OUR 9TH YEAR OF PROVIDING PROPRIETARY CAPITAL MARKETS INTELLIGENCE ON THE CANNABIS / HEMP / PSYCHEDELIC SECTORS

Quick

Links

Past Charts

Home » Viridian Capital Chart of the Week: A Different Perspective on Valuing Distressed Cannabis Equities – Option Based Valuation

Chart of the Week

Chart of the Week

The Viridian Capital Chart of the Week highlights key investment, valuation and M&A trends taken from that week’s Deal Tracker that we believe are impactful for investors, companies and acquirers.

Week ended 11/15/2024

Viridian Capital Chart of the Week: A Different Perspective on Valuing Distressed Cannabis Equities – Option Based Valuation

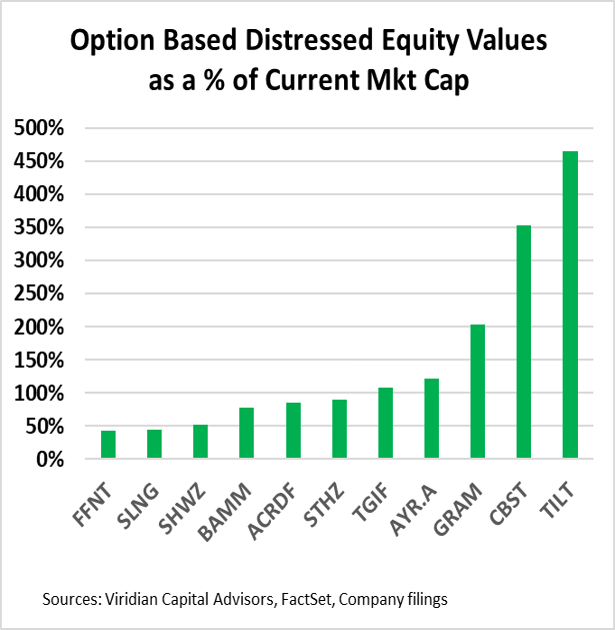

- Analysts have a range of choices when valuing cannabis companies. Viridian commonly uses Discounted Cash Flow Analysis, Public Company Comparables, and M&A Precedent Transactions to value both small private concerns as well as larger public companies.

- But, consider the task of valuing a company where the current asset value is close to or even below the value of the debt. The companies in the chart all have total liabilities to market cap in excess of 9x, a good measure of distress. In addition, our initial assigned asset value for all of them, except Cannabist, is lower than the debt.

- Does that mean that the equity is worthless? No, it doesn’t. Finance theory teaches us that we can look at equity as a call on the value of the assets with a strike price of the debt. If the value of the assets is more than the value of the debt, then equity holders have the option to liquidate the assets for the difference. If the asset value remains less than the debt, the equity holders can hand the keys to the debt holders and walk away with no further liabilities. In that framework, corporate equity can never be worth zero unless the time for the option runs out. The chart compares our option valuation with the current market cap of each company.

- The application of this simple idea is less obvious. How do we get the current value of the assets, for example? We have chosen a maximum of 1x sales and a liquidation value of 1x tangible assets. We realize these values seem low, but remember, we are talking about equities with considerable credit risk. Another question is how do we get the option life? We have chosen the weighted average maturity of the debt. For companies whose debt is already classified as a current liability, we have assigned a one-year life.

- Volatility is a crucial assumption of any option model, and we have chosen 30% as our number. This is the same value we use to model the equity call options embedded in convertible debt or warrants. We have found this to be a pretty good value, lower than observed volatilities of equities but responsive to the fact that cannabis equities option valuation is constrained by the difficulty and expense of shorting the stocks. It should be a reasonable, although arguably conservative, estimate of asset value volatility.

- We use the Black-Scholes model as our valuation engine since none of these companies are likely to pay a dividend in the near future.

- Several of these companies, including Slang, Statehouse, and Tilt, are in the process of liquidating assets. Others like AYR, Cannabist, Gold Flora, and Schwazze are not currently in any restructuring process despite our debt metrics indicating distress.

- Note that six of the eleven companies have option valuations below their current market caps, while five are considerably higher.

- It is natural to view volatility as a negative, but investors should remember that the opposite is true. Distressed cannabis equities have two critical assets that don’t appear on the balance sheet: time and hope. With so many potential positive catalysts on the horizon, option valuation techniques are an important tool to consider, particularly for those higher-risk equities.