers.

Week ended 05/17/2024

Viridian Capital Chart of the Week: Are Ancillary Sectors Participating in the Rescheduling Price Upswing?

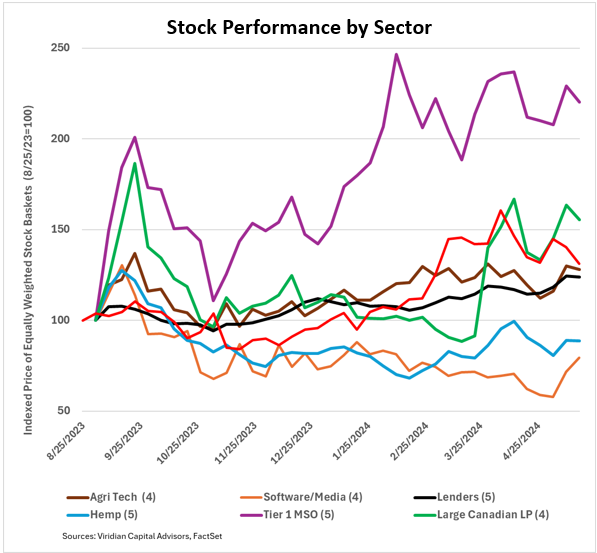

- The graph depicts the stock price performance of baskets of stocks in six different cannabis industry subsectors. Each basket consists of the top four or five U.S. companies in each group. The stocks in each basket are equally weighted, and the basket prices are indexed so that August 25, 2023 (the Friday before the HHS announcement) equals 100.

- Hundreds of articles (our own included) have analyzed the critical benefits of 280e removal, and, as expected, MSO prices have traded over 2x pre-HHS levels since the beginning of the year. We remain surprised that neither the PR Newswire leak of the DEA intentions nor Biden’s announcement has significantly rallied plant-touching stocks further. We remain incredulous that Canadian LPs are the second best-performing group on the chart despite their lackluster earnings reports and marginal-at-best cash flows.

- The brown line shows the top four ag-tech stocks, including Scotts Miracle Grow (SMG: Nasdaq), GrowGeneration (GRWG: Nasdaq), Hydrofarm (HYFM: Nasdaq), and Urban Gro (UGRO: Nasdaq). Rescheduling should benefit this group via the higher capital spending fostered expansion of cultivation capacity. New adult use states, including Ohio and, potentially, Florida and Pennsylvania, should also boost business. We do caution that very little uptick can be seen so far in their financials.

- The black line shows the top 5 cannabis lenders: IIPR (IIPR: NYSE), NewLake (NLCP: OTCQX), Chicago Atlantic (REFI: Nasdaq), AFC Gamma (AFCG: Nasdaq), and Silver Spike (SSIC: Nasdaq). Rescheduling will aid the credit quality of their borrowers and increase demand for debt since it will be tax deductible.

- The only two sectors that have suffered stock declines since the HHS announcement are Hemp and Software/Media. Hemp is likely down because of uncertainty about the contents of the new Farm Bill mixed with an increasing number of states taking action against intoxicating hemp products.

- Software (orange line) is the worst-performing sector on the graph. Plant-touching businesses, the sectors’ primary customers, have held back on non-mission-critical software systems to conserve cash. The opening of the purse strings can only be a positive for this sector. The 82 current reading hides a dichotomy with Quizam Media (QQ: CSE) at 180% of its beginning price versus Leafly (LFLY: Nasdaq) trading at only 32% of its beginning price.

- Investors are right to hold onto their plant-touching stocks as we see significantly more price appreciation ahead, even without additional near-term catalysts. Ancillary sectors have not run nearly as much, though, and attractive investments are available in the lenders, ag tech, and Software/Media sectors. They are unlikely to pop like the MSOs but offer solid returns with less risk.