OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Quick

Links

Past Charts

Home » Viridian Capital Chart of the Week: Analysts Expect Uninspiring 3rd Quarter Earnings

Chart of the Week

Chart of the Week

The Viridian Capital Chart of the Week highlights key investment, valuation and M&A trends taken from that week’s Deal Tracker that we believe are impactful for investors, companies and acquirers.

Week ended 11/01/2024

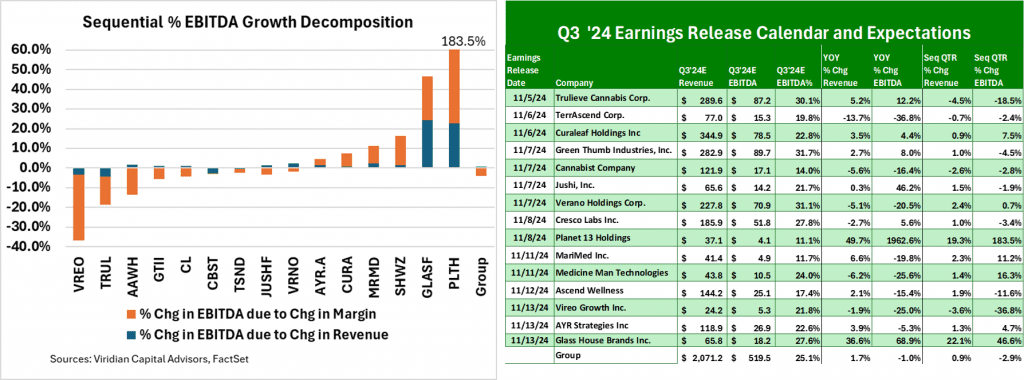

Viridian Capital Chart of the Week: Analysts Expect Uninspiring 3rd Quarter Earnings

- The table shows the expected 3rd quarter earnings release date and analysts’ consensus estimates of 3rd quarter revenue and EBITDA for fifteen of the largest MSOs. The four columns on the right calculate the Y/O/Y and sequential quarter percentage changes in Revenue and EBITDA.

- The year-over-year % changes in revenue and EBITDA for the group are expected to be 1.7% and -1.0%, respectively. Nine of the 15 companies are expected to have revenue gains, ranging from 0.3% for Jushi to 49.7% for Planet 13. Seven of the fifteen have projected EBITDA gains ranging from 4.4% for Curaleaf to nearly 2000% for Planet 13. Sequential quarterly expectations are even less inspiring, with a group growth in revenues and EBITDA of 0.9% and -2.9%, respectively. Part of the sequential-quarter change is attributable to regular seasonal changes. For example, we would expect Florida sales to dip in the 3rd quarter, and we indeed see that in Trulieve’s results. Taking Trulieve out of the totals, we would get a 1.9% revenue growth and a 1.0% EBITDA growth.

- The chart decomposes the sequential quarterly change in EBITDA into the component attributable to revenue changes (blue bars) and the component attributable to changed EBITDA margin expectations (orange bar).

- Lower EBITDA expectations are predominantly driven by lower EBITDA margins. Third-quarter group EBITDA margins are expected to be 25.1%, down a point from the 26.% actual margins for Q2. Analysts are expecting lower sequential EBITDA margins for five of the ten largest MSOs by market cap, including Green Thumb, Trulieve, Cresco, TerrAscend, and Ascend. Curaleaf, Verano, Glass House, AYR, and Planet 13 are expected to have sequentially higher margins.

- Why is Y/O/Y and sequential growth in revenue and EBITDA so low? The overall pattern shows the impact of continued cash husbanding, low capex, and restrained M&A activity. Managements have commented about pressured consumer spending and ongoing wholesale price compression. In addition, the Ohio rollout has has failed to produce the magnitude of gains that many expected.

- Catalysts like S3 and Florida rec will help; however, neither of these will impact results until mid-2025 at best. Meanwhile, we expect gains to mainly be derived from a continued reshuffling of the deck, as MSOs concentrate their M&A and capex dollars on markets where they are vertically integrated with critical scale and solid profitability.